Author: Shania, Jay Jo

Source: Tiger Research

Translated by: Blockchain Plain Language

JP Morgan is issuing deposit Tokens on public blockchain and integrating technology into existing order. In contrast, Circle is building a completely technology-based new order by establishing a trust bank.

Interestingly, these two participants with entirely different backgrounds and approaches are now embracing new technologies and constructing new institutions. This strategy ultimately blurs the boundaries between them.

However, this identity ambiguity may weaken their inherent competitive advantages, as previously experienced in the fintech industry. Therefore, each participant needs to understand their "unfair advantage" and find a balance between technology and institutions.

1. The Battle for On-Chain Financial Infrastructure

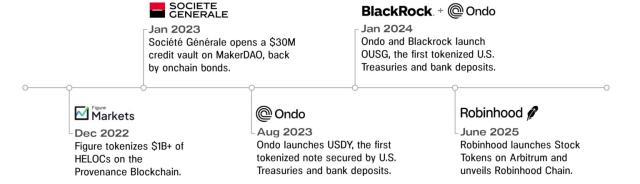

Blockchain technology is becoming the new cornerstone of global financial infrastructure. Traditional financial institutions and native crypto companies are fiercely competing for leadership in the next-generation financial system. JP Morgan is improving efficiency by integrating blockchain technology into the traditional financial system, while Circle is dedicated to building a new financial infrastructure entirely based on blockchain as an alternative to traditional structures.

This pattern is similar to the past competition between fintech and techfin driven by large tech companies. However, the current competitive landscape is entirely different. Previous competition was mainly focused on improving user experience and providing limited financial services, while now the competition has deepened to the core infrastructure level, covering asset issuance, fund flow, settlement, and asset custody.

This competition is not just about technological advantages, but about who will design and operate the future financial ecosystem. Traditional financial institutions are trying to transform incrementally within existing regulatory and system frameworks, while native crypto companies focus on technological efficiency and scalability, building a completely new order. This report will explore the on-chain financial strategies of JP Morgan and Circle, analyze the development direction of on-chain financial infrastructure, and how various participants are shaping the new global financial order.

2. JP Morgan: Building Blockchain on Traditional Finance

Source: JPMD Filing

In June 2025, JP Morgan's blockchain division Kinexys began trial operation of deposit Tokens (JPMD) on the public blockchain Base. Previously, JP Morgan had only applied blockchain technology on a small scale in private blockchain infrastructure. This time, JP Morgan adopted a different strategy, directly issuing assets and supporting on-chain transactions on an open network. This marks a crucial turning point for traditional financial institutions to directly operate financial services on public blockchain.

JPMD combines the characteristics of digital assets and traditional deposits. When customers deposit US dollars with JP Morgan, the bank records it as a deposit on the balance sheet and then issues an equivalent amount of JPMD Tokens on the public blockchain. These Tokens can circulate freely on the blockchain while retaining legal claims to bank deposits. Token holders can exchange them for US dollars at a 1:1 ratio and may enjoy deposit protection and interest income. Unlike traditional stablecoins that concentrate returns on the issuer, JPMD provides users with more substantial financial benefits.

These features provide asset managers and investors with practical conveniences beyond conventional legal stability. For example, assets operating on public blockchain can use JPMD as a payment tool, enabling 24-hour redemption. Compared to stablecoins that require a separate "withdrawal" path to exchange for fiat currency, JPMD supports instant cash conversion. Additionally, JPMD offers deposit protection and potential interest income, thereby enhancing the on-chain asset management ecosystem.

JP Morgan's launch of deposit Tokens is to address capital flows and new revenue structures around stablecoins. For instance, Tether generates approximately $13 billion in annual revenue, and Circle also earns billions by managing safe assets like US government bonds. These stablecoins' income models differ from traditional loan-deposit spreads but generate similar revenue structures through customer funds.

Of course, JPMD also has limitations. Its design fully complies with existing financial regulatory frameworks, making it difficult to achieve complete decentralization and openness of blockchain. Currently, the service is only available to institutional clients. Nevertheless, JPMD provides a practical strategy for traditional financial institutions to enter financial services based on public blockchain while maintaining stability and compliance. Many industry observers believe that JPMD represents the continued evolution of structural connections between traditional finance and the on-chain ecosystem.

3. Circle: Building Native Finance on Blockchain

Circle has become a key player in on-chain finance through its stablecoin USDC. USDC is pegged 1:1 to the US dollar, with reserves composed of cash and short-term US Treasury bonds. USDC's technological advantages include low cost and instant settlement, and many companies use it as a practical alternative for corporate payments and cross-border remittances. USDC supports 24-hour real-time fund transfers without the complex procedures of the traditional SWIFT network, helping businesses overcome the limitations of traditional financial infrastructure.

However, Circle's current business structure has some limitations. BNY Mellon serves as the reserve custodian for USDC, with BlackRock managing asset operations. This structure outsources core functions to external institutions. While Circle can earn interest income, its direct control over assets is limited. Moreover, its current revenue model is highly dependent on a high-interest environment. To achieve long-term sustainability and revenue diversification, Circle needs a more independent financial infrastructure and stronger operational permissions.

Source: Circle

To address these limitations, Circle applied to the Office of the Comptroller of the Currency (OCC) in June 2025 to establish a national trust bank. This move is not just a compliance effort but a transformation strategy. Many industry observers believe this marks Circle's transition from a mere stablecoin issuer to a comprehensive financial institution. The trust bank identity will enable Circle to directly manage reserve custody and asset operations, thereby strengthening internal control of its financial infrastructure and expanding digital asset custody services for institutional investors.

Circle originated as a native crypto company but is now adjusting its strategy to build sustainable operations within existing institutional frameworks. This involves trade-offs such as reduced flexibility and increased regulatory burden. The scope of future permissions will depend on policy developments and regulatory interpretations. Nevertheless, this move marks a key milestone in how on-chain financial structures grow and adapt within existing institutional frameworks.

4. Who Will Lead On-Chain Finance?

Participants from different backgrounds are actively entering the on-chain financial ecosystem, from traditional financial institutions like JP Morgan to native crypto companies like Circle. This phenomenon is reminiscent of the past competitive landscape in the fintech industry. At that time, tech companies entered the financial field by internalizing core functions like payments and remittances, while traditional financial institutions expanded user touchpoints and improved operational efficiency through digital transformation.

The key is that this competition is not simply parallel but breaks down the boundaries between the two. Similar phenomena are now reappearing in the on-chain finance field. For example, Circle is directly handling core functions like reserve management and asset custody by applying to establish a trust bank. JP Morgan, on the other hand, is issuing deposit Tokens on public blockchain, expanding into on-chain asset management. Both start from different directions but gradually absorb each other's strategies and business areas, trying to find a new balance point.

This trend brings new opportunities, but also comes with risks. Traditional financial institutions rushing to imitate tech companies' agility and speed may conflict with existing risk control systems. For example, Deutsche Bank pushed a "digital-first" strategy and made massive IT investments, but system errors caused by conflicts with old infrastructure resulted in billions of dollars in losses.

In contrast, native crypto companies face different risks. They might sacrifice flexibility and execution capabilities—which have been their main competitive advantages—in pursuit of institutional acceptance.

The success of on-chain financial competition ultimately depends on a profound understanding of one's own foundations and unique advantages. Enterprises must develop strategies based on their "asymmetric advantages" and coordinate the integration of technological and institutional frameworks. The ability to balance these two elements will determine the ultimate winner.

Article link: https://www.hellobtc.com/kp/du/07/5986.html

Source: https://reports.tiger-research.com/p/battle-of-onchain-finance-idn