Author: DeFi Cheetah, Crypto KOL

Translated by: Felix, PANews

As previously predicted, the US stock market would experience at least a 20% pullback, pulling Bitcoin's price back to around $50,000. The first target has been achieved: due to Trump's imposition of stricter tariffs on many other countries, the US stock market underwent a 20% pullback with the VIX index around 55. Bitcoin's price once dropped to $74,000, showing more resilience than historically expected.

Next, it is expected that the Federal Reserve will cut interest rates before June, followed by a rebound in the US stock market and crypto market. In fact, Trump has just explicitly requested that Federal Reserve Chairman Powell cut interest rates. This article will explain in detail why Trump is so obsessed with rate cuts and why he is bullish on the crypto market.

Two Urgent Issues Brought by High Interest Rates

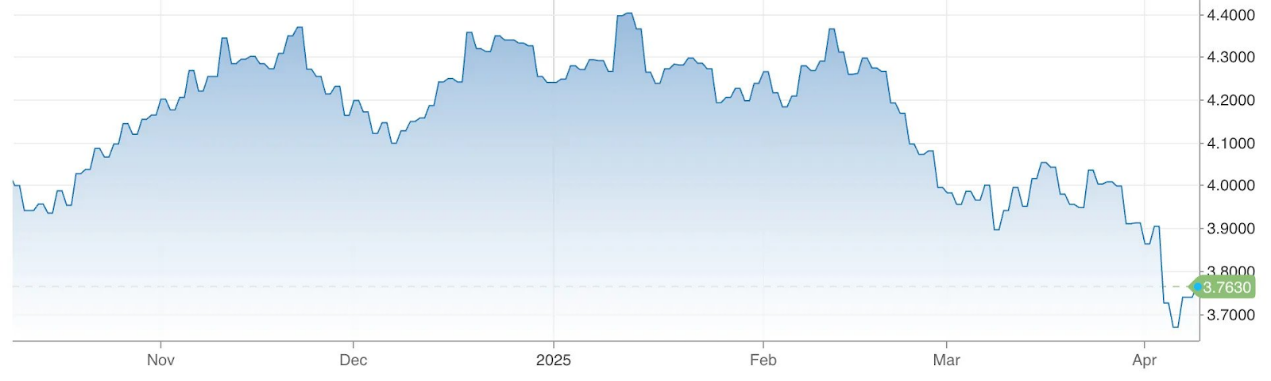

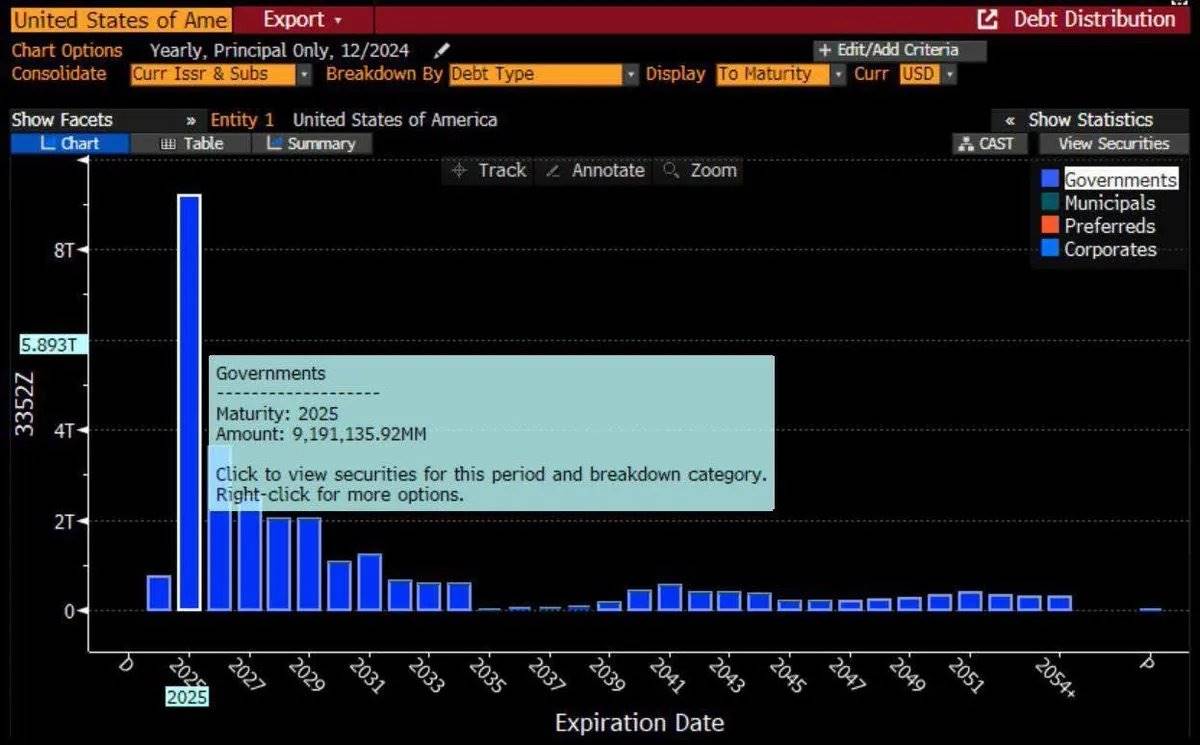

There are two issues in the coming months that will force the Federal Reserve to significantly cut interest rates. First, the "Maturity Wall" of $9 trillion in government bonds this year forces the Trump administration to seek rate cuts to save trillions of dollars in refinancing costs. However, from the Federal Reserve's perspective, the current inflation level does not leave room for rapid rate cuts. Therefore, the best explanation for the seemingly irrational aggressive policies and measures of the Trump administration (such as tariffs and establishing Doge) is that they constitute a synergistic mechanism trying to force the Federal Reserve to cut rates through macroeconomic uncertainty. Otherwise, the US government will have to pay at least 3-4 times the interest after extension. In fact, the two-year short-term Treasury bond yield has been declining, reflecting market risk aversion and capital inflows into Treasury bonds.

In the Trump administration's view, the urgency of rate cuts can be explained by the following chart:

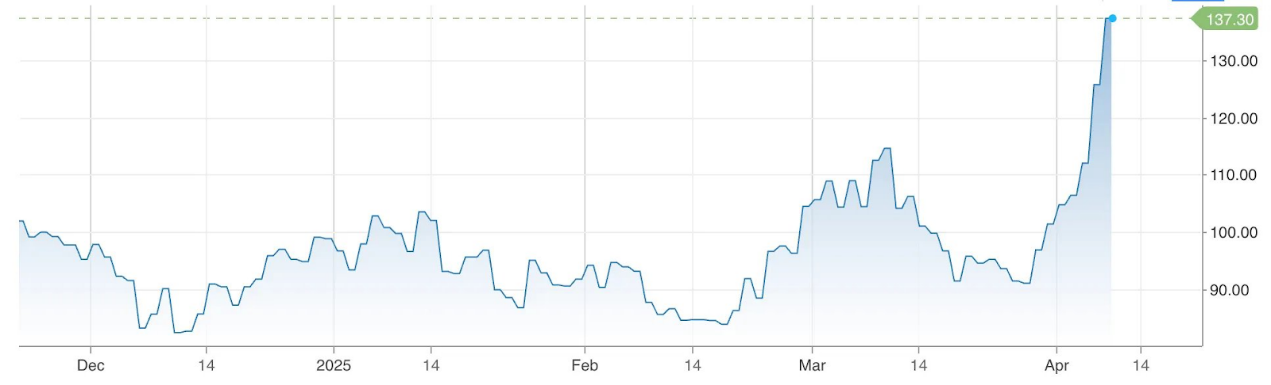

In fact, the surge in the Merrill Lynch Option Volatility Estimate Index (MOVE), which measures the interest rate volatility of the US Treasury market, further proves the possibility of the Federal Reserve cutting rates. This index is considered a representative of the US Treasury term premium (the yield spread between long-term and short-term bonds). As the index rises, anyone involved in US Treasury or corporate bond financing transactions will be forced to sell due to higher margin requirements. If the MOVE index continues to rise, especially above 140, it may indicate extreme market instability and could force the Federal Reserve to stabilize the Treasury and corporate bond markets through rate cuts, as these markets are crucial to the normal functioning of the financial system. (Note: The last time the MOVE index surged above 140 was due to the Silicon Valley Bank collapse - the largest bank failure since 2008.)

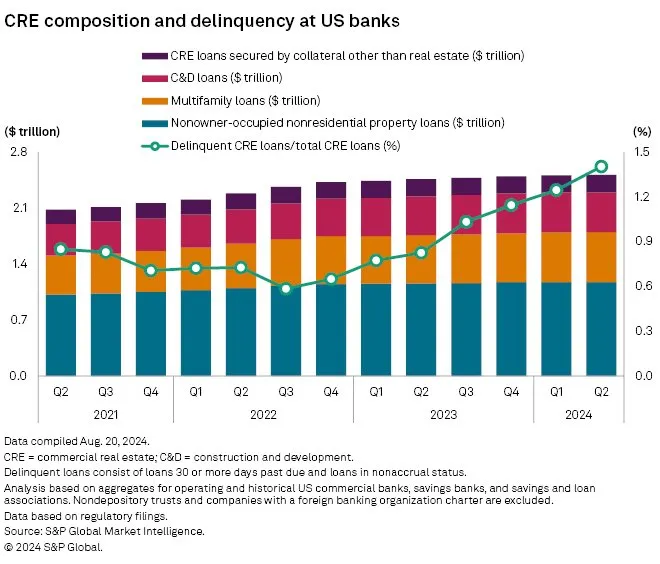

The second reason for significant rate cuts in the coming months is also due to the "Maturity Wall", this time referring to over $500 billion in US commercial real estate (CRE) loans maturing this year. Many CRE loans were previously underwritten at lower rates during the pandemic and now face refinancing challenges in a continuously rising interest rate environment, potentially leading to increased default rates, especially for highly leveraged real estate. Particularly with the rise of work-from-home, structural changes have led to persistently high vacancy rates post-pandemic. In fact, potential large-scale CRE loan defaults could cause the MOVE index to surge.

In the fourth quarter of 2024, the CRE loan delinquency rate was 1.57%, higher than 1.17% in the fourth quarter of 2023. Historical data shows that rates above 1.5% are concerning, especially in a monetary tightening environment. Meanwhile, with vacancy rates as high as 20%, continuously rising capitalization rates (around 7-8%), and a large number of loans maturing, office values have dropped 31% from their peak, and default risks have correspondingly increased.

The logic here is: High vacancy rates will reduce Net Operating Income (NOI), lower Debt Service Coverage Ratio (DSCR) and debt yields, but increase capitalization rates. High interest rates will exacerbate this situation, especially for loans maturing in 2025, where refinancing at higher rates may be unsustainable. Therefore, if commercial real estate loans cannot be refinanced at reasonable low rates similar to the pandemic period, banks will inevitably have more bad debts, which in turn could trigger a "domino effect" with more bank failures (recall the severity of bank collapses like Silicon Valley Bank during the 2023 interest rate surge).

Given these two urgent issues caused by current high interest rates, the Trump administration must take aggressive measures to cut rates as soon as possible. Otherwise, these debts must be extended, and the US government will face higher refinancing costs, while many commercial real estate loans may not be extended and could create a large number of bad debts.

Stablecoins - Catalyst for the Next Bull Market

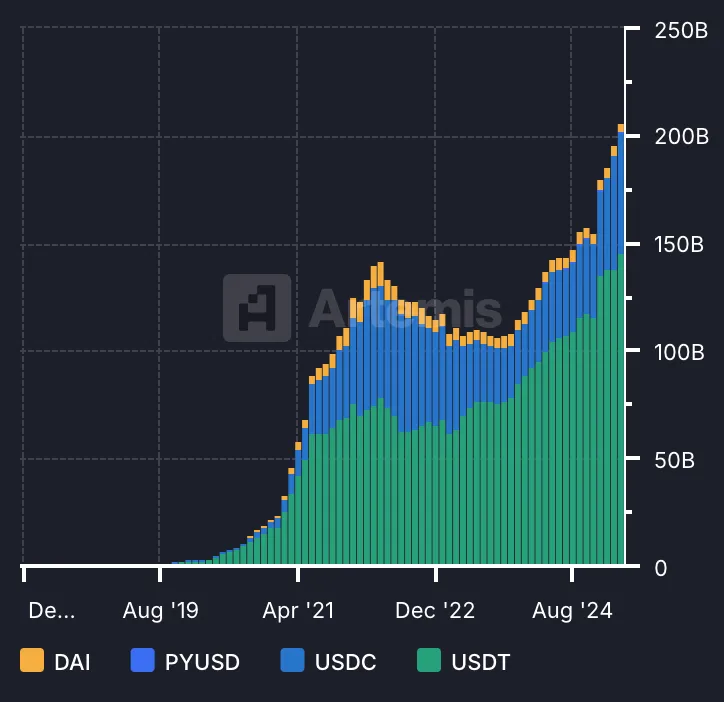

Market liquidity has the most significant impact on the crypto market. However, the factors most influencing liquidity are (i) monetary policy and (ii) stablecoin adoption. Under dovish monetary policy, stablecoin adoption can further catalyze capital inflows in the bull market. The bull market's upside potential depends on the increase in total stablecoin supply. In the previous bull market (2019 - 2022), the total stablecoin supply grew 10-fold from its trough to peak, while it has only grown about 100% from 2023 to early 2025, as shown in the chart below.

Below are key events indicating rapid stablecoin adoption growth in the next year:

US Stablecoin Legislation Progress: In the first quarter of 2025, the Senate Banking Committee approved the GENIUS Act in March, outlining regulatory and reserve rules for stablecoin issuers. The bill aims to integrate stablecoins into the mainstream financial system, reflecting growing recognition of their role in the crypto market. Additionally, the US House Financial Services Committee passed a stablecoin framework bill - the STABLE Act, which stipulates that any non-bank institution can issue stablecoins with federal regulatory approval. Regulatory transparency has always been considered the most important factor affecting stablecoin adoption, thereby influencing capital inflows into the crypto industry.

Accelerated Institutional Adoption: Fidelity began testing a USD-pegged stablecoin in late March, marking an important step for this traditional financial giant into the crypto realm. Meanwhile, Wyoming announced plans to launch a state-government-backed stablecoin by July, aiming to become the first fiat-backed, fully reserved token issued by a US entity.

World Liberty Financial Stablecoin: Trump-related World Liberty Financial announced on March 25 plans to launch a USD-pegged stablecoin called USD1, after previously raising $500 million through a separate token sale. This move aligns with the Trump administration's policy of supporting stablecoins as critical infrastructure for crypto trading.

USDC Expands to Japan: On March 26, Circle partnered with SBI Holdings to launch USDC in Japan, making it the first stablecoin officially approved under the Japanese regulatory framework. This move reflects Japan's proactive attitude towards incorporating stablecoins into its financial system and may serve as a model for other countries.

PayPal and Gemini Advance Stablecoin Development: Throughout the first quarter, PayPal and Gemini consolidated their positions in the stablecoin market. The adoption of PayPal's PYUSD and Gemini's GUSD increased, with PayPal leveraging its payment network and Gemini focusing on institutional clients. This intensifies competition among U.S. stablecoin issuers.

More Use Cases for Rise Payroll Platform: On March 24, the payroll platform Rise expanded its services to provide stablecoin payments for international contractors in over 190 countries. Employers can pay salaries in stablecoins, and employees can withdraw in local currency.

Circle's IPO: Circle has submitted an IPO application. If approved, Circle will become the first stablecoin issuer to be listed on the New York Stock Exchange. This will mark the official status of stablecoin business in the U.S. and encourage more companies, especially large institutions, to explore this field, as stablecoin business relies heavily on institutional resources, distribution channels, and business development.

Why was the Trump administration so actively supportive of stablecoin development? This is consistent with the first part's perspective: the collateral for circulating stablecoins is primarily short-term U.S. Treasury bonds. Therefore, as the U.S. government rolls over trillions of dollars in maturing bonds this year, the more prevalent stablecoins become, the higher the demand for short-term Treasury bonds.

The market direction is clear: in the short term, there may be market turbulence with high volatility, potentially further declining from current levels. However, from a medium-term perspective, with dovish monetary policy, significant interest rate cuts, and the proliferation of stablecoins, another strong bull market comparable to the previous cycle is expected.

Now is an ideal time to potentially obtain good returns through investing in the crypto market.