Written by Tristero Research

Compiled by Saoirse, Foresight News

In 2025, US cryptocurrency policy reached a critical turning point. For years, the industry had been mired in a state of "regulation through enforcement"—litigation replacing clear rules, applying outdated precedents to emerging technologies, and causing markets to fluctuate wildly based on headlines. Compliance became a guessing game, and talent flowed to Europe and Asia, where the rules were at least clearly defined and enforceable.

This year, the situation finally changed. In January, SAB 121, which had previously hindered banks from conducting cryptocurrency custody services, was repealed. In June, the US Congress passed the GENIUS Act, which recognized stablecoins at the federal level for the first time and pegged their value to the US dollar. On September 2nd, the US SEC and the Commodity Futures Trading Commission (CFTC) ended their years-long deadlock and issued a joint statement inviting institutions such as Nasdaq and the Chicago Mercantile Exchange (CME) to list Bitcoin and Ethereum spot products under the same standards as stocks and futures.

Now, there's finally a narrow but real path for launching cryptocurrency projects, conducting bank custody services, and institutional investors to enter the market—without having to worry about sudden rule changes in court. The signal is clear: the United States wants to integrate cryptocurrencies into its financial system and intends to set global standards for its operation.

The Era of Law Enforcement and Supervision (2021-January 2025)

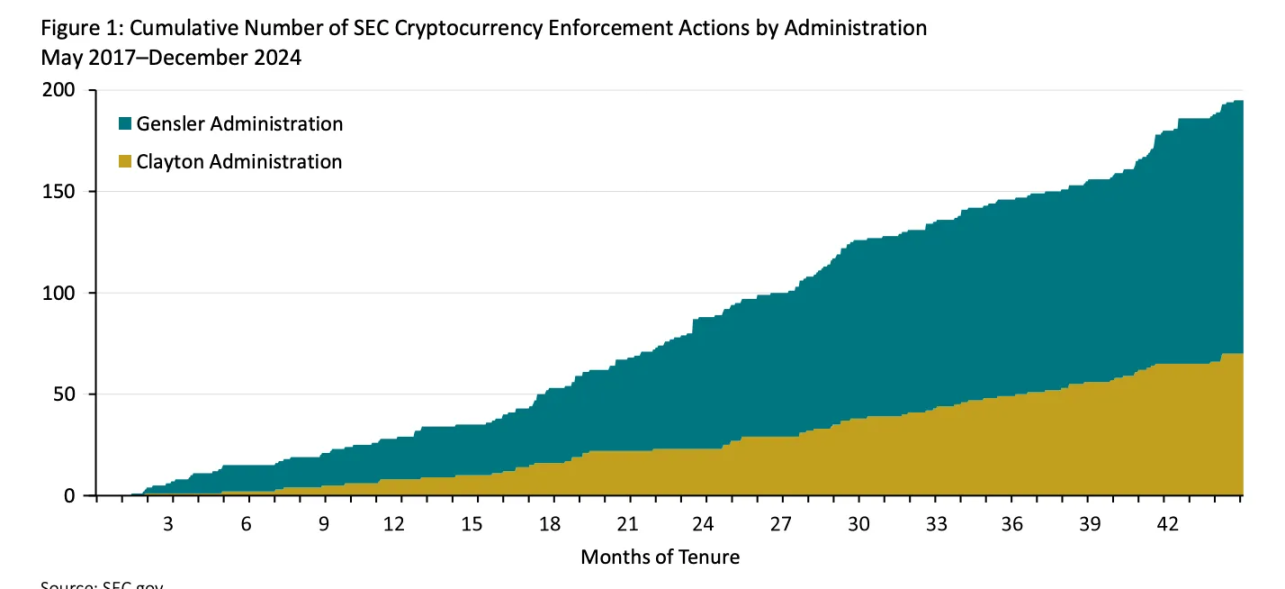

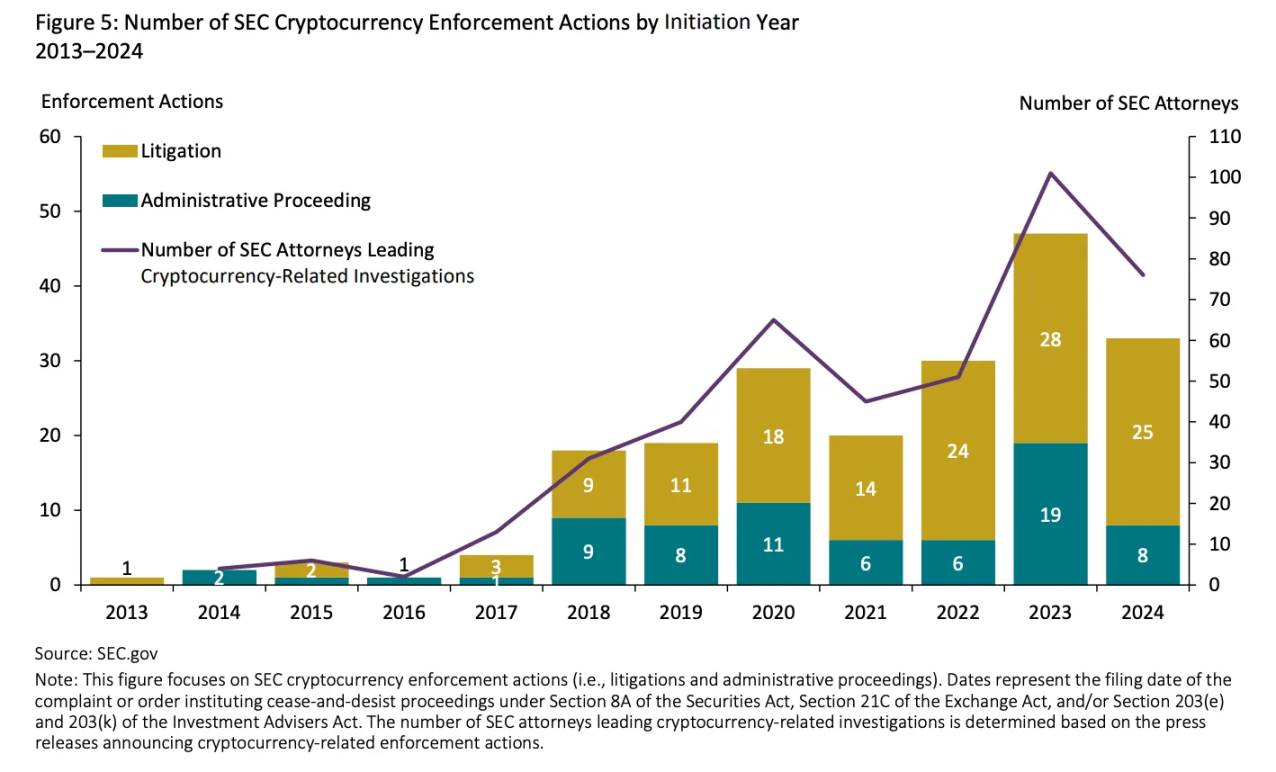

For much of the past decade, the U.S. cryptocurrency industry has been shrouded in legal uncertainty. During Gary Gensler's tenure as SEC Chairman, regulators relied on a 79-year-old precedent, the "Howey Test," to define the entire industry. This 1946 Supreme Court case ruled that if the buyer of a Florida citrus grove expects to profit from the labor of others, then the sale of the grove constitutes an "investment contract." This logic, which seemed reasonable in the mid-20th century, has been forcibly applied to tokens, blockchains, and decentralized networks. The SEC believes that as long as people buy a token with the expectation that the developer will increase its value, the token is a security. By this standard, almost any asset in the cryptocurrency field may be classified as a security.

Critics point out that this isn't "regulation" at all, but rather a political and legal strategy designed to control the industry without providing a path for compliance. The end result is years of court battles rather than a clear regulatory framework.

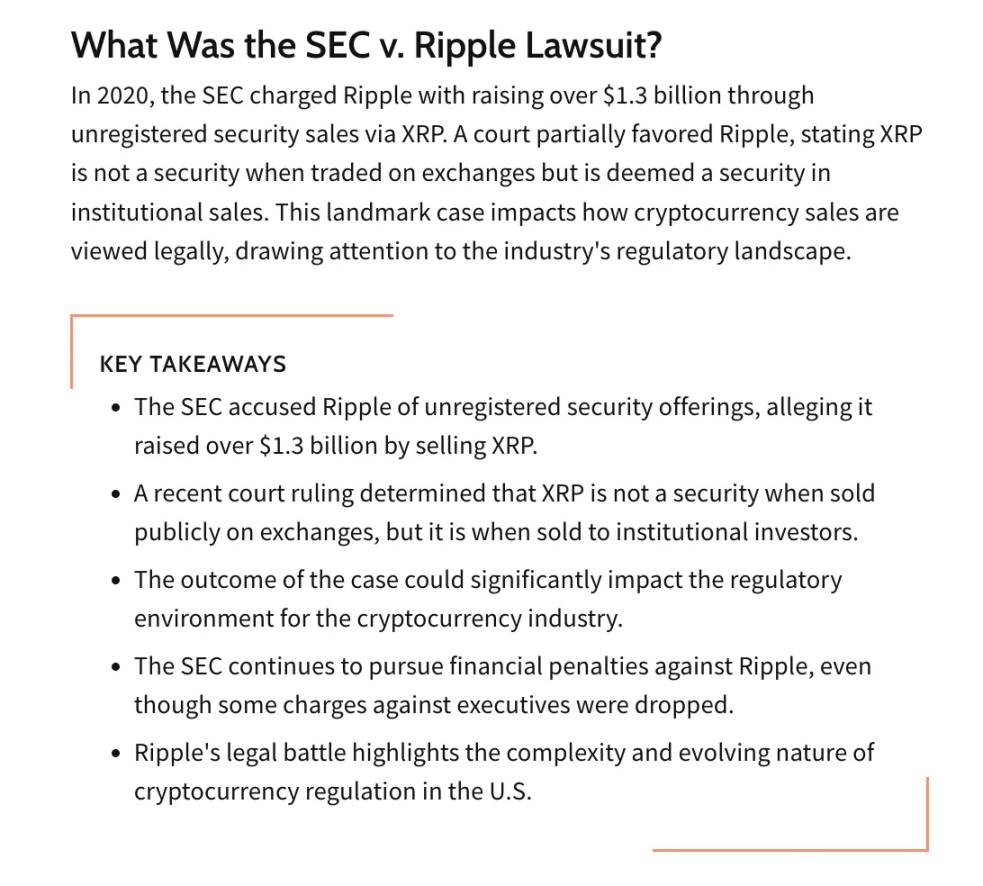

Ripple Case: One Token, Two Legal Identity

In December 2020, the SEC filed a lawsuit against Ripple Labs, accusing it of raising $1.3 billion through an unregistered securities offering of XRP tokens.

After years of litigation, Judge Analisa Torres ruled in a partial victory in July 2023: XRP was not a security when sold to the public on exchanges (because retail buyers did not rely on Ripple's operations for returns); however, when sold directly to institutions, XRP was deemed a security because the contract and marketing tied the token's value to Ripple's efforts. This ruling set a unique precedent: the same asset could have both "security" and "non-security" status in different scenarios. Exchanges and issuers were completely confused, unable to determine which actions would trigger SEC prosecution.

Coinbase Case: Approved First, Then Sued

The SEC's lawsuit against Coinbase further highlights regulatory tensions. In 2021, Coinbase went public with an SEC-approved S-1 registration statement. Two years later, in June 2023, the SEC sued Coinbase, alleging it was operating as an unregistered exchange, broker, and clearinghouse.

Coinbase immediately countered, pointing out that the SEC had reviewed and approved its disclosures during its IPO. It even raised an equitable estoppel defense, arguing that the government's silence during the IPO period amounted to "implied approval," and that a subsequent lawsuit constituted "active misconduct." While this legal argument is extremely difficult, it accurately reflects the industry's frustration: no matter how much it cooperates with regulators, the rules are always changed after the fact, as if the industry is designed to lose.

The cost of uncertainty

The market isn't waiting for the final verdict. Academic event studies show that when the SEC classifies an asset as a security, its price plummets: by 5.2% within three days and over 17% within a month.

Traders call this phenomenon the "SEC effect"—a sell-off driven not by asset fundamentals but by regulatory enforcement news. Talent and capital are flowing to Europe (such as the EU's Markets in Crypto-Assets Directive, MiCA) and Asia (such as Singapore's licensing regime) simply because these regions' rules at least clarify what's permitted. Meanwhile, the SEC in Washington continues to expand its enforcement staff: under Gensler's tenure, each cryptocurrency case has an average of 8.3 lawyers, far exceeding the 5.9 under his predecessor, Jay Clayton, demonstrating the intensity of litigation-driven regulation.

In early 2025, this strategy finally came to an end. The new administration dropped pending lawsuits against Coinbase and other companies, marking the end of the "era of regulatory oversight." While this left a legacy of uncertainty, stagnant innovation, and capital flight, it also paved the way for a major shift in regulatory direction: regulators moved away from battling the industry in court and began building a systemic framework to support it.

Spring 2025 Agenda: Building a New Regulatory Architecture

In 2025, US cryptocurrency regulation underwent a radical shift. The White House transformed its campaign promise of "becoming the global capital of cryptocurrency" into policy, demanding that regulators stop viewing cryptocurrency as a "problem to be punished" and instead view it as an "industry to be regulated." The working group's stated goal: to leverage existing regulatory authority to clarify rules, attract talent, and ensure the United States' central position in blockchain innovation.

The SEC and CFTC responded with a dual-track approach—Project Crypto and Crypto Sprint—which together constituted the first attempt to establish a long-term regulatory framework for digital assets.

Redrawing the regulatory landscape: a conceptual overhaul

The biggest shift occurred in regulatory philosophy. In a landmark speech, SEC Chairman Paul Atkins declared: “Most crypto assets are not securities.”

This statement completely overturned the previous assumption—regulators no longer assumed that almost all tokens met the definition of securities under the Howey Test, but instead adopted a more nuanced classification approach. The "Crypto Initiative" was subsequently launched to modernize securities laws through rulemaking and guidance, creating space for assets that did not easily fit into the 20th-century classification system.

Safe Harbor System: Unrestricted Innovation

For years, new network projects have been mired in a dilemma: any token distribution could be deemed a "securities offering." The new agenda introduces exemptions and safe harbors, allowing projects to launch operations under regulatory oversight and meet disclosure obligations, while gradually achieving "full decentralization." This system recognizes the evolving nature of crypto projects: tokens don't need to be permanently considered securities.

Spot access: opening the door to the mainstream market

On September 2, 2025, the joint statement of the SEC and the CFTC shocked the market, clarifying that current laws do not prohibit national exchanges such as Nasdaq, the New York Stock Exchange (NYSE), and the Chicago Mercantile Exchange (CME) from listing Bitcoin and Ethereum spot products.

Under the protection of regulatory guardrails such as "monitoring, secure custody, and transparent transaction reporting", digital assets were officially allowed to enter the same trading venues as traditional securities and commodities for the first time.

Custody unlocking: a key step for institutional entry

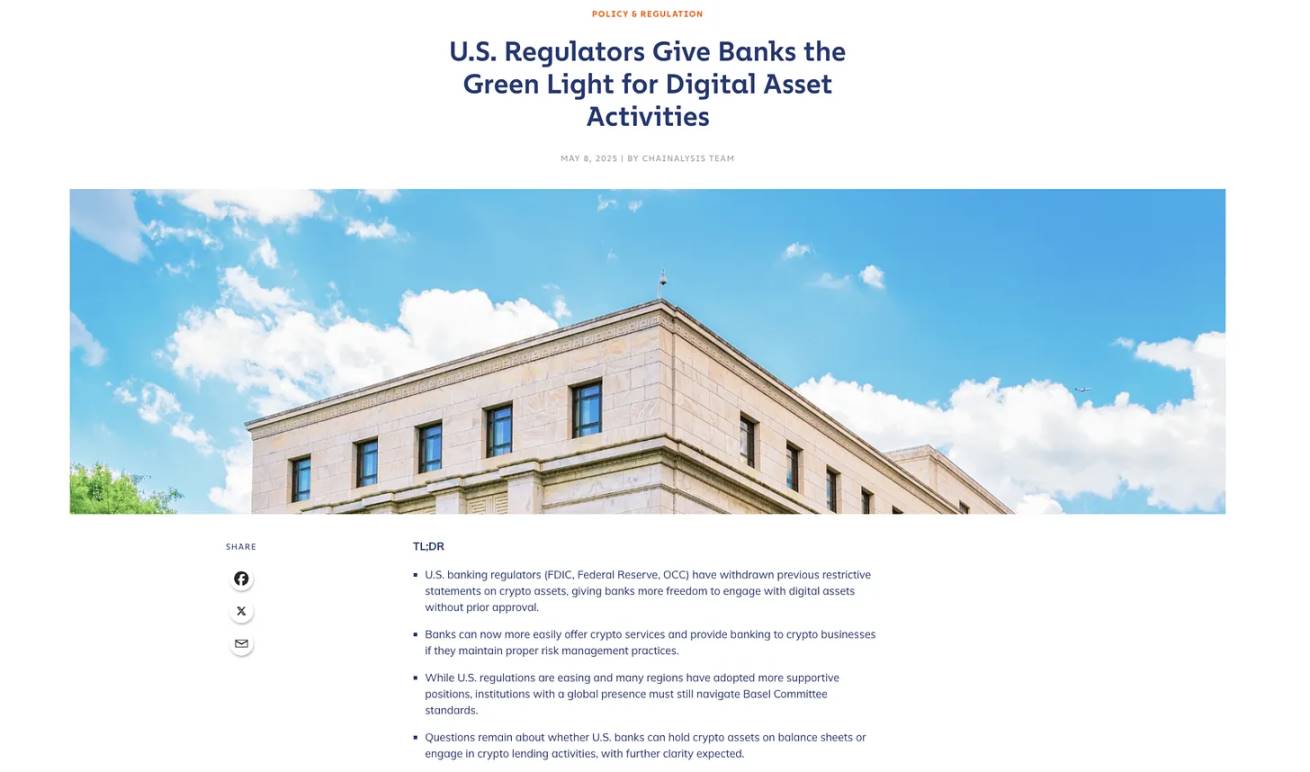

For a long time, SAB 121, a rule requiring banks to treat client cryptocurrencies as their own liabilities, created a "poison pill" clause with significant capital consumption. One of the first steps of the new regulatory framework was the repeal of SAB 121. Subsequently, directives were issued to adjust custody rules, allowing banks and custodians to securely hold digital assets. This change opened the door for traditional financial institutions, finally meeting the demand of asset allocators for institutional-grade, secure custody.

The Rise of “Super Apps”: Integrated Service Frameworks

Atkins also led his team to design a framework for "integrated intermediaries." The vision is for a single licensed entity to offer trading, lending, pledging, and custody services for both securities and non-securities. Instead of facing the current fragmented landscape of overlapping licenses, American companies would be able to offer integrated digital financial services on a single platform, emulating the popular Asian model.

A coherent strategy: Bringing cryptocurrencies into Wall Street's orbit

Taken together, these measures represent a coordinated effort to integrate cryptocurrency into the U.S. financial system. While the previous era of law enforcement led to the flight of talent and trillions of dollars in market capitalization overseas, the new agenda combines nationalistic narratives of "American leadership" and a "golden age of cryptocurrency" with mechanisms that favor large, regulated institutions. The permitting of spot exchange-traded products (ETPs), bank custody, and licensed super-apps all point in the same direction: integrating cryptocurrency into the fabric of Wall Street's operations.

While this strategy offers stability and investor protection, it also narrows the diversity of the industry ecosystem. For many, the future of cryptocurrency in the United States will rely on familiar financial institutions rather than peer-to-peer protocols. While the concept of decentralization hasn't died, it has been pushed to the brink of rapid integration into traditional financial systems.

A New World Order: A Global Benchmark for Cryptocurrency Regulation

The US regulatory shift is not an isolated incident. Across the globe, other power centers are competing to shape cryptocurrency rules according to their own logic. Three core models have emerged: the European "rulebook model," the US and UK "integrated model," and the Asian "sandbox model."

Europe: Rulebook

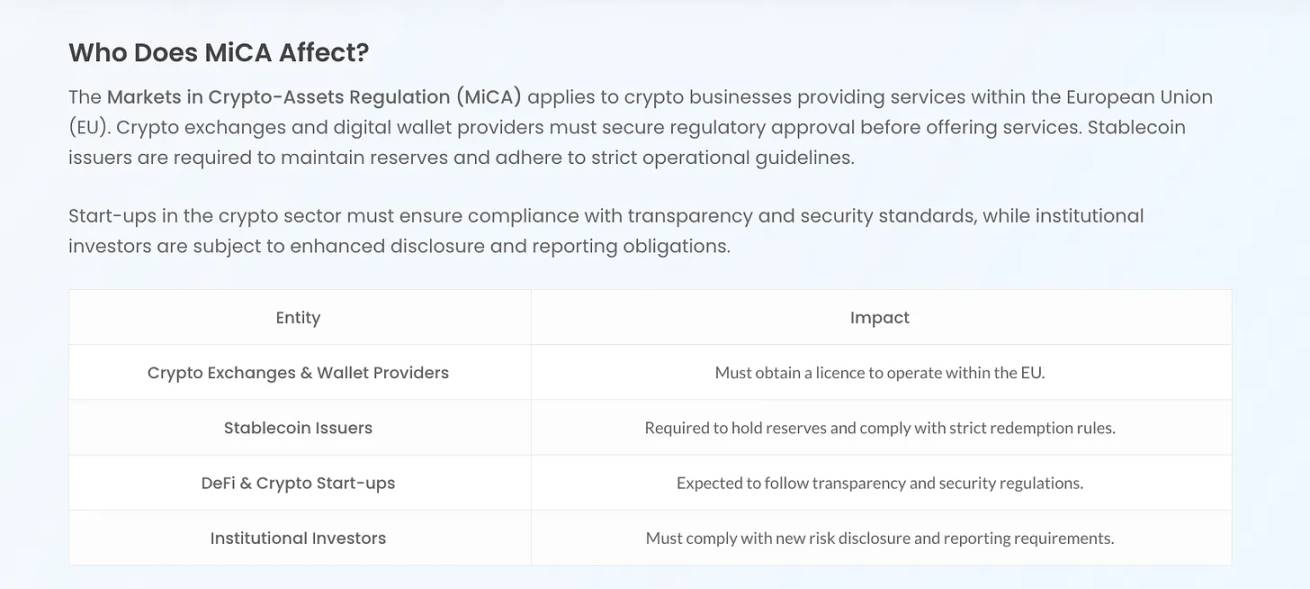

The EU's Markets in Crypto-Assets Directive (MiCA) officially came into effect at the end of 2024, providing unified regulatory framework for all 27 member states. This framework strictly categorizes tokens (e.g., asset-referenced, e-money) and establishes a "single license" system—once approved, businesses can operate across the EU. While MiCA provides legal certainty, it lacks flexibility and currently excludes NFTs and DeFi from its regulatory scope.

UK: Deeply integrated

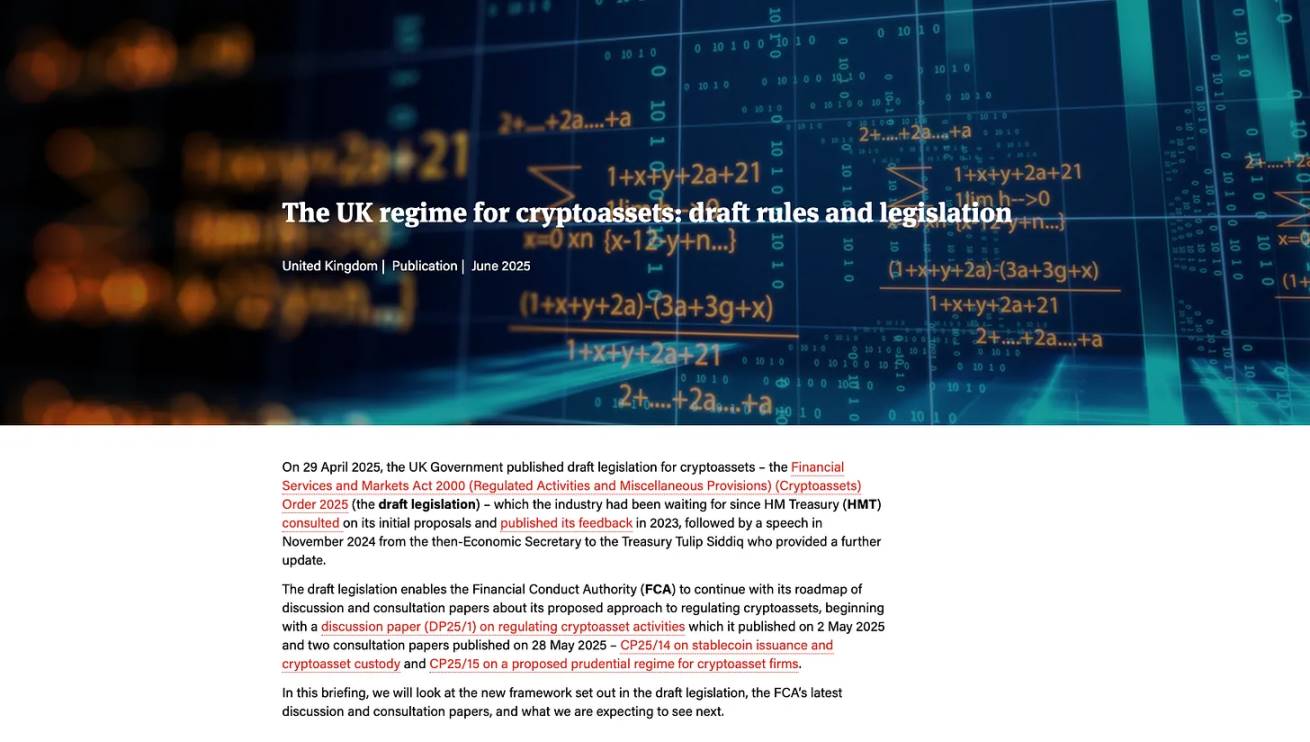

The UK has expanded the scope of the Financial Services and Markets Act (FSMA), incorporating cryptocurrencies into the existing financial system and even defining activities like custody and staking as "regulated services." This "beyond MiCA" approach is both detailed and comprehensive, requiring all overseas institutions that engage with UK retail clients to comply with UK rules.

Asia: Sandbox Hub

While the United States is mired in litigation, Singapore and Hong Kong have chosen a pragmatic approach:

Singapore has established a tiered licensing system under the Payment Services Act, formulated strict anti-money laundering/counter-terrorist financing (AML/CFT) rules, and set detailed standards for stablecoins;

Hong Kong, China has reopened its cryptocurrency market through an exchange licensing system, and has recently further expanded retail investors' trading rights for mainstream tokens.

The two places have clear goals: to quickly attract business, gradually update regulations, and build a global cryptocurrency hub.

China: Special exceptions

China still prohibits all private cryptocurrency trading, mining, and exchanges, focusing its efforts on developing a digital yuan. However, US initiatives in the stablecoin sector (particularly the GENIUS Act) are forcing China to reevaluate its policies. USDT has been widely used in China to circumvent regulations, and policymakers are currently considering whether to allow the issuance of RMB-backed stablecoins, with Hong Kong likely serving as a pilot platform.

Together, these models outline a "divided global crypto landscape": Europe seeks control through single regulations, Asia pursues flexibility and competitiveness, and the United States incorporates cryptocurrencies into the Wall Street orbit, betting that the depth of its capital market will make its model the global default standard.

Market reaction

The market is forward-looking. Even before the SEC and CFTC issued their joint statement, investor behavior already indicated anticipation of a policy shift. Every regulatory signal in 2025—the repeal of SAB 121 in January, the dismissal of the Coinbase lawsuit in March, and the Senate's passage of the GENIUS Act in June—infused the market with momentum. When Chairman Atkins delivered his "Crypto Plan" speech in September, the capital market was well aware that the "era of law enforcement regulation" had officially ended.

Institutional capital inflows: ETP becomes a key indicator

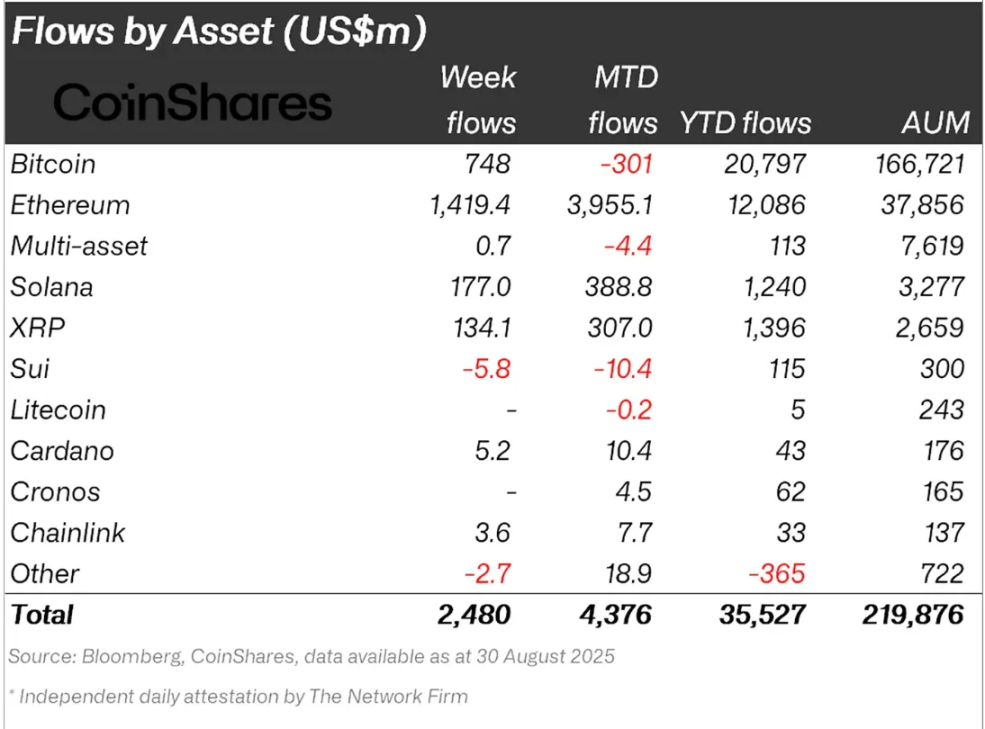

The most intuitive evidence comes from exchange-traded products (ETPs): From the beginning of 2025 to the present, the net inflow of US cryptocurrency ETPs has exceeded US$35 billion, of which Ethereum funds account for the largest proportion; in August alone, the inflow scale reached US$4.9 billion, and nearly US$4 billion flowed into Ethereum-related products.

The shift of funds from Bitcoin to Ethereum is a typical signal of increased institutional confidence - once institutions trust the regulatory framework, they will allocate assets further outside the risk curve.

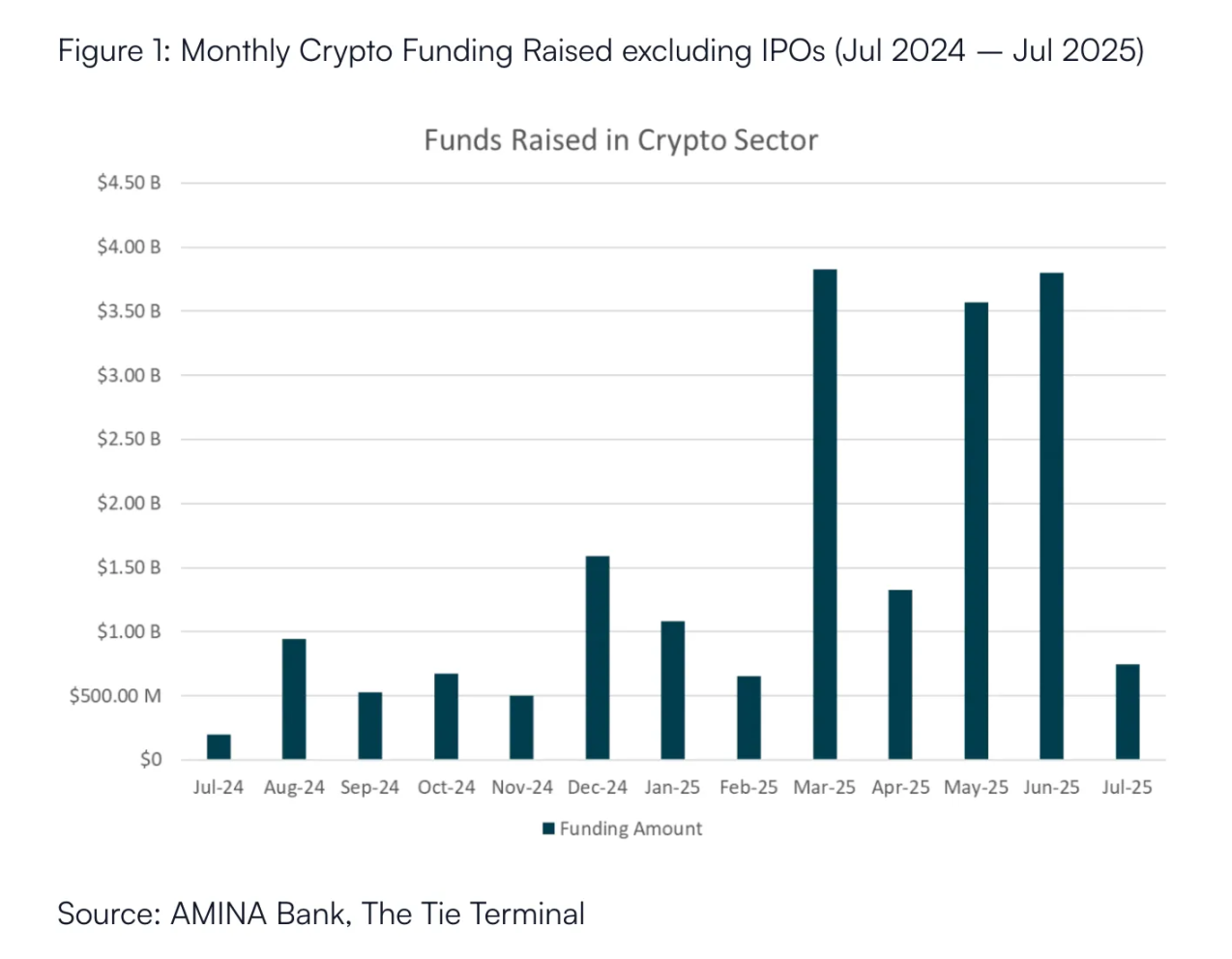

Venture Capital Rebounds: From "Speculation" to "Compliance"

In the second quarter of 2025, cryptocurrency startups raised over $10 billion in funding, double the amount raised in the same period of the previous year and the strongest quarter since the 2021 bull market.

Unlike the previous "diversified bets on popular concepts", current capital investment is more disciplined: nearly half of the funds flow into trading venues and compliance infrastructure, indicating that venture capital is "following regulatory clarity" rather than chasing hype hotspots.

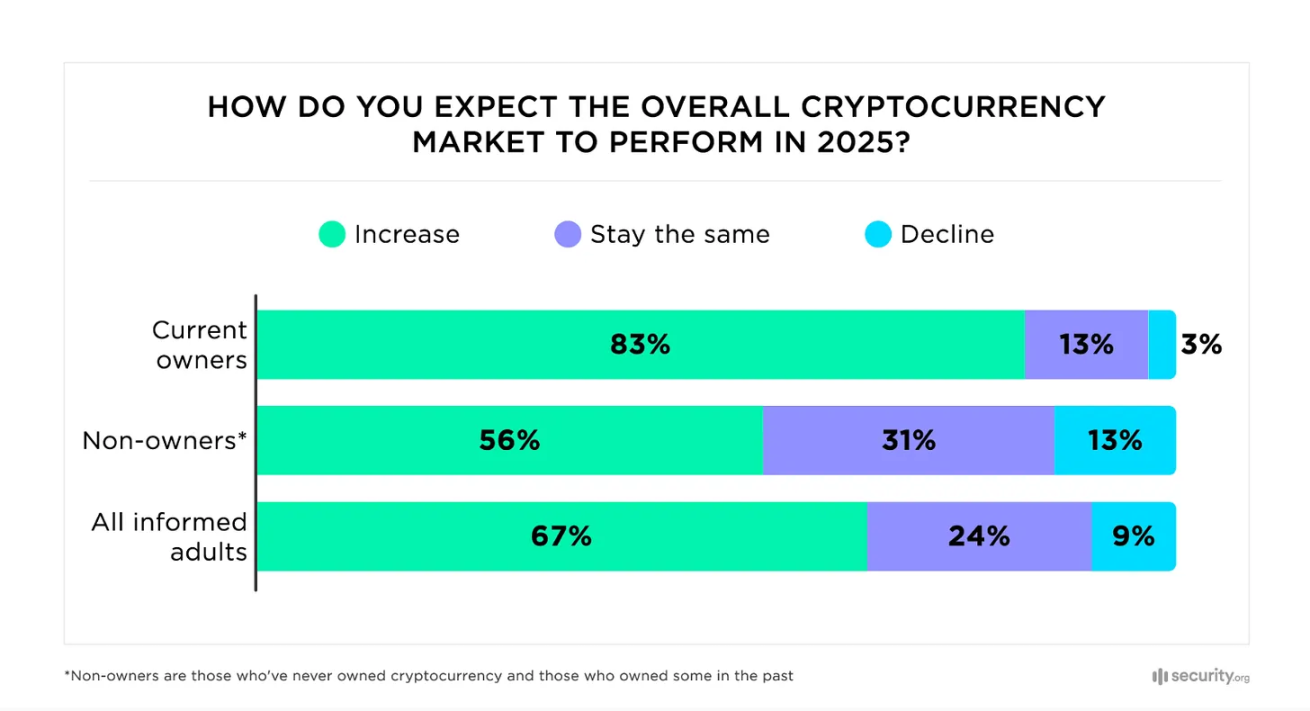

Retail investor sentiment: Optimism returns to 2021 levels

A survey in early summer showed that American investors' optimism about cryptocurrencies has reached a peak since 2021: more than 60% of Americans who understand cryptocurrencies expect cryptocurrencies to appreciate during the new president's term; two-thirds of existing holders plan to increase their holdings.

In short, the market had already "read the signals" and wasn't waiting for a final announcement in September. Each policy move—the repeal of stringent accounting rules, the dismissal of lawsuits, the passage of stablecoin legislation—pushed more capital from the sidelines to the market. The joint statement from the SEC and CFTC simply formalized expectations that investors had already priced in: the United States was back on the cryptocurrency scene, and capital was flowing back with it.

Winners, losers, and new vulnerabilities

Every major regulatory shift creates winners, losers, and hidden risks. The US regulatory shift is no exception—it not only opens the door to innovation but also redefines the competitive landscape by favoring some players and excluding others.

Winners: Compliance firms and traditional financial giants

Compliant exchanges: Platforms like Coinbase and Kraken, which have built compliance systems over the years, have become a natural gateway for US capital to enter the market. After the SEC dropped its lawsuit against Coinbase in early 2025, it has practically become the default exchange in the US market.

Wall Street institutions: The repeal of SAB 121 and the approval of spot products open the floodgates for banks and asset management companies. Traditional core financial services such as custody, ETFs, and physical subscriptions have officially entered the market. Giants like BlackRock and Fidelity can easily integrate cryptocurrencies into their existing distribution systems and quickly capture market share.

Compliant Stablecoin Issuers: Stablecoins that meet the stringent requirements of the GENIUS Act (such as Circle's USDC) leverage federal oversight to transform regulatory liabilities into competitive advantages. The market reaction was immediate: Coinbase's stock price rose on USDC's anticipated growth, while Visa and Mastercard's stock prices fell due to the potential impact of stablecoins on the credit card settlement system.

Tokenized RWA platform: Clear securities definition standards and compliant issuance safe harbors provide a clear path for "on-chain" assets such as real estate, private equity, and bonds, promoting the accelerated development of the RWA field.

Losers: Arbitrageurs and non-mainstream assets

Offshore exchanges: Offshore platforms that rely on regulatory arbitrage are facing a sharp decline in their survival space. The case of OKX, which pleaded guilty and paid a fine in February 2025, highlights the risks of serving US users – for these platforms, the US market has become "more risk than reward."

Algorithmic Stablecoins: The vision of “uncollateralized currency” has been completely dashed. Due to their inability to meet the “1:1 liquidity reserve endorsement” requirement, algorithmic stablecoins are effectively banned in the US market.

Privacy coins: Anonymous assets such as Monero and Zcash directly conflict with AML/KYC regulations and are gradually being removed from regulated platforms, becoming the "junk bonds of cryptocurrencies" - trading only on the fringe of the market and extremely risky.

DeFi at a Crossroads

DeFi is facing two choices:

Compliant DeFi (RegDeFi): Integrate KYC/AML functions in smart contracts or front-ends to meet the needs of institutional participation;

“Wild West”: Adheres to the “no permission required” attribute, but is isolated from mainstream liquidity.

Regulators don't buy into the idea that "complete decentralization means unregulatable." As the Bank for International Settlements (BIS) points out in its "decentralization illusion," nearly all DeFi projects have "pressure points" (such as governance token holders, core developers, and web interfaces) that can be targeted for regulation.

This regulatory pressure also creates room for regulatory capture: deep-pocketed giants like Coinbase, Wall Street banks, and asset management firms are in the best position to influence rulemaking. The risk is that regulation could become a barrier to entry, excluding smaller innovators. For example, Coinbase's lobbying for stablecoin legislation (which could be detrimental to Tether) demonstrates this trend of giants dictating the rules.

New risks: hidden dangers of systemic connections

The deeper risk lies in "systemic interconnectedness." While the old regulatory system was chaotic, it maintained a firewall: when FTX collapsed, the risk spread was largely confined to the cryptocurrency sector. The new framework, however, has torn down that wall—banks are involved in custody, stablecoins are integrated into payment channels, and ETFs are directly linking cryptocurrencies to retirement portfolios.

This means that risks in the cryptocurrency sector are no longer isolated: failures in the custody departments of major banks, systemic ETF failures, and the sudden collapse of regulated stablecoins can all trigger chain reactions in traditional markets. Ironically, the very rules designed to make cryptocurrency safer have actually tied it even more tightly to the traditional financial system. While the house may have been rebuilt, the foundation is still deeply intertwined with traditional finance; a tremor in one area is felt throughout.

Looking Ahead: Three Possible Paths to 2026 and Beyond

The stage is set for the regulatory shift in 2025, but the drama is still unfolding. As the dust settles, three paths seem most likely:

Big integration (most likely)

The United States has successfully integrated cryptocurrencies into its financial system. By 2026, a safe harbor for token issuance will be in place, and the SEC and CFTC will finalize registration rules for digital asset intermediaries. Compliant US dollar stablecoins under the GENIUS Act will become mainstream payment channels, integrated into fintech applications and traditional banking operations. Bitcoin and Ethereum spot ETPs will become a regular part of investment portfolios, with banks and asset managers offering custody and investment products on a large scale. The market will concentrate on a small number of large, compliant exchanges, and DeFi will establish an "institutional-grade RegDeFi" sector through the integration of KYC/AML procedures. Leveraging the depth of the US capital market, this framework will become the global default standard, with other jurisdictions gradually aligning with it to maintain market access.

A fragmented world (medium likelihood)

The US may be stalled by internal obstacles: political deadlock, legal proceedings, and the SEC-CFTC power struggle could lead to a fragmented and difficult-to-enforce regulatory framework. The EU, with its unified MiCA rules, could then become a core hub for "large-scale, compliant crypto businesses," while Singapore and Hong Kong will continue to attract high-growth projects with their flexible sandbox mechanisms. Ultimately, this could leave three independent regulatory tracks globally, fragmenting the market and minimizing interoperability. Companies will need to separate their operations by region and adapt to different rules.

Decentralized revival (small probability)

Excessive centralization can backfire: If regulation heavily favors traditional financial giants, recreating the inefficiencies of Wall Street's "high fees, low selection" model, developers and users may exit the mainstream ecosystem en masse. Breakthroughs in zero-knowledge proofs, decentralized identity, and cross-chain technology could catalyze the emergence of a "censorship-resistant parallel economy"—one that doesn't replace the regulatory system but rather operates alongside it, providing users with the "sovereignty and resilience" of a single nation's oversight and becoming a new vehicle for the decentralized ideals of cryptocurrency.

Conclusion: The era of large-scale integration has officially begun

The significance of the regulatory shift varies greatly depending on one’s stance: for the public, it is about security and stability; for investors, it means legitimacy and market access; for industry developers, it is a long-awaited clear roadmap; for policymakers, it is a geopolitical strategy to reshape the global dominance of US fintech.

These perspectives converge on a common theme: the grand integration of cryptocurrency and the core of the US financial system has officially begun. The risks (such as systemic interconnectedness), contradictions (the clash between decentralized ideals and traditional financial rules), and countercurrents (the potential for a decentralized resurgence) inherent in this integration will collectively shape the next phase of the cryptocurrency industry's development.