Written by: David, TechFlow

On July 31, the new SEC Chairman Paul Atkins delivered a speech titled 《American Leadership in the Digital Finance Revolution》, announcing a brand new plan called "Project Crypto".

Although this news has not yet made the mainstream media headlines, it may become one of the most far-reaching events for the crypto industry in 2025.

In January, when Trump returned to the White House, he boldly declared that he would make the United States the "world's cryptocurrency capital". At the time, many viewed this as campaign rhetoric, and the entire industry was waiting to see if Trump's promise was just an empty check.

Yesterday, the answer was revealed.

This Project Crypto appears to be the first important implementation of Trump's crypto-friendly policy.

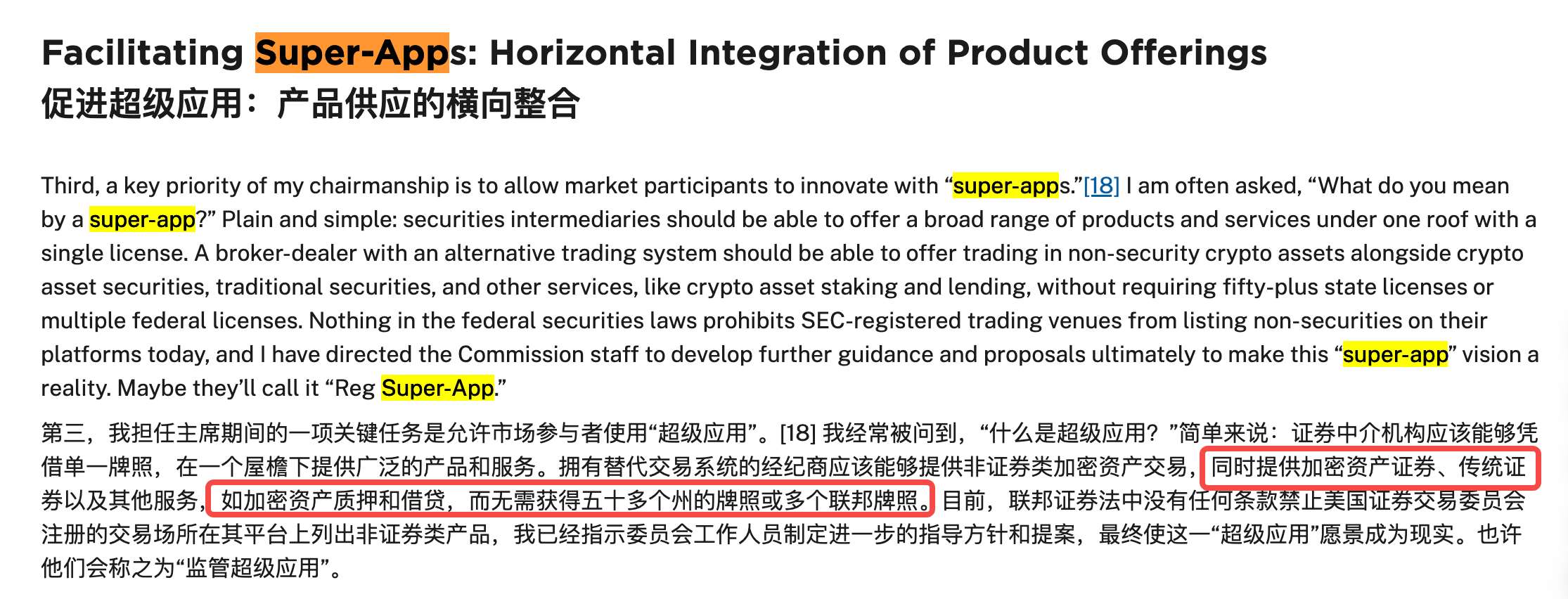

Currently, there are many detailed interpretations of this plan on social media, which I will not elaborate on; but I believe the most valuable part is that it allows financial institutions to create "super apps" that provide all financial services simultaneously on one platform, including traditional stock trading, cryptocurrency, and DeFi services.

What would it mean if JPMorgan's app could buy stocks, trade Bitcoin, and participate in DeFi mining?

From campaign promises to regulatory actions, from "enforcement is regulation" to "embracing on-chain finance" - this transformation took only 6 months. When the world's largest capital market decides to turn comprehensively, the entire industry's competitive landscape may be rewritten.

Super App's All-in-One

The super app concept in Atkins' speech might first remind you of WeChat. Chatting, payment, investment, insurance purchase, even loan application - all needs solved in one app.

This experience common in China is impossible in the United States, which prides itself on a free market.

The reason is simple: regulatory barriers.

In the United States, payment requires a payment license, securities require a broker license, loans require a bank license, with different requirements in each state.

Project Crypto breaks this deadlock for the first time.

According to the new rules, a platform with a broker's license can simultaneously provide traditional stock trading, cryptocurrency trading, DeFi lending services, NFT trading markets, stablecoin payment functions - all of these with just a unified license framework.

In the crypto industry, this unified framework's additional benefit is its alignment with the composability of many products.

You can automatically buy Bitcoin with stock returns, borrow stablecoins using NFTs as collateral, then invest stablecoins in DeFi for returns... all operations completed on one interface, with assets freely circulating on-chain.

When users can freely navigate on one platform, the Web3 super financial platform doesn't seem so far-fetched.

And the SEC's decision is equivalent to firing the starting gun of an arms race.

Three Types of Players, Diverging Fates

[The translation continues in the same manner, maintaining the specified translations for specific terms and preserving the original structure and meaning.]Once again, it's the old topic of liquidity.

In the financial world, liquidity is everything. In the era of super apps, this truth has been amplified many times over.

Users expect: transactions of any asset, at any time, and of any scale can be completed instantly. This requires accessing all major trading venues, aggregating global liquidity, and providing the best prices. More importantly, capital efficiency—how the same funds can efficiently flow between stocks, crypto, and DeFi.

Finally, user experience.

This might be the most underestimated competitive dimension. When functions are similar and fees are close, experience determines everything.

The difficulty lies in the huge differences in service targets. You need to satisfy crypto veterans (who want self-custody and to view on-chain data), while also reassuring traditional users (who don't even know what a seed phrase is). One app, two languages, which tests the product managers' balancing skills.

Overall, Project Crypto poses a challenge to practitioners: licenses determine what you can do, technology determines how well you can do it, liquidity determines how big you can do it, and experience determines how far you can go. In this multidimensional competitive chess game, every move could change the entire situation.

Potential Winners and Losers

Under the new Project Crypto policy, I know you want to know which enterprises and assets have better winning prospects.

But predicting the future is a dangerous game, and nothing is conclusive yet. Currently, we can only see some hints. The winners of the crypto super app era won't have just one face. Instead, we might see three completely different but equally successful models.

First, the "Alliance" model.

The smartest players have realized that collaboration is better than going solo.

Take Fidelity as an example, this giant managing $11 trillion in assets established a digital assets division as early as 2018, but has always been lukewarm in retail crypto trading.

What if Fidelity deeply integrates with a technologically leading crypto company (like Fireblocks)? Fidelity's 200 million clients would get a seamless crypto experience, while the partner gains the scarcest resources in traditional finance—trust and users. The result might not be a marriage between these two companies, but such "1+1>2" combinations will become common in the future.

Second, the "Arms Dealer" model.

During a gold rush, the most stable business is selling shovels.

In the super app era, "shovels" are key infrastructure. Take Chainalysis as an example, whoever wins the super app war will need its compliance tools. The beauty of these companies is that the more diverse their customers, the more stable their position. They don't need to choose sides because every side needs them.

Third, the "Specialization" model.

Not everyone needs a Swiss Army knife. If there's a financial platform specifically serving DAOs, or a vertical application focused on NFT financialization. While giants are busy building comprehensive platforms, these specialized players might capture long-tail value in niche markets.

The winners' approaches are nothing more than the above, but regarding losers, I think it's those mediocre institutions and speculators.

Take some regional banks in the US as an example: they have neither JPMorgan's resources for large-scale technological investment nor the flexibility of small fintech companies. When customers can get full crypto services at major banks, the survival space for these mid-sized institutions will be dramatically compressed.

As for speculators, in the past few years, many projects avoided regulation through complex legal structures—registering in the Cayman Islands, operating through DAOs, claiming to be "fully decentralized".

The clear rules of Project Crypto mean these gray areas will no longer exist. They must either be truly decentralized (accepting liquidity and user experience limitations) or fully compliant (accepting regulatory costs). Fence-sitters will have no place.

From a business competition perspective, the time window is closing rapidly.

First-mover advantage might be decisive in a winner-takes-all platform economy. Whoever can build a complete ecosystem in the next few months might become the next crypto financial giant.

An iPhone Moment?

In 2007, when Jobs demonstrated the first-generation iPhone, Nokia executives scoffed—how could a phone without a keyboard possibly succeed? 18 months later, the entire mobile phone industry's rules were completely rewritten.

Project Crypto might be the "iPhone launch" of crypto finance.

Not because it's perfect, but because it's the first time mainstream financial institutions saw the possibility: financial services can be provided like this, traditional and crypto assets can be integrated like this, compliance and innovation can be balanced like this.

But remember, the iPhone didn't truly change the world in 2007, but after the App Store appeared. Project Crypto is just the beginning; the real revolution will erupt after the ecosystem forms.

When hundreds of millions of developers start innovating on the new platform, when billions of users get used to on-chain finance, that will be the good days.

Drawing conclusions now would be premature.