Written by: thiccy

Translated by: AididiaoJP, Foresight News

The Era of High-Risk Speculation

(The article contains a few mathematical calculations, but the logic is clear and easy to understand.)

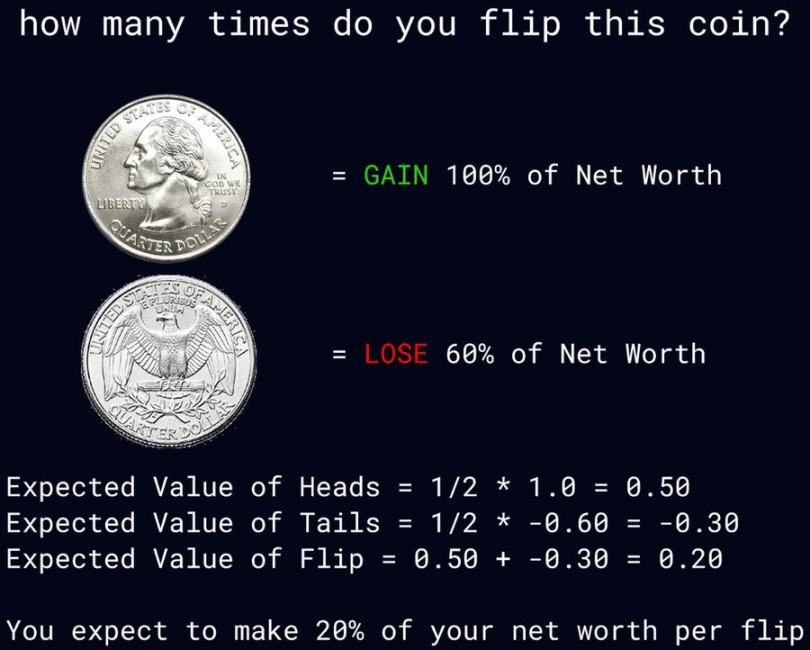

Imagine you participate in this coin-tossing game. How many times would you toss? The rules are: if it's heads, your assets grow by 100%; if it's tails, your assets lose 60%

At first glance, this game seems like a money-printing machine. Each coin toss has a positive expected value of 20%, meaning that with each coin toss, your assets are expected to grow by 20%. Theoretically, if you toss the coin enough times, you could accumulate the world's wealth.

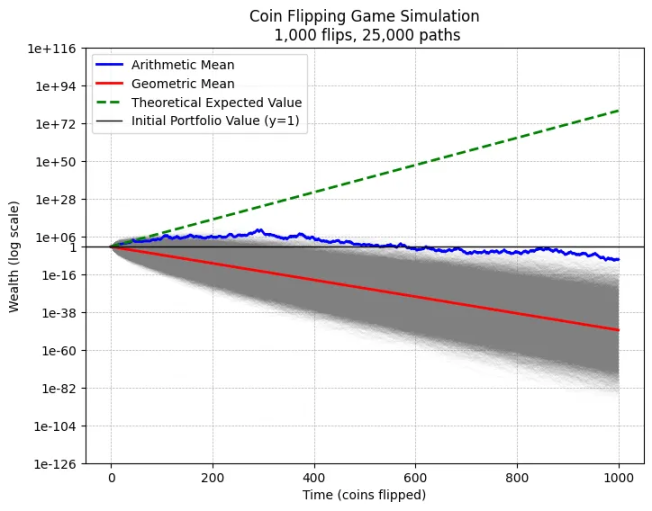

However, the reality is that if we simulate 25,000 people each tossing a coin 1,000 times, almost everyone will end up at zero.

This result is due to the multiplicative effect of repeated coin tosses. Although the game's expected value (arithmetic mean) is a 20% positive return each time, the geometric mean is negative, which means that in the long term, the compound interest of this game is actually negative.

How to understand this? Here's an intuitive explanation:

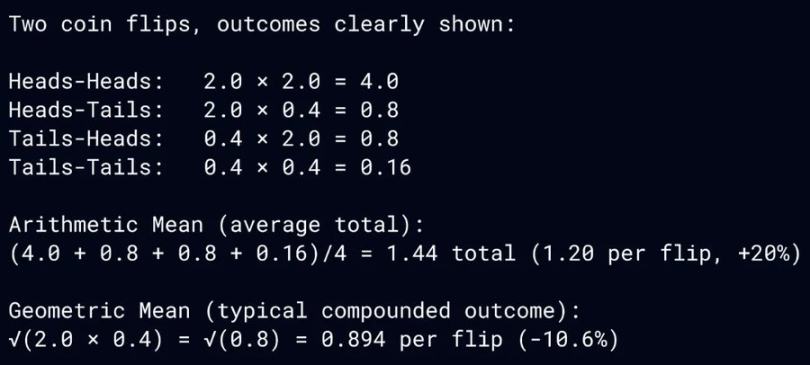

The arithmetic mean measures the average wealth created by all possible outcomes. In this coin-tossing game, wealth is highly concentrated in scenarios that are almost impossible to achieve consecutive heads. The geometric mean measures the wealth level corresponding to the median result.

The above simulation reveals the difference between the two. Almost all paths will end at zero. In this game, you need to toss 570 heads and 430 tails just to break even. After 1,000 tosses, all expected values are concentrated in the extremely rare results of 0.0001% consecutive heads, that is, those extremely rare situations of consecutive heads.

The difference between the arithmetic mean and geometric mean forms what is called the jackpot paradox. Physicists call it the ergodicity problem, and traders call it volatility decay. When the expected value is locked in extremely low-probability events, it is basically impossible to realize. Chasing low-probability events excessively will cause volatility to turn a positive expected value into a path to zero.

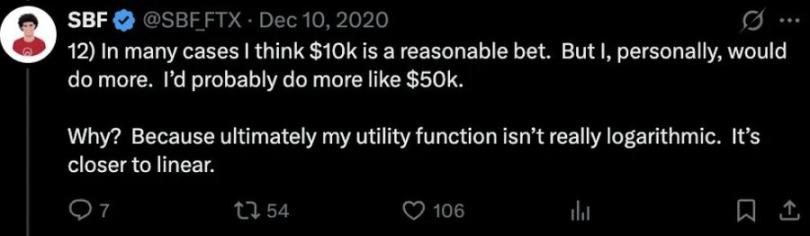

The crypto culture of the early 2020s is a vivid example of the jackpot paradox. SBF once tweeted about wealth preference, initiating this conversation:

Logarithmic wealth preference: Each dollar is worth less than the previous one, and risk appetite decreases as capital grows.

Linear wealth preference: Each dollar has the same value, maintaining the same risk appetite regardless of how much has been gained.

SBF proudly claimed to have a linear wealth preference. Since he planned to donate all his wealth, he believed that doubling from $10 billion to $20 billion was as important as earning $10 billion from zero, so high-risk, high-return was reasonable.

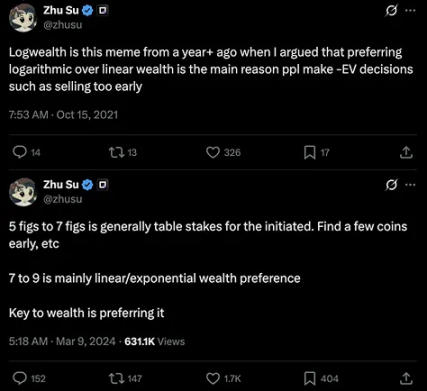

Three Arrows Capital founder Su Zhu also agreed with linear wealth preference and further proposed exponential wealth preference:

Exponential wealth preference: Each dollar is worth more than the previous one, and risk appetite increases with capital growth, and is willing to pay a premium for extremely low-probability events.

How do these three wealth preferences manifest in our coin-tossing game? According to the jackpot paradox, SBF and Three Arrows Capital obviously would toss the coin infinitely, which is precisely how they initially accumulated wealth. Unsurprisingly, SBF and Three Arrows Capital ultimately vaporized billions of dollars. Perhaps in a parallel universe, they are already trillionaires, proving the rationality of their adventurousness.

These liquidation events are not only cautionary tales of risk management mathematics but also reflect a deeper cultural shift towards linear and exponential wealth preferences.

Founders are expected to adopt linear wealth thinking, serving as cogs in the venture capital machine, placing heavy bets to maximize expected value. The stories of Elon Musk, Jeff Bezos, and Mark Zuckerberg betting everything and becoming global billionaires reinforce the myth driving the entire venture capital field, while survivorship bias easily masks millions of founders who end up at zero.

This preference for excess risk has permeated daily culture. Wage growth severely lags behind capital compounding, causing ordinary people to increasingly pin their real upward mobility on the jackpot with negative expected value. Online gambling, zero-day options, meme stocks, sports betting, and crypto meme coins are all examples of exponential wealth preference. Technology has made speculation more widespread, and social media spreads every get-rich-quick story, luring the masses into a massive, inevitable losing game like moths to a flame.

We are becoming a culture that worships the jackpot and prices survival cost at zero.

Artificial intelligence further exacerbates this trend by further devaluing labor and intensifying winner-take-all outcomes. The AGI abundance world dreamed of by tech optimists, where humans devote themselves to art and leisure, is more likely to be billions of people chasing zero-sum capital and jackpots with UBI subsidies. Perhaps "always rising" should be redesigned to reflect the blizzard experienced by those paths to zero—this is the true contour of the jackpot era.

In its most extreme form, capitalism behaves like a collectivist hive. The mathematics of the jackpot paradox shows that civilization reasonably sacrifices millions of worker bees to maximize the linear expected value of the group. This might be most efficient for overall growth but is cruel to the worker bees.

Marc Andreessen's technological optimism manifesto warns: "Humans should not be caged; humans should be useful, productive, and dignified."

But the rapid development of technology and increasingly radical risk appetite are pushing us towards the very outcome he warned about. In the jackpot era, growth is fueled by caging one's own kind. Usefulness, productivity, and dignity are increasingly limited to the few privileged classes who win the competition. We have enhanced the average at the cost of the median, leading to widening gaps in liquidity, status, and dignity, breeding an economic body of zero-sum cultural phenomena. These externalities manifest as social unrest, starting with the election of agitators and ending in violent revolutions, which are costly to civilization's compound growth.

As someone who makes a living trading in the crypto market, I have personally witnessed the decay and despair spawned by this cultural transformation. My victories are built on the bodies of thousands of other traders, a monument to wasted human potential.

When industry insiders seek trading advice from me, I almost always discover the same pattern: they take excessive risks and have deep drawdowns. The deep-seated reason is usually a scarcity mindset: an anxiety of "falling behind" and an impulse to quickly turn things around.

My answer has always been consistent: build more advantages, not increase risk. Don't commit suicide chasing jackpots. Logarithmic wealth is key. Maximize the median result. Create your own opportunities, avoid drawdowns, and you will succeed one day.

But most people will never establish a sustainable advantage. "Winning more" is not scalable advice, and in this competition of technological feudalism, meaning and purpose become winner-take-all. This brings us back to meaning itself. Perhaps we need a revival of some religion, reconciling ancient spiritual doctrines with modern technological reality.

Christianity spread because it promised universal salvation. Buddhism spread by declaring that everyone can attain enlightenment.

The modern version must similarly provide dignity, purpose, and alternative paths for everyone, lest they self-destruct in pursuit of the jackpot.

The Psychology of the High-Risk Speculative Era

This obsession with the jackpot has profound psychological roots. The human brain has evolved a strong preference for instant rewards, a mechanism that aided survival during the hunting and gathering era but has become a trap in the modern financial environment. The dopamine system is abnormally sensitive to potential high returns, even when the actual probability is extremely low. Neuroscience research shows that when people fantasize about winning big, the brain's activation pattern is almost identical to when actually receiving small, guaranteed continuous rewards.

Social media and financial technology products cleverly exploit these neural mechanisms. Infinite scrolling information feeds, instant trade execution, and dazzling profit displays create a perfect addictive cycle. Each success story is algorithmically amplified, while countless failure cases are quietly filtered out. This distorted information environment reinforces the illusion that "the next one could be me".

The Failure of the Education System

The modern education system, to some extent, fosters this jackpot mentality. Standardized testing and elite selection mechanisms are essentially winner-takes-all competitions, instilling in students from a young age a "all or nothing" mindset. The star effect in fields like arts and sports further reinforces this concept. When young people enter society, they are already accustomed to defining success as extreme outcomes, rather than gradual accumulation.

University education is increasingly viewed as a lottery, where a few people obtain massive returns through elite school halos, while most carry heavy loans with limited returns. This structure naturally guides people to seek other forms of "lottery" - whether in cryptocurrencies, internet celebrity economy, or startup fever.

The Financial System's Contribution

The modern financial system is technically the perfect engine of jackpot culture. Zero-commission trading, leverage products, and derivatives allow ordinary people to engage in speculative behaviors once reserved for professional institutions. Algorithmic market makers and dark pool trading create an illusion of liquidity, masking the essentially zero-sum nature of the game.

The venture capital industry has even institutionalized the jackpot logic. Successful funds often rely on a few hundred-fold return projects to compensate for most failed investments. This model is revered, with few questioning its long-term impact on the innovation ecosystem. When all resources chase potential unicorns, stable companies creating moderate returns are left unsupported.

The Collapse of Social Mobility

The prevalence of jackpot culture is closely related to declining social mobility. When opportunities for class advancement through traditional paths (education, career progression) decrease, extreme speculation naturally becomes an alternative choice. The financialization of the real estate market has transformed housing from a basic need into a speculative tool, further intensifying this trend.

The widening intergenerational wealth gap creates a vicious cycle: young people without family wealth are more inclined to high-risk behaviors, which in turn leads to greater wealth disparity. When the social safety net is weak, people's tolerance for "all or nothing" bets abnormally increases.

The Dilemma of Technological Accelerationism

The current narrative of technological accelerationism forms a dangerous resonance with jackpot culture. The blind worship of exponential growth ignores the fundamental limitations of physical and social systems. When every startup claims to "change the world", the actual output is often zero-sum or negative-sum financial engineering.

This is especially evident in blockchain and AI fields. Most projects do not create substantial value but attract capital through complex tokenomics and arbitrage opportunities. The result of this technological financialization is a bubble-filled ecosystem where genuine innovation struggles to obtain resources and attention.

Possible Solutions

To reverse jackpot culture, reforms are needed at multiple levels:

Financial Regulation: Limit the accessibility of leverage and speculative products, and strengthen behavioral oversight of financial technology.

Educational Reform: Cultivate students' probabilistic thinking and long-term planning abilities, reducing excessive emphasis on rankings.

Tax Policy: Impose heavy taxes on short-term capital gains, encouraging long-term investment.

Media Responsibility: Require social media platforms to balance the display of speculative risks and returns.

Social Security: Establish a more comprehensive safety net to reduce economic pressures that drive risky behavior.

Ultimately, we need to redefine the standards of success. A healthy society should reward continuous value creation, not occasional lucky breakthroughs. This requires a comprehensive transformation from individual mindset to institutional design, and is a difficult long march against deep-seated psychological biases.