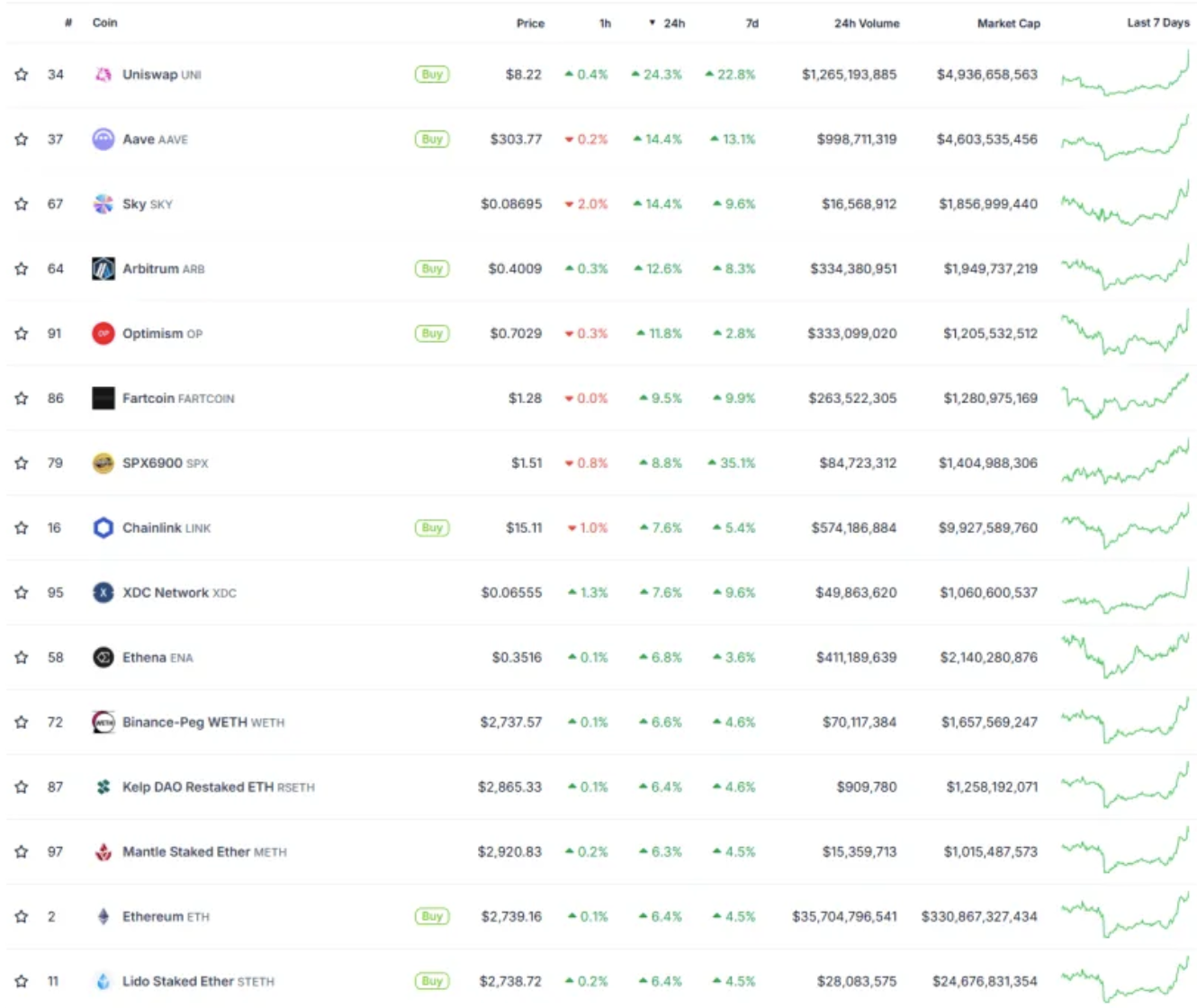

Yesterday, ETH and ecological blue-chip targets saw a surge in price, with ETH up 6.4%, UNI up 24.4%, AAVE up 13.1%, and ENA up 6.6%, which we mentioned in previous research reports. This round of Trend Research combines knowledge and action. From the opening of a position at $1,400 to the present, we are optimistic about and increase holdings of ETH-related targets, and recently purchased ETH call options, becoming the first secondary investment institution in the entire network to openly be optimistic and publicly disclose its position address.

At present, we are still optimistic about the underlying logic of ETH: the Trump administration is committed to establishing a stablecoin system, using the decentralized and on-chain characteristics of blockchain to absorb M2 liquidity from other countries in the world, thereby increasing the demand for US debt. To this end, the Trump administration has relaxed macro-regulation on encryption, promoted the implementation of regulatory measures, and regulated encryption from all aspects to accommodate more funds. The most important facility for stablecoins and on-chain finance (DeFi) is Ethereum. The influx of stablecoins and the continued development of RWA will bring further prosperity to DeFi, promote the increase in Ethereum consumption and GAS revenue, and push up its market value.

1. Continued Optimism about Crypto Regulation

1. Changes in the concept of crypto regulation

The Trump administration is crypto-friendly. John Atkins, chairman of the SEC who took office in April 2025, has clearly promoted the transformation of crypto asset regulation.

1. Public statement on streamlining the process

· Rules take precedence over enforcement: Atkins criticized his predecessor’s model of “defining compliance through litigation” and stressed that clear and predictable rules will be formulated to reduce industry uncertainty.

Classification and regulatory framework: It is planned to release token classification standards within 90 days and establish a "safe harbor" system for compliant projects.

2. Long-term policy direction

· On-chain securities compliance: Atkins proposed exploring the “listing of on-chain securities trading platforms” in May 2025, which may restructure the issuance and trading processes.

· Cross-departmental collaboration: Plan to work with the CFTC and FTC to establish a joint regulatory framework to reduce jurisdictional conflicts.

DeFi is in line with America’s core values and will introduce an “innovation exemption” framework.

(II) Further improvement and relaxation of the crypto regulatory framework

1. CLARITY Act

The CLARITY Act aims to build a structural regulatory bill for the crypto market, effectively solving the problem of regulating the digital asset market with a scale of 3.3 trillion US dollars. Its regulatory goals are to clarify asset classification, distinguish between security tokens (regulated by the SEC), commodity tokens (regulated by the CFTC), and licensed payment stablecoins, and solve the long-standing controversial "securities or commodities" identification problem. The second is to standardize institutional supervision, requiring financial institutions that custody digital assets to meet capital reserve and segregate customer funds requirements to prevent risks similar to FTX. The bill was passed by the U.S. House of Representatives Committee on June 11, 2025 with 47 votes in favor and 6 votes against, and will be transferred to the House Financial Services Committee for the next stage of review.

According to the bill, mainstream cryptocurrencies such as Bitcoin and Ethereum are commodity tokens, while company equity tokens (representing company ownership and enjoying voting rights or dividend rights), bond tokens (promising fixed interest returns), and DeFi governance tokens with income rights and dividends (relying on the project party to continue operating) are security tokens. This will change the previous state of ambiguity, unclear law enforcement, and confusion. The clarification of rights, responsibilities and obligations will help promote the prosperity of DeFi platforms.

The probability that mainstream infrastructure tokens like SOL may be identified as commodities is increasing. On June 11, the SEC has asked potential Solana ETF issuers to submit a revised S-1 form within the next week. The SEC said it will provide feedback on the S-1 form within 30 days of submission. This shows that regulators are relaxing and accelerating their recognition of crypto commodities.

2. Genius Act

The Genius Act aims to fill the regulatory gap of stablecoins, strengthen the world currency status of the US dollar, and solve the dilemma of US debt demand. This is the first comprehensive regulatory framework for stablecoins at the federal level, clarifying the qualifications of issuers, reserve requirements and operating specifications. It is mandatory to anchor stablecoins to the US dollar at a 1:1 ratio, promote the penetration of the US dollar into the global crypto economy and cross-border payment fields through stablecoins, and consolidate the dominance of the US dollar in international finance. Through mandatory reserve rules (requiring reserve assets to be short-term US debt or cash), structural demand is created for the US debt market, easing US fiscal pressure.

In the past few years, stablecoins USDT and USDC have repeatedly been reported to have regulatory risks and redemption risks, resulting in more than 10% depegging. If they can be included in federal supervision, it will undoubtedly help to strengthen the security and credit of stablecoins. At the same time, after the federal legislative attitude is clear, more issuers will participate in the issuance of stablecoins and attract more funds to enter the crypto market. Standard Chartered Bank predicts that after the bill is passed, the scale of stablecoins may increase to US$2 trillion in 2028.

3. Statement on the relaxation of regulation on the issuance, custody and trading of crypto assets

SEC Chairman Atkins mentioned in his speech that more relaxed supervision will be implemented in the three key areas of crypto assets: issuance, custody and trading.

In terms of issuance, the SEC will formulate clear and reasonable guidelines for the issuance of crypto assets under securities or investment contracts. So far, only four crypto asset issuers have issued securities under Regulation A. Regulation A is a simplified issuance exemption mechanism for small projects proposed by the US Securities and Exchange Commission. Issuers below a certain amount can issue stocks and bonds through this mechanism. Since the biggest policy obstacle to the issuance of crypto assets is the unclear determination of whether the nature of the asset is a security and what type of security it is, issuers are worried that the issuance of crypto assets will violate the corresponding legal provisions, which has led to few projects using this rule. Atkins asked the staff of the Securities and Exchange Commission to consider whether the issuance of crypto assets in the United States can be smoothed through means such as business guidance, registration exemptions and safe harbors at the working level.

In terms of custody, registrants are supported to have greater autonomy in determining how to custody crypto assets. Investment advisors and fund companies can use self-custody solutions that are more advanced than current custodian technology to store crypto assets. This is mainly due to historical reasons. Traditional custodians are not well adapted to the needs of blockchain due to their lack of information technology.

In terms of trading, investors are supported to trade a wider range of products on trading platforms, which can provide trading of securities assets, non-securities assets, and even provide sales of other financial services. Staff have been asked to explore whether it is necessary to specify some guidelines or rules to allow crypto assets to be listed and traded on national securities trading platforms.

4. DeFi is expected to implement "innovation exemption"

SEC Chairman Paul S. Atkins made it clear at the "DeFi and the American Spirit" roundtable on June 9, 2025: "The basic principles of DeFi (economic freedom, private property rights, and disintermediation) are highly consistent with the core values of the United States. Blockchain technology is a revolutionary innovation, and the SEC should not hinder its development."

The SEC is developing conditional exemption rules for DeFi to quickly allow registered and unregistered parties to bring on-chain products and services to market. The innovation exemption can make the United States the "global crypto capital" by encouraging developers, entrepreneurs and other companies willing to comply with certain conditions to innovate on-chain technology in the United States.

UNI has been troubled by compliance issues before. Although it is the most important DEX on the chain, its price performance is not good. If the innovation exemption rules can be quickly applied, UNI may be expected to be the first beneficiary. This is also one of the important reasons why the price of the top DeFi coins rose sharply after the roundtable meeting.

5. Expected approval of Ethereum ETF pledge

On May 29, 2025, the U.S. Securities and Exchange Commission (SEC) Corporate Finance Division issued a statement clarifying that certain staking activities based on proof-of-stake (PoS) blockchain protocols do not constitute securities transactions. Atkins' speech at the "DeFi and the American Spirit" roundtable also further clarified that "voluntary participation in proof-of-work or proof-of-stake networks as "miners", "validators" or "staking as a service" providers is not within the scope of federal securities laws." And will promote the formulation of relevant regulations, which means that Ethereum's staking activities (including node self-staking and staking through service providers) will not be regarded as securities transactions if certain conditions are met, and it also paves the way for the currently approved Ethereum ETF to be pledged.

If the SEC approves an Ethereum ETF that includes staking income, institutional investors will be able to obtain ETH staking income through ETFs. ETH will become a "bond" in the crypto industry, and a huge amount of traditional institutional funds will legally flow into ETH. On the one hand, a large amount of ETH will be locked up by staking, which will further improve the decentralization and security of on-chain finance. On the other hand, compliant on-chain income will significantly increase the demand for ETH and push up prices.

From the above, it can be seen that the Trump administration is conducting more systematic and adaptive supervision of crypto assets and markets. The supervision is becoming clearer and more relaxed, encouraging blockchain innovation to attract more funds into crypto.

2. Ethereum is still the most important infrastructure for on-chain finance

The "DeFi" statement and the implementation of specific bills will break down compliance barriers in the future and open up channels for traditional funds to enter. Trillions of incremental funds will come to on-chain finance in the form of stablecoins, and the largest and safest "soil" for on-chain finance is Ethereum.

1. Ethereum Foundation promotes “Defipunk”

The Ethereum Foundation's 2030 plan clearly states that it will promote the establishment of a "Defipunk" evaluation mechanism and promote the relevant transformation of DeFi projects. The core content of "Defipunk" revolves around building a DeFi ecosystem that complies with the principles of Cypherpunk, aiming to protect user autonomy, privacy and anti-censorship through technical means.

The core principles of Defipunk include: First, security, giving priority to field-proven, tamper-proof and open-source technical architectures, and avoiding reliance on centralized trust mechanisms (such as multi-signatures or legal recourse). Second, financial sovereignty, emphasizing the user's complete control over assets, supporting permissionless self-hosted wallets and on-chain transactions, and reducing reliance on intermediaries. Third, technology takes precedence over trust, and de-trust is achieved through cryptographic tools and smart contracts, such as the use of technologies such as zero-knowledge proofs to enhance privacy protection. Fourth, open source and composability, promoting transparent code development, ensuring interoperability between protocols, and encouraging modular design to promote innovation.

The Ethereum Foundation has full expectations for the development of DeFi, and the Ethereum ecosystem is also vigorously developing DeFi-related businesses. Ethereum has the basic conditions to become a new generation of on-chain financial paradigm.

2. Current Status of Stablecoin Issuance and Distribution

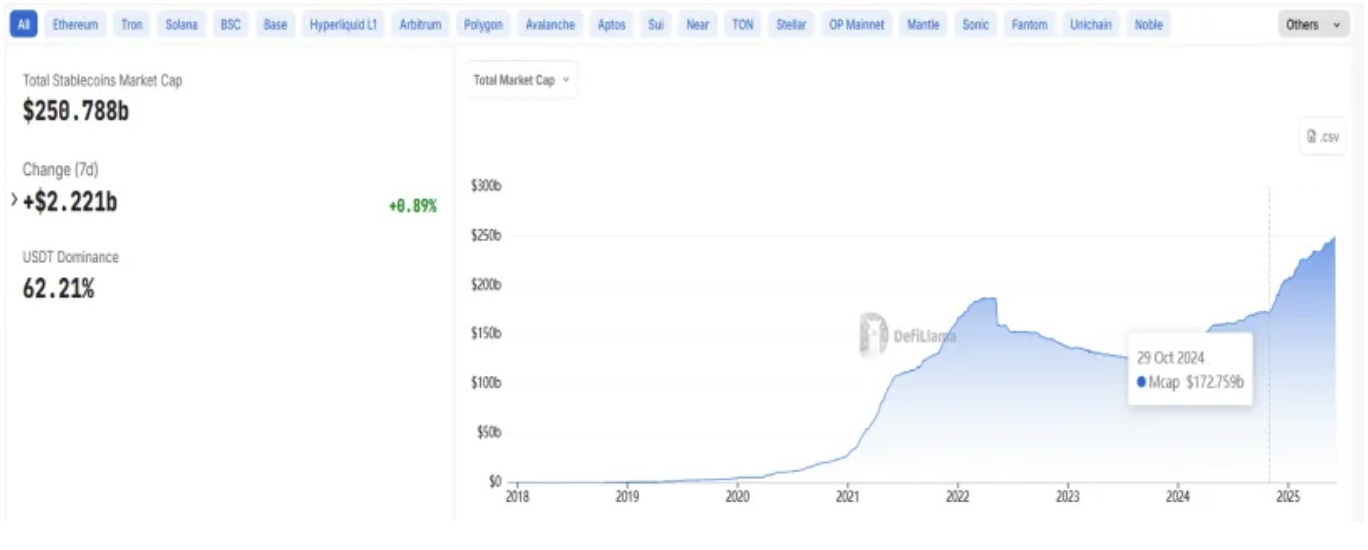

1. Total amount of stablecoins

Since Trump took office, the total amount of stablecoins has increased by about $76 billion, an increase of more than 40% in 7 months. This growth rate significantly exceeds the total amount and increase of stablecoins during the market recovery in 2023. In September 2023, the total amount of stablecoins reached the lowest market value in nearly four years, about $123.7 billion, and increased to $173.7 billion in November 2024, an increase of $50 billion, and an increase of about 40% in 13 months.

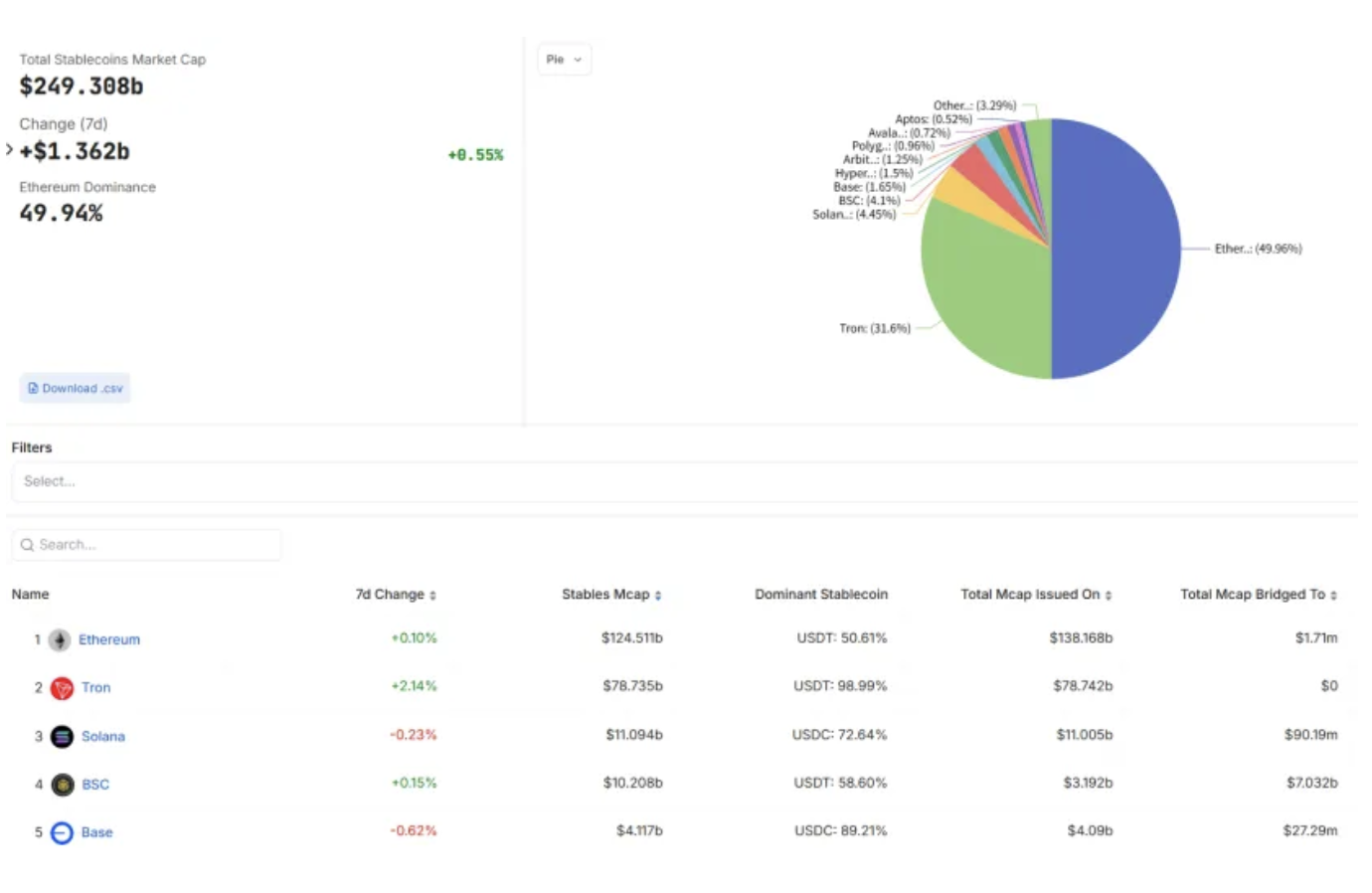

2. Current distribution of stablecoins on the chain

About 50% of stablecoins are in circulation on Ethereum, 31% on TRON, 4.5% on Solana chain, and 4% on BSC chain. Ethereum accounts for half of the stablecoin circulation.

3. Ecological status of major public chains and stablecoins in DeFi

From the comparison in the above figure, we can see that more than 50% of the funds on Ethereum are deposited in DeFi protocols, which has the largest DeFi TVL. Although Tron has a large number of stablecoins, they are mainly used for payment, with a small number of ecological protocols, and DeFi TVL accounts for only 6.5%. Although Solana and BSC have a relatively high proportion of DeFi TVL, their absolute values are small, and their DeFi infrastructure is generally mature. Based on the above, when the stablecoin bill is passed, Ethereum will most likely receive the largest amount of funds.

(II) Flow of New Stablecoins

It is currently speculated that the newly added stablecoins will have four flows:

1. Flowing to the DeFi market, which is native to the crypto market and has higher yields

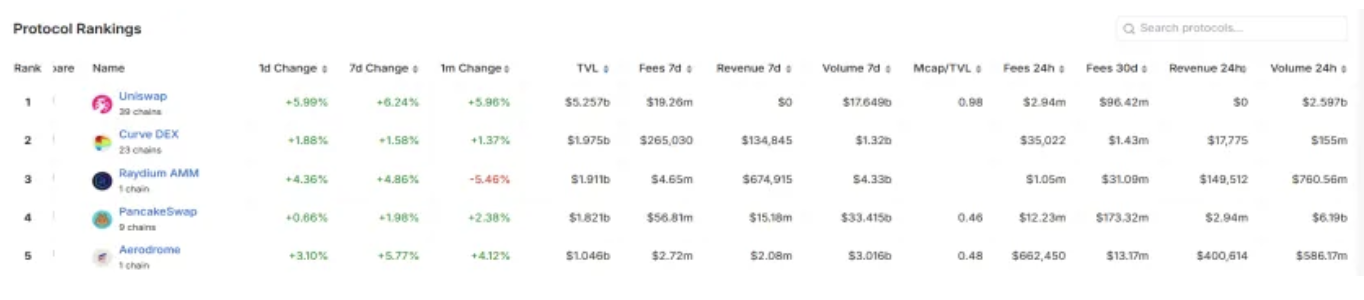

The high volatility of Crypto has led to many DeFi protocols on the chain that are far higher than the traditional financial market and easy to enter. As incremental stablecoins enter the chain, some funds will inevitably choose more intelligent, efficient, and profitable investment opportunities. Ethereum's high degree of decentralization, security, and scale will become the first choice for incremental funds to enter this part. Among them, UNI, as the largest on-chain Dex, and AAVE, as the largest on-chain lending protocol, are blue-chip targets that cannot be ignored. Small-cap DeFi protocols with good business data such as COMP are also worthy of attention.

Among DEXs, UNI is currently in a clear advantage, with a TVL of $5.1 billion, a 7-day trading volume of $17.6 billion, and a 7-day fee income of 19.26 million. Its TVL is significantly higher than other DEXs. Pancake is more special, with a 7-day trading volume of $33.4 billion and a 7-day fee income of 56.81 million. Its trading volume is significantly higher than UNI, mainly benefiting from Binance alpha wash trading.

In the lending sector, AAVE is in an absolute dominant position, with a TVL of 26.4 billion, 7-day fees of 11.68 million, and 7-day agreement income of 1.49 million. The TVL of the rest of the lending market is less than 5 billion US dollars.

2. Flow to the RWA market mainly built by US compliance institutions

Many traditional funds entering the chain will not participate too much in the market of Altcoin, but will enter the RWA market built by the leading institutions of this wave of financial innovation in the United States, such as the BUILD fund issued by BlackRock on the chain. The BUIDL fund mainly invests in:

· Cash: Highly liquid cash or cash equivalents to ensure the stability of the fund and the ability to redeem immediately;

· U.S. Treasury Bonds: Short-term U.S. Treasury bonds, as low-risk, high-credit-rated assets, provide a stable source of income.

· Repurchase Agreement: A short-term lending agreement, usually backed by Treasury bonds, that ensures liquidity and returns for the fund.

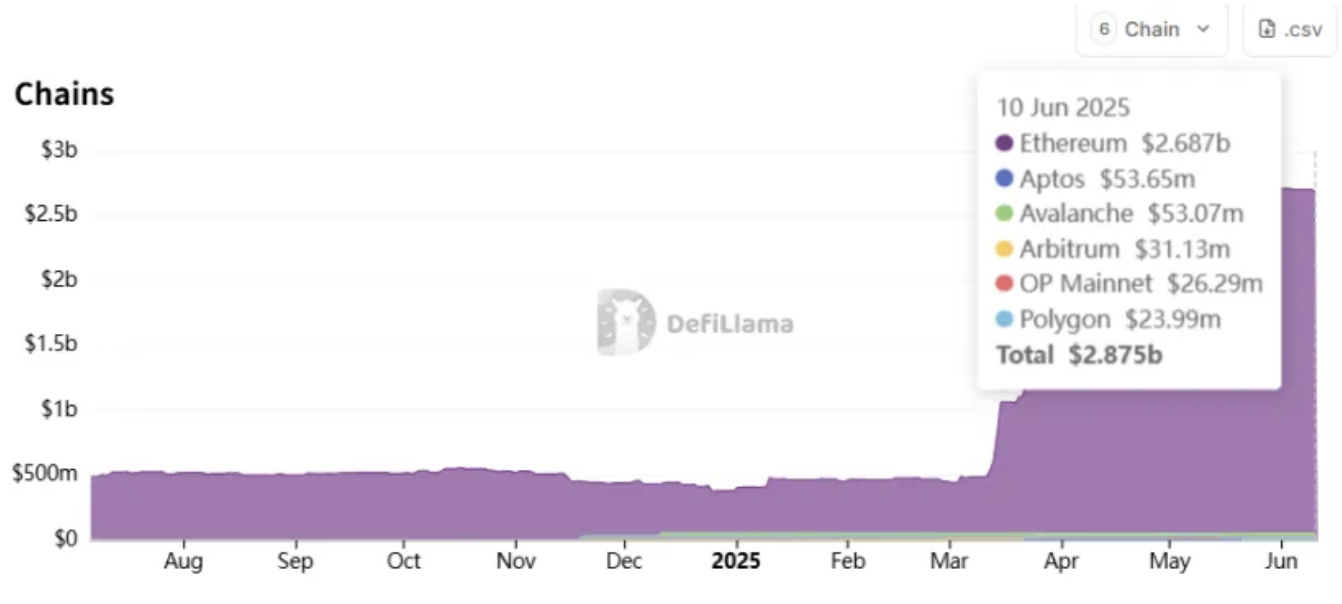

The combination of these assets aims to maintain a stable value of the BUIDL token (targeting $1/token) and distribute dividends to investors through daily accumulated earnings, which are distributed monthly in the form of new tokens. The fund is managed by BlackRock Financial Management, custodian is Bank of New York Mellon, and the tokenization platform is Securitize. The platform-managed TVL has grown rapidly in the past three months. In March 2025, TVL just exceeded $1 billion, and has now increased to $2.87 billion, an increase of 187%; of which $2.687 billion is on Ethereum, accounting for 93% of the total.

Native projects in the crypto are also paying close attention to the RWA market. Circle, the issuer of USDC, acquired Hashnote, the issuer of USYC, to make up for its shortcomings in RWA. Hashnote is a startup incubated by Cumberland Labs with an investment of US$5 million, focusing on tokenized US debt products. Its core product USYC (US YieldCoin) is anchored to short-term US Treasury bonds and had a scale of US$1.3 billion at the time of acquisition. Circle deeply binds USYC with USDC to create a closed loop of "cash + income assets" to meet the dual needs of institutions for on-chain collateral and income tools.

In addition to BUIDL and Circle, large RWA projects include ENA and ONDO. The problem with ENA is that it is mainly used for arbitrage of funding rates for crypto token contracts. The market size is limited by the size of transactions, and there is also a learning cost problem for funds outside the circle, so there has not been much growth in the past six months. ONDO has increased from 600 million to 1.3 billion since the beginning of 2025, an increase of about 116%. It can be seen that although the stablecoin bill has not been fully passed, debt tokenization has been ongoing. In addition, Chainlink is also very important in RWA. It is the largest oracle for the integration of off-chain assets on the chain and on-chain Defi.

3. Flow to the payment field to solve the efficiency of traditional finance

Traditional funds become stablecoins. One of the most important uses of blockchain is to solve payment problems, such as optimizing the traditional SWIFT payment system and improving transaction efficiency. For example, JPMorgan Chase's Kinexys platform (formerly Onyx) focuses on wholesale payments, cross-border payments, foreign exchange transactions and securities settlements. It supports multi-currency cross-border payments, reduces middlemen and settlement time. It provides tokenization functions for digital assets and explores payment scenarios for stablecoins and tokenized bonds. Kinexys is also based on the Ethereum technology stack, using its smart contracts and distributed ledger technology. Currently, Kinexys' average daily trading volume has exceeded US$2 billion.

4. Flowing to some crypto-native hype markets

A small amount of incremental funds will quickly flow into the crypto-native Altcoin speculation market.

In summary, compared with other on-chain ecosystems, Ethereum and its on-chain DeFi are the destinations with the largest increase in stablecoins. On-chain DeFi may usher in a new "DeFi Summer" in 2025 and further demand for pledges to promote network security. At the same time, the SEC's "DeFi" statement on June 10 may pave the way for ETF pledges for ETH. If successfully passed in the future, ETH will become a "bond" in the crypto market, triggering large-scale purchases. A series of changes may push ETH into a deflationary state again (the current annual inflation rate is 0.697%).

3. Open interest in the contract market hit a new high, and bearish sentiment remains; spot ETFs continue to flow in, and options are bullish

1. Contract positions hit a new high, and funds are active

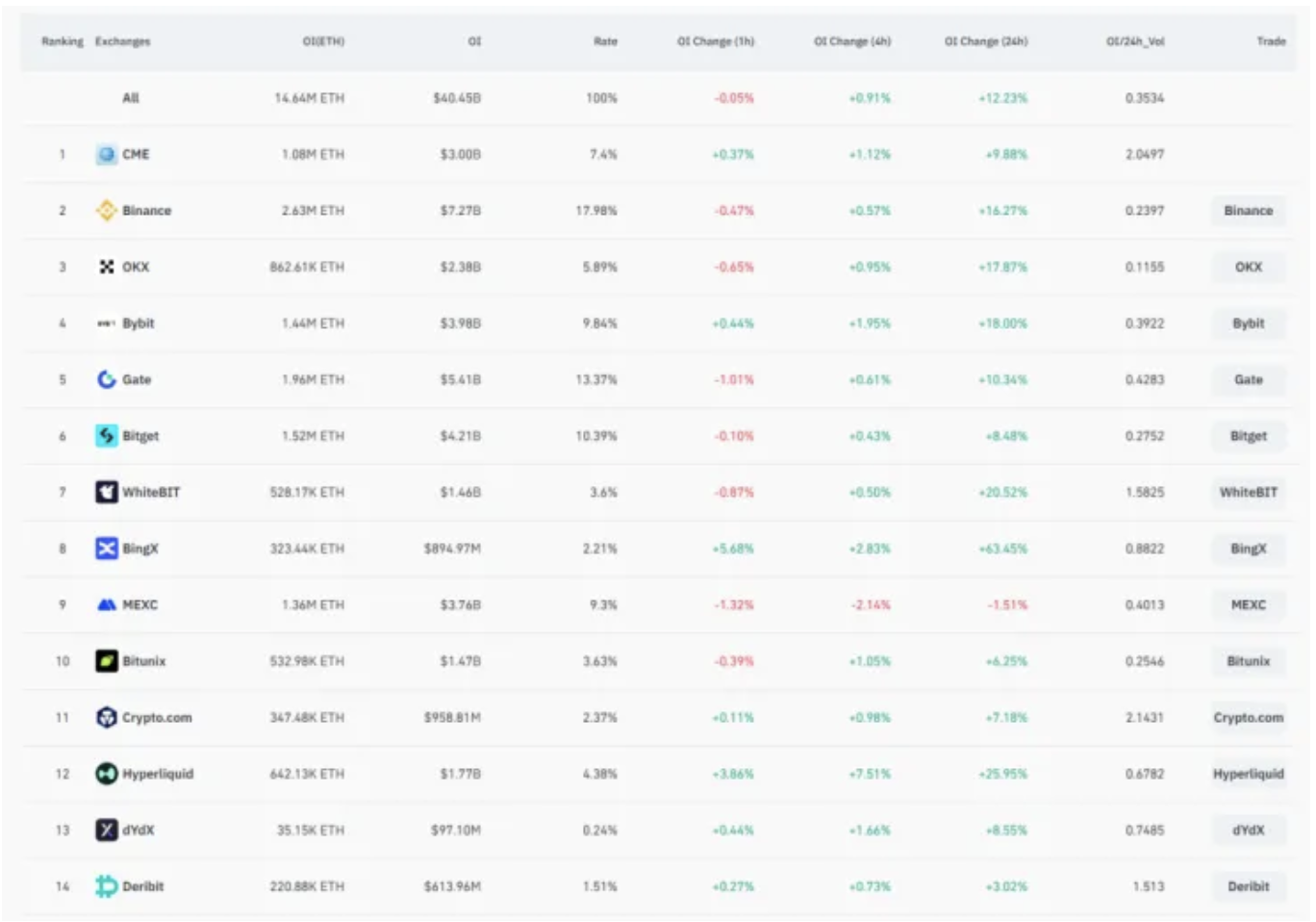

Currently, ETH is still about 40% away from its ATH, but the total network contract positions have reached a record high of US$37 billion, and the contract market liquidity is extremely good.

2. The peak of market sentiment has not yet arrived

At the same time, the current market sentiment has not reached its high point. The fear and greed index has just turned from neutral to greed. The high point of sentiment in the market has not yet arrived, and incremental funds outside the market have not yet begun to enter.

3. The number of short on trading platforms increased

Judging from the long-short ratio of contract positions on the trading platform, the ratio of long and short positions is continuously decreasing, and the number of short is increasing. At the same time, positions are continuously increasing, so the overall short positions are also increasing. However, the long-short ratio is still in a relatively balanced state, and the funding rate is relatively stable.

4. ETH spot positions on some trading platforms are lower than contract positions

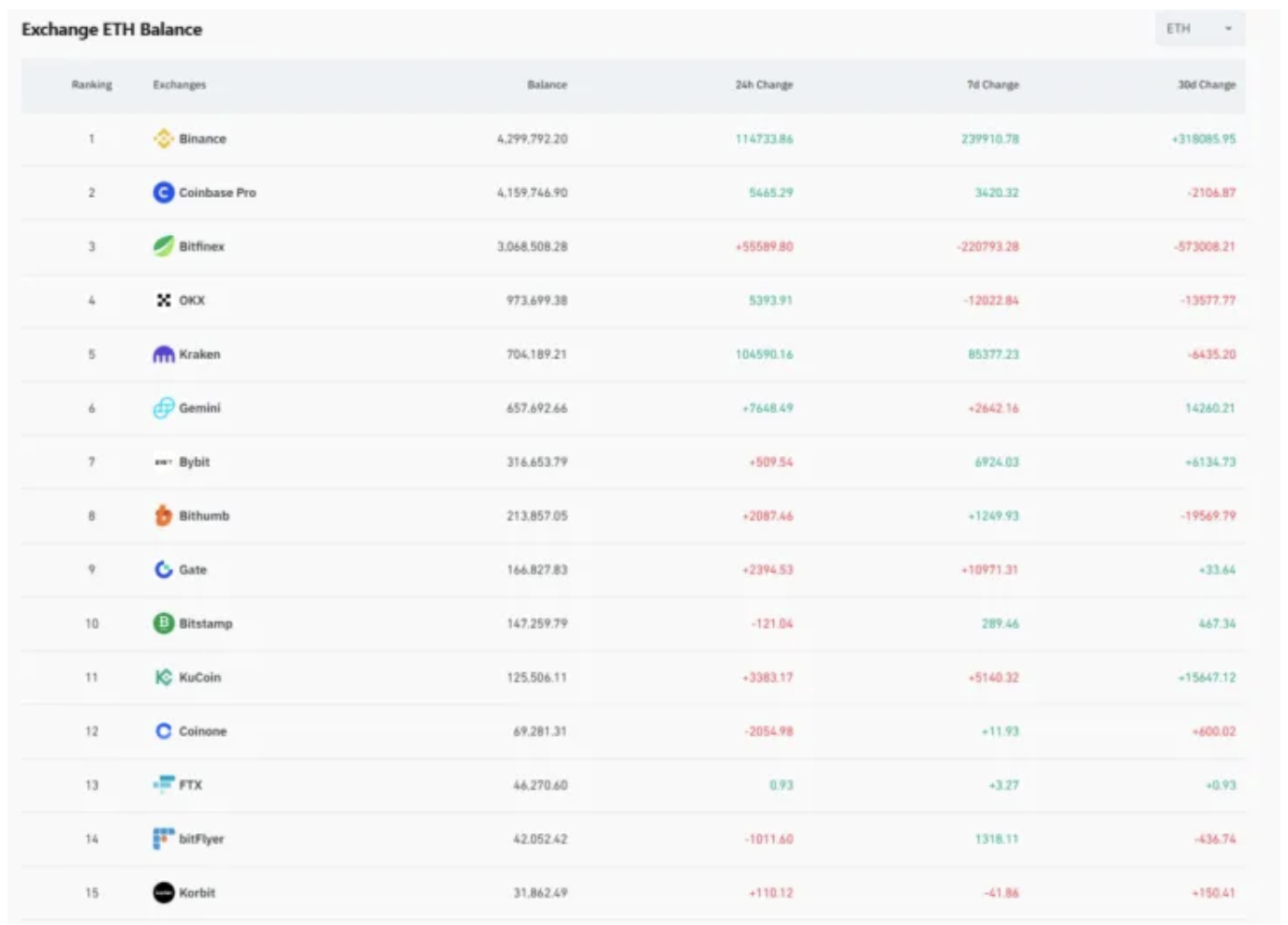

When the trend reversal research report was released in April, we observed that some trading platforms had ETH holdings far lower than the contract holdings of the trading platform. At present, this situation still exists. The Bybit trading platform holds 1.44 million coins, and the balance of the trading platform wallet is 316,000 coins, which is 4.5 times the balance; the Gate trading platform holds 1.96 million coins, and the balance of the trading platform wallet is 166,000 coins, which is 11.8 times the balance. The Bitget trading platform holds 1.52 million coins, but the balance of the trading platform wallet has not been disclosed yet.

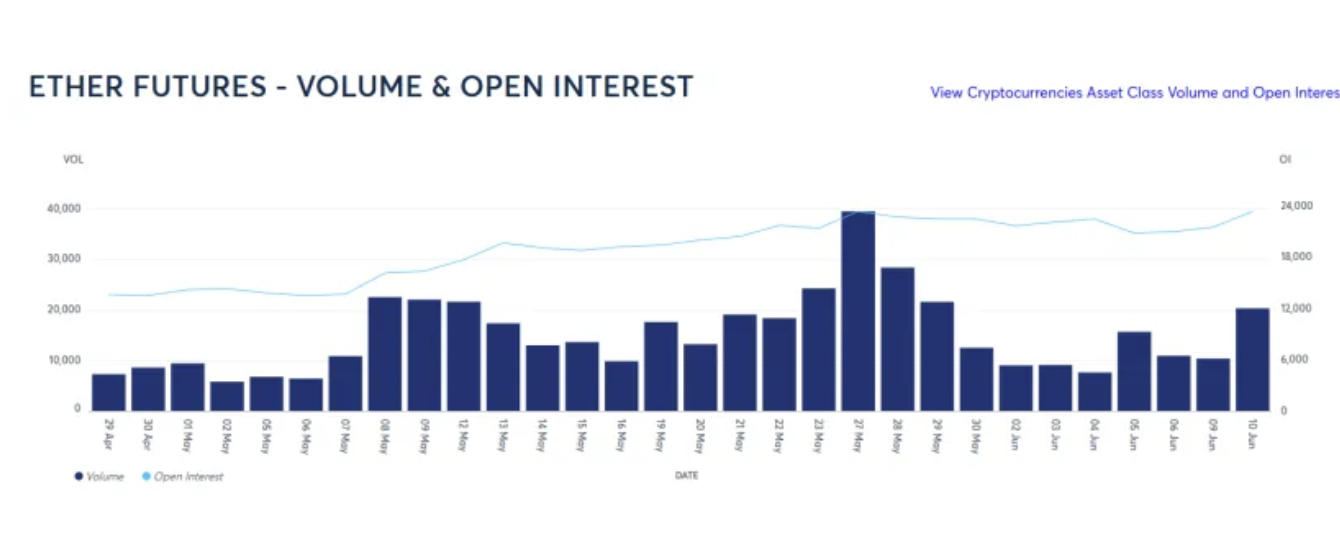

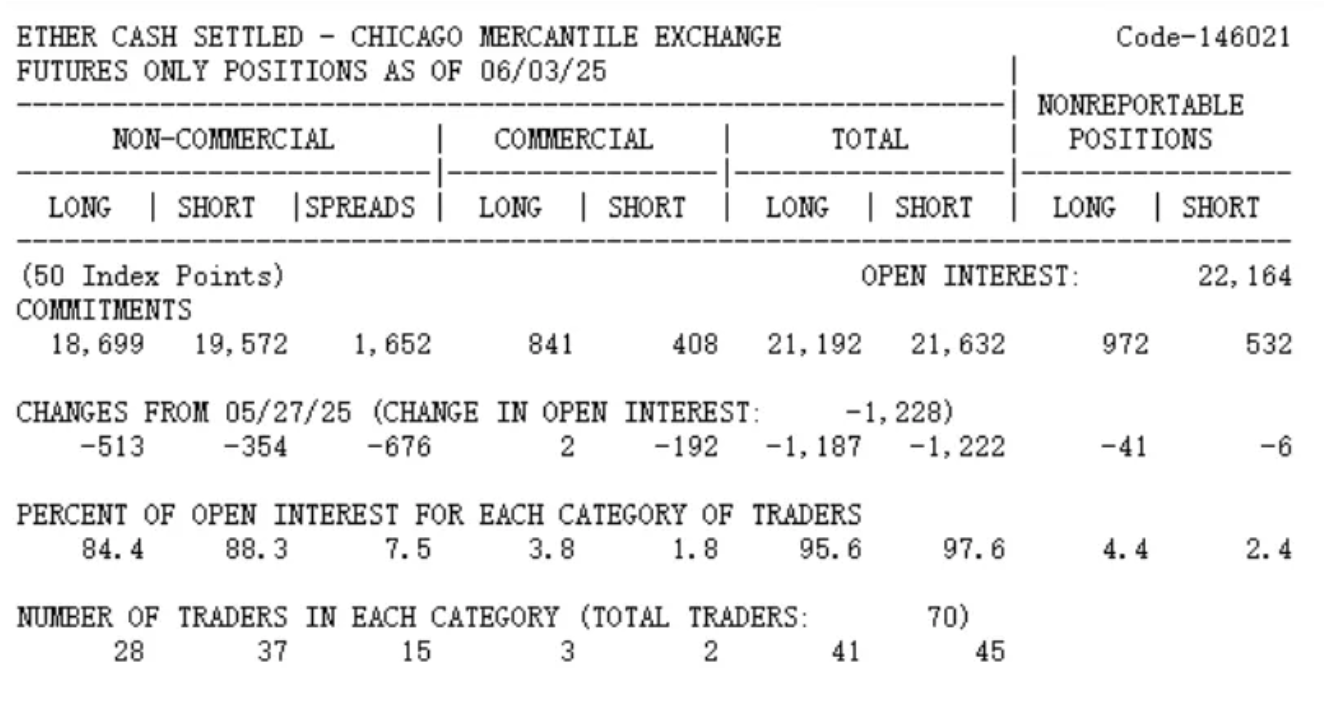

5. CME contract open interest hits new high

According to CME data, the current ETH trading volume on CME has not reached a new high, but the open interest (OI) has reached a near-record high. From the perspective of long and short positions, non-commercial traders have 18,699 long positions and 19,572 short positions, with a net position of 873 short contracts, indicating that speculators in the futures market are mostly bearish. If 30%-40% of the short positions of non-commercial traders are hedged, then the naked short positions account for 60%-70%. Calculated at a price of $2,750, the naked short positions of speculators on CME are approximately $1.6-1.8 billion.

6. AAVE lent ETH 6.8 billion

According to data from AAVE, the largest lending protocol on the chain, the current amount of ETH loaned on the chain is about US$6.8 billion. According to market common sense, these loans will not be fully hedged, and a lot of them will be leveraged short. We speculate that the amount of this naked short selling is no less than US$1 billion.

7. Spot ETFs continue to see net inflows, and the options market is bullish

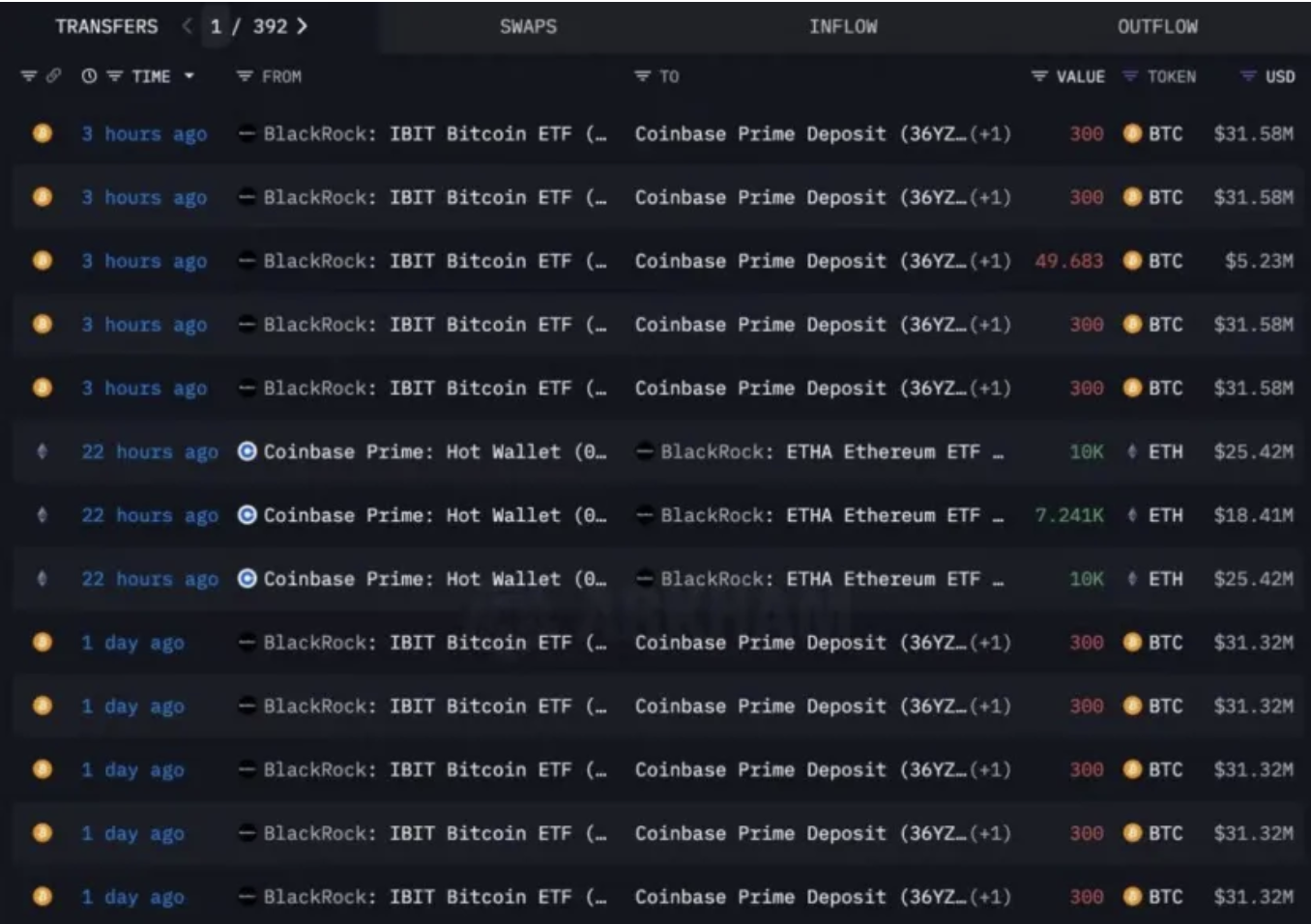

Through the data of futures derivatives, we believe that the current bearish sentiment in the market is still there, and there are naked shorts at the billion level, but a certain degree of bullish layout is reflected in the options and spot markets. In the spot market, ETH ETF reversed its previous weak state and continued to have net inflows for nearly 15 days. On June 10, the single-day net inflow reached US$125 million, and the cumulative inflow in June was US$450 million. Among them, BlackRock bought US$360 million, which was the main purchase, showing a bullish trend.

The changes in BlackRock ETH spot ETF holdings are as follows, which have been in a continuous increase since May 2025.

BlackRock is selling some BTC spot and buying ETH spot instead.

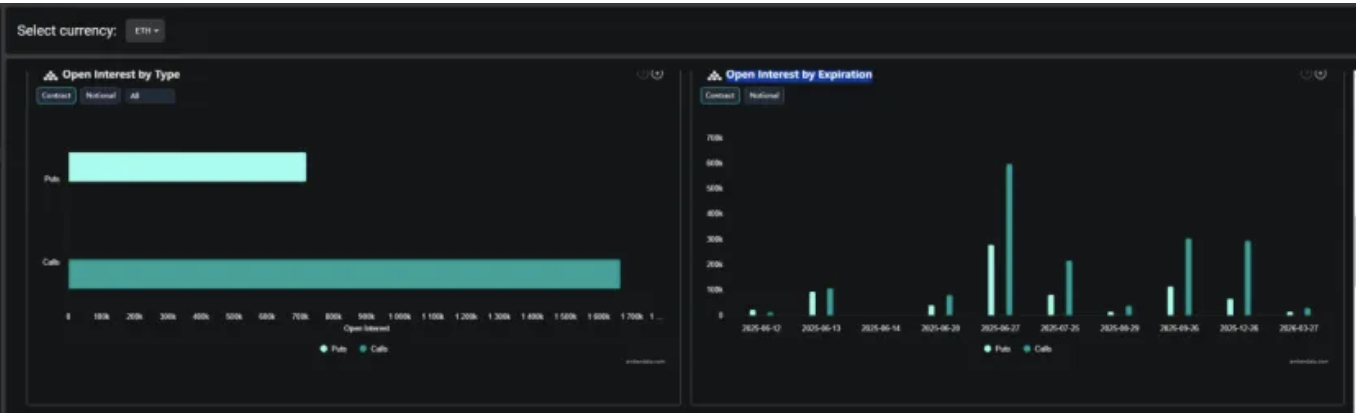

Deribit shows that the number of call options in the current open options is much higher than that of put options. There is not much difference between the two options for delivery before June 20, but in the options traded after June 20, the number of call options is significantly higher than that of put options.

Liquidation monitoring shows that $2.1 billion worth of ETH shorts will be liquidated at $3,000. The market will squeeze these shorts, and ETH is expected to rise to $3,000 in the short term.

8. Ethereum Treasury SBET brings new demands

In an environment that is crypto-friendly and leniently regulated, many companies in the U.S. stock market have imitated MSTR's model and purchased mainstream tokens such as BTC, ETH, and SOL as underlying assets.

Joe Lubin, co-founder of Ethereum and founder and CEO of ConsenSys, announced that he will serve as chairman of the board of directors of SharpLink Gaming (ticker: SBET) and lead its $425 million Ethereum Treasury strategy. The Ethereum Treasury will be an active treasury. In addition to enjoying the benefits of rising token prices, most ETH tokens will be used for staking, making it an active participant in network security, and investors can also receive at least 2% of staking income. This model will bring new demand for ETH.

9. Crypto companies are intensively listed, creating a continuous funding hotspot

Stablecoin Circle landed on Nasdaq in early June, and its stock price rose by more than 200% on the day of listing, triggering a high enthusiasm of market funds for cryptocurrency stocks. Many crypto companies have revealed their plans to list on Nasdaq. Bullish Global, a crypto asset trading platform in which Peter Thiel has invested, Kraken, a veteran trading platform, Galaxy Digital, a crypto asset management company, Bitgo, a cryptocurrency custody and institutional service provider, and Bgin Blockchain, a crypto mining equipment manufacturer, all have plans to go public, and some have already submitted applications for listing. The listing of these projects will create a continuous hotspot for funds, and more funds will pay attention to crypto assets and participate in them.

In summary, we believe that ETH contract holdings are at a high level and funds are active; market sentiment is heating up, but it has not yet entered the extreme greed stage; the number of bearish people on trading platforms is increasing, but there has not been a significant imbalance between long and short positions. ETH spot is in a continuous inflow stage, and options are bullish. The price has broken through the key support-resistance swap zone and further broke through the short-term resistance level. The long-term accumulated short orders may further boost the continuation of the rising market. Combined with the relaxation of digital currency regulation, the gradual increase in the market value of stablecoins, the gradual growth of Ethereum vault strategies in the U.S. stock market, and the increasing acceptance of crypto companies in the U.S. stock market, ETH may break through $14,000 in the medium and long term.

IV. Conclusion

The United States has further systematized, standardized, and clarified crypto regulation, simplified the issuance, custody, and trading procedures of crypto assets, promoted the issuance of stablecoins, and explored the development of innovative assets such as DeFi and RWA. This series of measures will expand the scale of crypto assets. Ethereum has the most mature on-chain financial ecosystem and is most likely to receive funds brought by the compliance of stablecoins. DeFi projects and RWA projects built on it will also benefit from this and achieve long-term development.

Click here to learn about BlockBeats' BlockBeats job openings

Welcome to join the BlockBeats official community:

Telegram subscription group: https://t.me/theblockbeats

Telegram group: https://t.me/BlockBeats_App

Official Twitter account: https://twitter.com/BlockBeatsAsia