Author: Tang Jun Kang Kai

summary

Unprecedented legislative endorsement in various countries and regions has given stablecoins a higher standard of development space than their predecessor Bitcoin. It will impact traditional cross-border payments. This is not only a business competition, but also related to the status of future sovereign currencies.

A virtual carnival in the marginal world finally extends to reality.

On June 5, Eastern Time, Circle Internet Group, Inc. (hereinafter referred to as "Circle"), the issuer of the world's second largest stablecoin USDC (Dollar Coin), was officially listed on the New York Stock Exchange. It opened up 122.58% on the first day. During the trading session, the stock price fluctuated too much and triggered a temporary circuit breaker.

By the close of the day, Circle's stock price had risen by 168.5%, with a total market value of over $18 billion. The next day, Circle's stock price continued to rise, and its current market value has exceeded $23.8 billion.

The enthusiasm of the capital market comes from the unprecedented endorsement of cryptocurrencies by sovereign states and regions, which has enabled stablecoins to gain a higher level of development space than their Bitcoin predecessors.

Two weeks ago, the U.S. Senate voted to pass the Guidance and Establishment of a United States Stablecoin National Innovation Act (hereinafter referred to as the "GENIUS Act"), and the Legislative Council of Hong Kong, China passed the Stablecoin Bill (hereinafter referred to as the "Bill") in the third reading, just two days apart.

Earlier, major economies such as the European Union, Singapore, and Japan have also included stablecoins in their regulation.

As a special cryptocurrency, stablecoins have the advantages of blockchain technology such as decentralization, peer-to-peer, low cost, and high efficiency. Unlike cryptocurrencies such as Bitcoin, stablecoins are usually pegged to reference assets such as legal tender to maintain a relatively stable value and serve as a medium for crypto asset transactions.

In 2014, Tether issued the first stablecoin USDT (Tether), marking the birth of stablecoins. In recent years, with the characteristics of stable value, high efficiency and low cost, stablecoins have gradually penetrated into traditional financial fields such as cross-border payments.

In sync with official legislative actions, global payment giants Visa and MasterCard announced that they would incorporate stablecoins into their global payment systems, which means that stablecoins are expected to become a mainstream payment and settlement option in global transactions.

Since the resumption of border access between Hong Kong and the Mainland in 2023, Chinese financial technology giants such as Ant, JD.com, and Tencent have gathered in Hong Kong to explore new opportunities in the Hong Kong Web3 (third-generation Internet) industry wave.

"It's very exciting." Ten days after the "Regulations" were passed, Ant Group Vice President and Ant Digits Blockchain Business President Bian Zhuoqun lamented in an interview with "Caixin" that stablecoin compliance is expected to open a window for the large-scale development of Web3 asset transactions.

"The Ordinance provides a good institutional environment for the healthy and sustainable development of Hong Kong's stablecoin market. It is also a major milestone event for the global cryptocurrency industry," said Liu Peng, CEO of JD CoinChain Technology.

Note: Hong Kong, China promotes stablecoins with the characteristics of flexibility, openness and user-friendliness. The city intends to emphasize the construction of an innovative digital financial system. Photo by Kang Kai

Stablecoins are issued and traded based on blockchain, and naturally have technical characteristics such as globalization, real-time transactions, 24/7 operation, and "peer-to-peer" decentralization. At the same time, stablecoins achieve value stability by being linked to legal currencies.

From official legislation to commercial layout, the high attention paid to stablecoins by all walks of life stems from its own substantial development in the past few years.

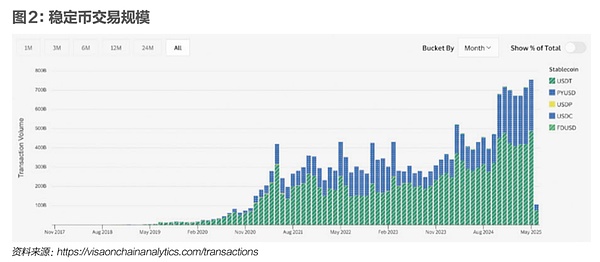

In 2024, the transaction volume supported by stablecoins will reach 27.6 trillion US dollars, exceeding the total transaction volume of Visa and Mastercard.

In the same year, Tether, the world's largest issuer of stablecoin USDT, had no more than 200 employees, but achieved a net profit of US$13.7 billion, with an average profit of more than US$68 million per person, making it the company with the highest per capita revenue in the world.

The financial reports of Tether and Circle show that their revenue mainly comes from the investment income of stablecoin reserve assets. After achieving compliance, how stablecoins can be applied in more scenarios has become the focus of market attention.

Circle asserted in its prospectus that its stablecoin network has the potential to disrupt the international remittance and cross-border payment markets. Bian Zhuoqun also believes that the biggest use case for stablecoins is cross-border payments, which can achieve a low-cost, T+0 (real-time) cross-border payment experience.

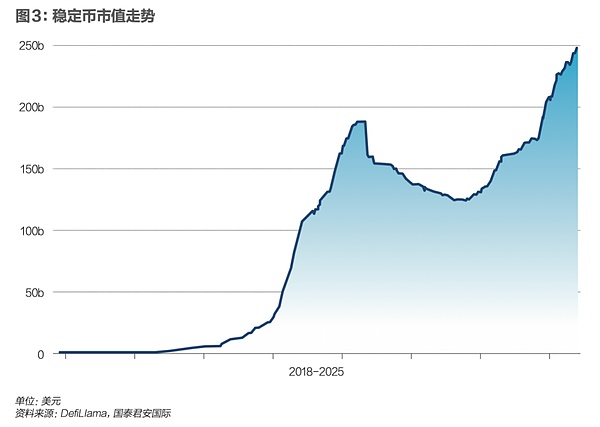

As the application of stablecoins in cross-border payments expands, sovereign currency competition also unfolds. Public data shows that as of May 2025, the global stablecoin stock size is about US$250 billion, of which 99% are US dollar stablecoins, far higher than the 49.68% share of the US dollar in global payment currencies.

Public data shows that as of May 2025, the global stablecoin stock will be approximately US$250 billion, of which 99% are US dollar stablecoins, which is far higher than the 49.68% share of the US dollar in global payment currencies.

"The US dollar stablecoin has been widely used in cross-border trade settlement, inter-enterprise payment, consumer payment, employee salary payment and corporate investment and financing activities." Zou Chuanwei, director of the Frontier Finance Research Center of the Shanghai Finance and Development Laboratory, told Caixin that the strengthening effect of the US dollar stablecoin on the status of the US dollar is emerging.

Zou Chuanwei, director of the Frontier Finance Research Center of the Shanghai Finance and Development Laboratory, told Caixin that the strengthening effect of the US dollar stablecoin on the status of the US dollar is emerging.

"The introduction of the stablecoin bill by the United States is equivalent to endorsing the dollar stablecoin. The dollar stablecoin will undoubtedly usher in greater growth in the future. " Xia Le, chief economist for Asia at Banco Bilbao Vizcaya Argentaria, told Caixin that this may further strengthen the status of the dollar.

"Xia Le, chief economist for Asia at Spanish bank BBVA, told Caixin that this could further strengthen the position of the U.S. dollar.

"The rapid development of the US dollar stablecoin has brought new challenges to the cross-border payment and clearing of the RMB. If we cannot surpass the US dollar stablecoin in terms of payment efficiency and clearing costs, then the cross-border payment and international development of the RMB will face great constraints." Wang Yongli, former vice president of the Bank of China, wrote.

In view of this, many professionals including Wang Yongli suggested that research on stablecoins should be strengthened, and consideration should be given to launching offshore RMB stablecoins in Hong Kong, China, and relevant exploration should be carried out.

In addition, Zhao Binghao, dean of the Financial Technology and Law Research Institute of China University of Political Science and Law, told Caixin that since 2017, China has adopted relatively strict regulatory measures on cryptocurrencies, and encrypted digital currency-related businesses have been classified as illegal financial activities.

"To a certain extent, this has put the stablecoins that exist in large numbers in domestic economic life and judicial practice in a regulatory vacuum, which is not conducive to China's participation in the construction of global crypto asset rules," said Zhao Binghao.

"Technology participants can roam around the world, but institutional shaping can only be done by sovereign states." Zhao Binghao bluntly said that China needs to move from "absence of supervision" to "institutional construction" and from "global follower" to "shaper of future rules." This is a challenge and an opportunity. The key lies in whether we are truly willing to face reality and dare to take responsibility.

Zhao Binghao said frankly that China needs to move from "absence of supervision" to "system construction" and from "global follower" to "shaper of future rules". This is a challenge and an opportunity. The key lies in whether we are willing to face reality and take responsibility.

"Now, the field of stablecoins and crypto assets has become a battleground for large businesses and even countries. China needs to adjust its policies on crypto assets and stablecoins. At least it should actively participate in the development of crypto assets and stablecoins overseas, accelerate the improvement of its own international competitiveness, and enhance the influence of international cooperation in this field." Wang Yongli said in the aforementioned article.

China needs to adjust its policies on crypto assets and stablecoins, at least actively participate in the development of crypto assets and stablecoins overseas, accelerate the improvement of its international competitiveness, and enhance the influence of international cooperation in this field. "Wang Yongli said in the aforementioned article.

With the endorsement of US legislation and the promulgation of the "Regulations" by Hong Kong, China, the EU, Singapore, Japan and other economies have included stablecoins under regulation; payment giants are positioning themselves for position... Stablecoins are impacting the traditional cross-border payment system. This is not only a commercial competition, but also concerns the status of sovereign currencies in the future.

Business competition: giants are making moves intensively

Commercial organizations have already started competing to make their moves in the stablecoin game.

On April 29, New York time, Mastercard’s official website issued a press release stating that in view of the increasingly clear global regulation of digital assets such as cryptocurrencies that are usually pegged to legal currencies, a new “stablecoin settlement” option will be added for merchants in the near future.

On April 30, San Francisco time, Visa's official website announced a partnership with fintech company Bridge to provide users with card products linked to stablecoins. Cardholders can directly use the stablecoin balance for daily consumption at any merchant that accepts Visa worldwide.

“We are focused on integrating stablecoins into Visa’s existing network and products in a frictionless and secure way,” said Jack Forestell, Visa’s chief product and strategy officer.

In addition, American online payment institutions such as Paypal and Stripe have already launched stablecoin payments.

In Hong Kong, China, financial technology giants such as Ant and JD.com are closely watching the implementation of stablecoin licenses.

In July 2024, JD CoinChain Technology, a subsidiary of JD Group, was selected into the Hong Kong Monetary Authority's stablecoin issuer sandbox along with two other companies.

Liu Peng revealed in an interview with "Caixin" that JD.com's stablecoin has entered the second phase of sandbox testing. The test scenarios mainly include cross-border payments, investment transactions, retail payments, etc. In the future, it will provide mobile and PC application products for retail and institutions.

"Issuing payment-type stablecoins through blockchain technology can not only solve the problems encountered in cross-border settlement, but also effectively serve other companies and the real economy, and can produce huge economic and social effects for companies and society." Liu Peng told "Caixin".

Liu Peng said, "It is foreseeable that the Hong Kong Monetary Authority is pushing forward the licensing issue in full swing. We are also cooperating with the regulator to complete the sandbox test. The specific licensing time is still waiting for the regulator's notification."

Ant Digits hopes that compliant stablecoins can open up a growth portal for its RWA (Real World Assets tokenization) business.

In August 2024, under the guidance of the Hong Kong Monetary Authority, Ant Digits supported Longsun Technology, a mainland new energy listed company, to successfully complete RWA cross-border financing, that is, to tokenize the income rights of new energy charging pile assets, making them on-chain assets, and selling them to global investors on the blockchain platform for financing.

"Hong Kong legislation gives stablecoins a legal identity, which is equivalent to issuing a 'birth permit' for Web3's on-chain transactions." Bian Zhuoqun said that compliant stablecoins will provide legal transaction currencies for on-chain transactions such as RWA, which means that the regulatory authorities have recognized the relevant business exploration. After obtaining legal status, stablecoins, RWA and other businesses are expected to usher in large-scale development.

Bian Zhuoqun said that compliant stablecoins will provide legal transaction currencies for on-chain transactions such as RWA, which means that the regulatory authorities have recognized the exploration of related businesses. After obtaining legal status, stablecoins, RWA and other businesses are expected to usher in large-scale development.

"I believe that the combination of our RWA and Hong Kong stablecoin will give rise to broad application scenarios and promote the development and growth of the Hong Kong dollar stablecoin," said Bian Zhuoqun.

Banking and financial institutions have also entered the market.

As early as 2019, JPMorgan Chase launched its own stablecoin - JP.M coin.

Recently, according to media reports, the largest banks in the United States are exploring whether to jointly issue a joint stablecoin. The companies involved in the discussion include JPMorgan Chase, Bank of America, Citigroup, Wells Fargo and other large commercial banks. At the same time, some regional banks and community banks in the United States are also considering whether to establish an independent stablecoin alliance. But for smaller banks, such a project will be more difficult.

Among the first three companies selected for the Hong Kong Monetary Authority's stablecoin issuer sandbox are Standard Chartered Bank (Hong Kong), Ansai Group, and a joint venture established by Hong Kong Telecom (HKT). It is reported that Standard Chartered Bank is one of the three note-issuing banks in Hong Kong, China, which will help the joint venture company to fully utilize the construction of banking infrastructure and rigorous governance.

In Japan, Mitsubishi UFJ, the country’s largest bank, is reportedly preparing to issue a yen stablecoin.

"Since 2025, the integration and development of stablecoins and the traditional financial system is being fully promoted." JD Group Chief Economist Shen Jianguang and others stated in a signed article published in "Caixin" that on the one hand, this is reflected in the continuous expansion of cooperation between stablecoin issuers and payment institutions, and on the other hand, banking institutions are also entering the stablecoin business.

JD Group Chief Economist Shen Jianguang and others stated in a signed article published in "Caijing" that on the one hand, this is reflected in the continuous expansion of cooperation between stablecoin issuers and payment institutions, and on the other hand, banking institutions are also entering the stablecoin business.

Legislative race: Countries are positioning themselves for digital finance

With Trump's re-election as US President, the cryptocurrency industry has been redefined. Behind this, a legislative competition for stablecoins is underway around the world.

On May 21, the Hong Kong Monetary Authority said that it welcomes the Hong Kong Legislative Council's passage of the "Regulations" to establish a licensing system for issuers of legal currency stablecoins in Hong Kong, China, and improve the regulatory framework for virtual asset activities in Hong Kong, China, in order to maintain financial stability and promote financial innovation. This means that Hong Kong, China will legally issue stablecoins.

After the implementation of the Ordinance, anyone who issues a fiat currency stablecoin in Hong Kong, China in the course of their business, or issues a fiat currency stablecoin claimed to be pegged to the value of the Hong Kong dollar in Hong Kong, China or outside, must apply for a license from the Monetary Authority.

"From the perspective of legislation, supervision, technology, and the global stablecoin legislation situation, the Regulation has arrived at a very good time to be launched." Bian Zhuoqun told Caixin, "The Regulation has been in planning for more than a year, and we can see that it has undergone sufficient preparation at the legislative level. Last year, the Hong Kong Monetary Authority launched a sandbox for stablecoin issuers to test relevant processes and rules, and it has also laid a certain foundation at the regulatory and technical levels. Internationally, the United States and other countries and regions have taken frequent actions, and stablecoin legislation is a general trend to a certain extent."

Hong Kong's move echoes that of the United States across the ocean. Just a few days later, the U.S. Senate voted to pass the GENIUS Act on May 19, which is the first federal-level stablecoin regulatory framework in the United States.

"The legislation in Hong Kong, China and the United States reflects the strategic positioning of both sides in digital finance. Both places are unwilling to be absent from the formulation of rules for digital financial infrastructure. Improving the regulatory system can gain an advantage in the global market." Li Ming, associate researcher of AIoT at the Hong Kong Polytechnic University, chairman of the IEEE Computer Society Blockchain and Distributed Ledger Standardization Committee, and executive president of the Hong Kong WEB3.0 Standardization Association, said in an interview with Caixin.

Xiao Feng, Chairman and CEO of Hong Kong HashKey Group, told Caixin that Hong Kong, China, followed the United States and started the "ChatGPT" moment of financial asset tokenization in 2025. This marks that the new generation of financial market infrastructure based on blockchain distributed ledgers has begun to gradually integrate with traditional finance.

This marks the beginning of the gradual integration of a new generation of financial market infrastructure based on blockchain distributed ledgers with traditional finance.

Stablecoins are a new emerging trend in the development of the financial industry, and the world is moving forward in exploration. All parties seem to have a consensus on the construction of the market's basic system, which is first reflected in the regulations on licenses and issuers.

According to the Hong Kong Regulations, three types of stablecoin activities require a license. First, issuing legal currency stablecoins in Hong Kong; second, issuing Hong Kong dollar stablecoins in or outside Hong Kong; third, actively promoting the issuance of legal currency stablecoins to the public in Hong Kong. The Regulations only allow designated licensed institutions to sell legal currency stablecoins in Hong Kong, and only legal currency stablecoins issued by licensed issuers can be sold to retail investors.

In the United States, only "licensed payment stablecoin issuers" can legally issue payment stablecoins. Licensed payment stablecoin issuers must be subsidiaries of insured deposit institutions, federally approved non-bank entities, or state-approved entities. In addition, compliant stablecoin issuers include not only entities registered in the United States, but also entities registered in foreign countries can register with the U.S. Office of the Comptroller of the Currency.

Stablecoins are seen as a bridge between cryptocurrencies and fiat currencies, and are pegged to stable reserve assets such as the U.S. dollar or gold. This means that regulators in Hong Kong and the United States have strict requirements on the adequacy of stablecoin reserve assets.

The Hong Kong Regulations require issuers to have a minimum paid-in capital of HK$25 million and to hold highly liquid reserve assets equal to the par value of the circulating stablecoin. In the United States, stablecoins must be backed by highly liquid assets at a ratio of at least 1:1, including US dollar cash, notice deposits, US Treasury bonds due within 93 days, repurchase agreements, etc. Reserve assets must not be repeatedly pledged or misappropriated, and issuers must publicly disclose redemption policies.

However, beyond the consensus, different countries and regions still have different development strategies for stablecoins, which may lead to differences in the development of national markets. In Li Ming's view, the implementation of stablecoins in Hong Kong, China is characterized by flexibility, openness and user-friendliness. The region aims to emphasize the construction of an innovative digital financial system.

First, the US Act stipulates that stablecoins can only be pegged to the US dollar, while the Hong Kong Act allows for pegs to fiat currencies such as the Hong Kong dollar, US dollar or RMB. Second, regarding reserve assets, the US Act clearly stipulates that US dollar cash or short-term US Treasury bonds can be used as reserves. The Hong Kong Act allows for a variety of low-risk assets such as cash, short-term Treasury bonds, and commercial paper, but does not specify specific reserve asset categories.

"Hong Kong, China is promoting stablecoins, which are pegged to more assets. To a certain extent, this can consolidate Hong Kong's position as an international financial center and accelerate Hong Kong's development towards digital finance," said Li Ming.

In the view of Hong Kong Legislative Council member Wu Jiezhuang, the legal issuance of stablecoins will be an important step for Hong Kong, China to become an international Web3 center. "In the future, we will focus on promoting two directions: one is to expand the application scenarios of stablecoins in physical retail, cross-border trade and other fields; the other is to improve the market attributes of stablecoins, including releasing stablecoin interest to holders to enhance market competitiveness."

"In comparison, the United States emphasizes maintaining the dominance of the US dollar. Stablecoins may become a strategic tool for the United States to maintain the status of the US dollar, which will alleviate the pressure on the US dollar and US debt to a certain extent." Li Ming further said.

Previously, U.S. Treasury Secretary Besant said that stablecoins will strengthen the dollar's position as the world's dominant reserve currency.

However, in the view of some market participants, although the GENIUS Act has been passed by the Senate, there may still be obstacles in the process of implementation in the future. For example, although the bill strengthens anti-money laundering and national security clauses, it does not resolve the conflict of interest controversy brought about by Trump, which may cause disputes between the Republicans and the Democrats again. Generally speaking, it takes a long political struggle for the U.S. Congress to introduce a new law. During the deliberation of the Senate and the House of Representatives, the process requires multiple rounds of consultation and compromise.

In the global game of stablecoins, countries and regions such as the European Union, Japan, and Singapore are also involved, which reflects that all countries are unwilling to lose at the starting line.

In 2024, the EU's Markets in Crypto-Assets Act (MiCA) officially came into effect. This solves the fragmentation and regulatory arbitrage problems in the EU and EEA countries in crypto-asset regulation and is the world's largest cryptocurrency regulatory law. The Monetary Authority of Singapore issued stablecoin regulations in August 2023. Under this framework, stablecoins can be used as a medium of exchange to connect the legal currency and digital asset ecosystems.

"Stablecoins need to provide financial collateral, and they are becoming an important bridge connecting the current financial world and the digital world. Behind this, the trends of major global economies such as the United States and the European Union are most worthy of attention. As cross-border payments, supply chain finance, remittances and other applications gradually take shape, stablecoins of various countries will play a greater role in the financial field, and this will even rise to an issue of international political economy." Li Ming said.

In fact, the global legislative race is laying the institutional foundation for the market and promoting the continuous development of the stablecoin industry. "Stablecoins are the tokenization of legal tender. Perhaps ten years later, all financial assets may be tokenized, because the transaction settlement system based on the blockchain distributed ledger is more efficient, lower cost, and has fewer links than the traditional transaction settlement system. This allows payment settlement based on stablecoins to do more with less funds, and because the time for funds to be in transit is reduced, the efficiency of fund use is also improved, allowing funds to obtain more interest income. This is exactly what the financial director of any institution dreams of." Xiao Feng said.

Capital story: Related concept stocks soared

The first stablecoin license has not yet been issued, but digital currency concept stocks have taken over and are rising.

Wind data showed that as of June 6, the A-share digital currency index was at 2135.19 points, up 17% from two weeks ago. On May 29, digital currency concept stocks such as Lakala, Xiongdi Technology, and Sifang Jingchuang all hit their daily limit.

Cryptocurrency concept stocks are also hot in the Hong Kong stock market. As of June 6, ZhongAn Online (06060.HK) and LianLian Digital (02598.HK) rose 41% and 20% respectively compared to two weeks ago. As of the close of the day, ZhongAn Online and LianLian Digital were priced at HK$17.50 and HK$8.96 per share respectively.

The market's enthusiasm for digital currency is not limited to the policy level. They are more looking forward to the possibility of its commercial implementation, which has become the key to the outbreak of digital currency concept stocks in recent times.

As a subsidiary of ZhongAn Online, ZhongAn Bank will become the first digital bank in Hong Kong, China to provide reserve bank services to stablecoin issuers in 2024. Currently, ZhongAn Bank has provided commercial banking services to more than 80 Web3 companies and is also the banking partner of local licensed virtual asset trading platforms HashKey and OSL.

By the end of 2024, DFX Labs, a subsidiary of LianLian Digital, had obtained the Hong Kong Virtual Asset Trading Platform (VATP) license, making it one of the ten licensed VATPs in Hong Kong. In addition, the company also has a partnership with Yuanbi Technology, which was selected for the Hong Kong Stablecoin Issuer Sandbox.

"The share prices of listed companies involving digital currency and blockchain concepts in A-shares and H-shares have risen sharply, reflecting the market's collective consensus on the revaluation of structural assets. The institutional progress of policies has sent a clear signal that stablecoins, as the technical form closest to the real financial system in the digital asset market, are gaining regulatory recognition and are beginning to be embedded in the sovereign financial architecture." Yu Jianing, co-chairman of the Blockchain Committee of the China Communications Industry Association and honorary chairman of the Hong Kong Blockchain Association, told Caixin.

The institutional progress of the policy sends a clear signal that stablecoins, as the technical form closest to the real financial system in the digital asset market, are gaining regulatory recognition and beginning to be embedded in the sovereign financial architecture. Yu Jianing, co-chairman of the Blockchain Committee of the China Communications Industry Association and honorary chairman of the Hong Kong Blockchain Association, told Caixin.

From the perspective of changes in the financial architecture, some market participants believe that the application scenarios of stablecoins can be roughly divided into two parts. The first is for businesses (to B), which is mainly used for cross-border settlement and supply chain finance; the second is for consumers (to C), which is mainly used for consumption, transfers, remittances, etc.

"The C-end scenario has a relatively mature user base, but it still needs to leverage the advantages of traditional industries for large-scale promotion in the market. At the same time, the B-end scenario needs to rely on the upgrade of traditional financial services to allow more traditional institutions to accept innovative business models. Both scenarios require upgrading and transformation of existing financial infrastructure, which will be a huge market opportunity. For enterprises, from the perspective of time and cost, using stablecoin payment and settlement can improve service efficiency and reduce usage costs." Li Ming said.

He further stated that with the advancement of technology and the implementation of business scenarios, stablecoin system providers, operators and financial service institutions can all benefit. This can not only provide payment, settlement and custody services for enterprises and consumers, but also give rise to new infrastructure, services and investment opportunities. In addition, stablecoins will also promote the gradual maturity of the RWA industry and form a new Web3.0 ecosystem.

Not only in the secondary market, the trend of stablecoins has also boosted the enthusiasm of the primary market.

In April, Circle, the issuer of the world's second largest stablecoin USDC, formally submitted an IPO (initial public offering) application to the U.S. Securities and Exchange Commission.

According to the company's updated prospectus on June 2, its IPO issuance scale has been expanded from 24 million shares to 32 million shares, and the pricing range has been increased from US$24-26 per share to US$27-28 per share. The issuance results show that Circle ultimately raised approximately US$1.1 billion at a price of US$31 per share, exceeding the previous pricing cap.

From a fundamental perspective, Circle's profit model is mainly "interest-earning". That is, each USDC issued is backed by a $1 legal currency reserve. Circle stores these reserves in safe short-term assets, such as US bank deposits and short-term US Treasury bond funds managed by BlackRock. In this way, it can generate considerable interest income in a high-interest environment.

That is, every USDC issued is backed by a $1 fiat currency reserve. Circle stores these reserves in safe short-term assets, such as US bank deposits and short-term US Treasury bond funds managed by BlackRock. In this way, it can generate considerable interest income in a high-interest environment.

According to the prospectus, Circle's total revenue in 2024 will be approximately US$1.676 billion, of which 99% (approximately US$1.661 billion) will come from interest income generated by USDC reserves. In the same year, its net profit reached US$156 million.

In the view of market participants, compared with Tether, Circle’s biggest advantage is compliance and transparency. With the implementation of the US GENIUS Act, the volume of compliant stablecoins will increase in the future, and Circle’s advantage may be expanded.

Although digital assets are popular in the market, they, including stablecoins, are facing multiple challenges in regulation, technology, and business, which also causes concerns in the market.

"At present, the complexity of regulatory risks is particularly prominent, and there are obvious differences in the pace of legislative processes among countries. In addition, stablecoins have macro-spillover problems, which may pose a potential impact on national monetary sovereignty and capital controls. In the future, stablecoins must strike a balance between efficiency and compliance," said Yu Jianing.

Compared with stablecoins, central bank digital currencies (CBDCs) are also a means for countries to regulate and promote digital currencies. Massimiliano Castelli, head of global sovereign market strategy and consulting at UBS Asset Management, told Caixin that at present, the form of central bank digital currencies may have obvious advantages. It is issued by central banks of various countries, which can control the amount of currency issuance and prevent inflation caused by excessive currency issuance. In addition, central banks of various countries can monitor capital flows, provide legal protection, and prevent risks in advance.

Payment innovation: cross-border transactions become the largest scenario

Many interviewees told Caixin that as of now, the main application scenario of stablecoins is crypto asset trading, namely "cryptocurrency speculation."

In fact, the birth of stablecoins in 2014 was to solve the problem of deposits and withdrawals in cryptocurrency trading. On the one hand, crypto asset transactions mostly occur in non-compliant offshore exchanges and decentralized exchanges, which are often unable to access the mainstream banking system and lack channels for investors to enter and exit funds; on the other hand, the prices of cryptocurrencies such as Bitcoin fluctuate frequently and cannot serve as trading currencies.

In this context, stablecoins with stable value and the ability to connect to the traditional financial system came into being. Taking Bitcoin investment as an example, investors need to first purchase stablecoins and then use them to buy and sell Bitcoin on exchanges. For this reason, stablecoins are considered a bridge between legal tender and the Web3 digital ecosystem.

Driven by the enthusiasm of cryptocurrency investors, the efficiency and cost advantages of stablecoins in cross-border payments have been fully demonstrated.

According to Zou Chuanwei, in traditional cross-border transaction scenarios, transaction funds flow overseas through the bank account system, while transaction information is transmitted through message systems such as SWIFT (Society for Worldwide Interbank Financial Telecommunication). Payment settlement can only be completed after the two meet. At the same time, cross-border payments often involve cross-time zones, cross-systems, cross-networks, and cross-bank settlements. Each link must undergo KYC (know your customer), anti-money laundering, anti-terrorist financing and other compliance reviews, which are generally costly and inefficient.

Stablecoins have the characteristics of "peer-to-peer" transactions, and cross-border payments usually only require one wallet address. "The capital flow and information flow of stablecoins are combined into one, and they are all running on a blockchain system, running 24 hours a day, without any intermediate links, and of course faster," said Zou Chuanwei.

Shen Jianguang mentioned in a previous article that according to data from the World Bank, existing cross-border bank remittances usually take about five working days to settle, with an average cost rate of 6.35%. However, blockchain-based stablecoin payments support global "7×24" real-time payments, and the fees are very low. For example, the average cost of sending stablecoins through blockchains such as Solana is about $0.00025, and Binance Pay's stablecoin transfers only charge $1 when the transfer amount exceeds 140,000 USDT.

It is worth noting that Zhao Yao, a guest researcher at the Payment and Clearing Research Center of the Institute of Finance of the Chinese Academy of Social Sciences, stated in his signed article that the fixed cost of a typical B2B cross-border payment is between US$25 and US$35, of which account liquidity costs, financial operation costs and compliance costs account for the majority. "In the future, after stablecoins enter the regulatory compliance framework, the various costs that traditional cross-border payments should pay will also be imposed on stablecoins. Only practice can verify the cost advantage of stablecoin cross-border payments." Zhao Yao said.

The ability and stability of stablecoin payments are also constantly improving. Shen Jianguang said that the actual TPS (number of transactions per second) continuously processed by mainnet such as Solana has reached 2,000-3,000 times, and is rapidly approaching mainstream payment institutions such as Visa and MasterCard.

Shen Jianguang said that the actual TPS (number of transactions per second) continuously processed by mainnet such as Solana has reached 2,000 to 3,000 times, and is rapidly approaching mainstream payment institutions such as Visa and Mastercard.

In the stablecoin sandbox test conducted by JD.com, cross-border payments also showed the characteristics of fast transaction speed, low cost, and uninterrupted service throughout the year. "This makes it very suitable for current international trade settlement applications." Liu Peng said.

With its characteristics of 24-hour operation, natural cross-border nature, instant settlement and low cost, the application prospects of stablecoins in the field of cross-border payments have become a consensus.

Circle asserted in its prospectus that its stablecoin network has the potential to disrupt the international remittance and cross-border payment markets. According to McKinsey's 2024 Global Payments Report, international remittance and cross-border payment revenues will be approximately $288 billion in 2023.

Bian Zhuoqun also told Caixin that "the biggest use case for stablecoins is cross-border payments, which can achieve low-cost, T+0 (real-time) cross-border payment experience."

This also leads to a question: to what extent will stablecoins replace the existing cross-border payment and settlement system?

"The stablecoin payment network is a non-bank payment system based on blockchain, which certainly has its development space and prospects. But it is different from existing payment systems, such as the global payment network based on bank accounts and messaging systems such as SWIFT, and the two are not comparable," said Zou Chuanwei.

"According to the provisions of the mainstream stablecoin bill, stablecoins are more defined as a payment tool, which is essentially similar to the WeChat Pay and Alipay balances we are familiar with. It is hard to imagine that ordinary people do not use bank cards (especially credit cards), but instead recharge their money into Alipay and WeChat." Zou Chuanwei believes that the natural characteristics of stablecoins determine that it is more of a system focused on retail payments, and is more used in retail payment scenarios in cross-border payments, including cryptocurrency trading.

Zou Chuanwei believes that the natural characteristics of stablecoins determine that it is a system that focuses more on retail payments, and is more used in retail payment scenarios in cross-border payments, including cryptocurrency speculation.

In international trade settlement, the "peer-to-peer" transaction model of stablecoins is not necessarily a better choice.

Zhao Yao said that the "point-to-point" disintermediation ignores the dual information asymmetry of time and space in international trade settlement, ignores the experience and system accumulated by mankind in international trade activities over a long period of time, and also ignores the inherent need of international trade for various types of intermediary service agencies such as insurance, notarization, and inspection. It is precisely because of the complexity of international trade settlement that people have developed various trade settlement tools such as letters of credit (L/C), collections (Collection), and telegraphic transfers (T/T), while telegraphic transfers that are close to "point-to-point" payments can be applied to very few trade scenarios.

An article published by Zhao Binghao in the Political and Legal Forum in 2022 pointed out that "the convenience and global nature of stablecoins also bring many regulatory challenges such as cross-border money laundering and evasion of foreign exchange supervision."

"Electronic fraud, drugs, money laundering, etc., all illegal and criminal activities involving fund transactions use stablecoins to evade supervision." Zhao Binghao told Caixin, "Take electronic fraud as an example. After the fraudster succeeds, he quickly converts the fraud funds into stablecoins and transfers them. Stablecoins have strong anonymity and fast fund transfer speed, which brings great challenges to judicial organs from a technical point of view."

Relevant officials of the Ministry of Public Security once introduced at the "Commentary on the Work of Combating Telecom Network Fraud Crimes" that fraud groups use new technologies and new formats such as blockchain and virtual currency to continuously update and upgrade their criminal tools, and the offensive and defensive confrontation with public security organs in communication networks and money laundering through transfers has continued to intensify and escalate. From the perspective of funding channels, the proportion of money laundering through traditional third-party payments and public accounts has decreased, and a large number of money laundering platforms and digital currencies have been used, especially the use of USDT, which is the most serious.

"Stablecoins and traditional payment and settlement systems will continue to exist in parallel for a considerable period of time in the future," Zou Chuanwei concluded.

“Payment is only one link in the operation of market entities, and the ultimate goal is to obtain returns denominated in legal currency and reflected in legal currency.” Liu Xiaochun, deputy director of the Shanghai New Finance Research Institute, said in his signed article, “Stablecoins must eventually be cashed in as legal currency and credited to bank accounts to obtain interest income.”

In Liu Xiaochun's view, the exchange of different currencies in cross-border payments cannot be solved by stablecoins, and ultimately it must be achieved through the bank clearing system. It can be seen that the real success of stablecoins is not to break away from the banking system, but to connect with the banking system efficiently and seamlessly.

Currency wrestling: Is dollarization making a comeback?

Behind the legislation and commercial competition surrounding stablecoins lies the struggle for sovereign currencies.

A key background for the Trump administration to push for the GENIUS Act is that the status of the US dollar is declining.

Data from the IMF (International Monetary Fund) shows that as of the end of 2024, the U.S. dollar's share of global official foreign exchange reserves fell to 57.80%, the lowest since statistics began in 1995.

In April and May 2025, U.S. Treasury bonds fluctuated violently for two consecutive months, and the market's trust in U.S. Treasury bonds as the "safest assets" began to weaken.

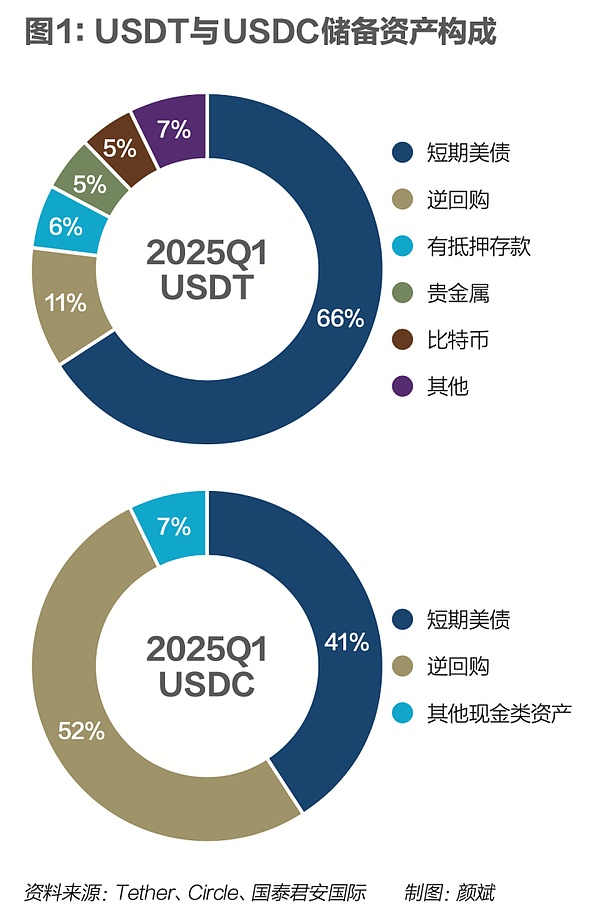

At the same time, USD-denominated stablecoins account for more than 99% of the total market value of stablecoins, and their reserve assets are mainly US Treasuries. As of the end of 2024, Tether directly or indirectly holds US$113 billion in US Treasuries, making it one of the largest holders of US Treasuries.

Deutsche Bank believes that since the Stablecoin Act formally establishes the role of stablecoin issuers as quasi-money market funds, this not only supports the U.S. short-term debt market, but also guides non-U.S. dollar liquidity to the U.S. dollar.

According to the Federal Reserve, the amount of U.S. dollar cash in circulation (M0) is $5.8 trillion by the end of April 2025. The Federal Reserve previously estimated that about 60% of the U.S. dollar is circulated outside the United States. Based on this calculation, the amount of U.S. dollar cash currently circulating outside the United States is $3.48 trillion.

"Stablecoins and cash are substitutes. If US dollar stablecoins replace US dollar cash circulating outside the United States, the scale will also be trillions of dollars." Xia Le said that this means that US dollar stablecoins may bring trillions of dollars in purchasing power for US debt.

Standard Chartered Bank's report predicts that stablecoin issuance will reach US$2 trillion by the end of 2028, bringing an additional US$1.6 trillion in demand for purchasing U.S. short-term Treasury bonds.

In the view of some industry insiders, the Trump administration is trying to build a "Bretton Woods system on chain" through the GENIUS Act, but the anchor of the US dollar has changed from gold to US debt.

Some people hold different opinions on this.

In Zou Chuanwei's view, the so-called "Bretton Woods system on the chain" exaggerates the role of stablecoins. "The total amount of U.S. national debt exceeds 36 trillion U.S. dollars, while the total amount of stablecoins is only 250 billion U.S. dollars, and it mainly reserves short-term U.S. debt. It is not enough to solve the problem of U.S. national debt, especially the problem of long-term U.S. debt."

"To put it another way, assuming that the U.S. debt held by the issuer of stablecoins can be expanded to 10 times the current level, is this a good thing for the United States, or a potential risk point for financial stability? It remains to be seen." Zou Chuanwei said that in theory, users of stablecoins can redeem them at face value at any time, and the issuer will sell reserve assets accordingly. Once users redeem them in a concentrated manner, the issuer of stablecoins will sell U.S. debt in a concentrated manner, which may cause market turmoil.

"In theory, the US dollar stablecoin faces an ' Blockchain Trilemma': large-scale issuance of US dollar stablecoins, large-scale investment of reserve assets in US Treasuries (especially long-term Treasuries), and users can redeem flexibly. These three goals cannot be achieved at the same time." Zou Chuanwei said.

Despite this, it is almost a consensus in the industry that US dollar stablecoins will strengthen the status of the US dollar.

"This is mainly because the US dollar stablecoin will strengthen the use of the US dollar worldwide." Xia Le said that in some countries where the sovereign currency is not strong enough, the US dollar stablecoin may largely replace the local sovereign currency, enter daily payments, and impact a country's monetary system, which is the so-called "dollarization" problem.

Previously, sovereign states mainly ensured the status of sovereign currencies through legislation and law enforcement, but stablecoins, as online payment tools, have also brought considerable challenges to local government supervision.

In fact, Zou Chuanwei told Caixin that there are also residents and institutions in mainland China that hold and use US dollar stablecoins. The application scenarios include daily payments, trade settlements, investment and financing, and even capital flight, forming a "US dollar enclave."

Taking the cross-border e-commerce scenario as an example, a domestic cryptocurrency investor and researcher told Caixin that he found in field research in Yiwu and other places that some cross-border e-commerce companies collect US dollar stablecoins during the sales process to reduce collection costs, improve collection efficiency, and circumvent foreign exchange controls. In domestic transactions, US dollar stablecoins are also used.

Another person from a cross-border payment institution told Caixin that there are indeed very few cross-border e-commerce companies and some traditional cross-border traders who use US dollar stablecoins for transactions. This phenomenon may be concentrated in countries and regions such as Africa and South America where the foreign exchange environment is complex and traditional banks have weak cross-border processing capabilities (local banks are unable to handle foreign exchange or the processing time is too long).

In this regard, many interviewees stated that the RMB is a strong currency, and the secret circulation of US dollar stablecoins within the country will not shake the RMB's sovereign currency status, but attention should be paid to its impact on the internationalization of the RMB.

Wang Yongli wrote that “the rapid development of the US dollar stablecoin has brought new challenges to the cross-border payment and settlement of RMB. If the payment efficiency and settlement cost cannot be surpassed by the US dollar stablecoin, then the cross-border payment and international development of RMB will face great constraints.”

In view of this, professionals including Wang Yongli have suggested that research on stablecoins should be strengthened, and consideration should be given to launching offshore RMB stablecoins in Hong Kong, China, and relevant exploration should be carried out.

"At present, the RMB is actually used for daily payments in some countries. Offshore RMB stablecoins can replace this part of the demand, which is a good choice for promoting the internationalization of the RMB." Xia Le said that in the face of the spillover effects that may be brought about by the US dollar stablecoin in the future, China must try to issue RMB stablecoins before it knows how to respond.

Under current rules, there are also some obvious challenges in issuing offshore RMB stablecoins.

"The biggest challenge is the lack of a sufficiently deep offshore RMB currency market, " Xia Le said. "Currently, offshore RMB currency products are limited, and short-term interest rates fluctuate widely. Can they provide sufficient liquidity and stability for offshore RMB stablecoins?"

"Xia Le said, "Currently, offshore RMB currency products are limited, and short-term interest rates fluctuate greatly. Can they provide sufficient liquidity and stability for offshore RMB stablecoins?"

In addition, stablecoins themselves may also face risks such as price decoupling.

In May 2022, UST, the world's third largest dollar stablecoin, decoupled due to the plummeting price of its anchored assets, and eventually suffered a systemic collapse, with its market value, which once exceeded US$18 billion, falling to zero.

The risks of the traditional financial system are also penetrating into stablecoins. In March 2023, Silicon Valley Bank collapsed after a deposit run, and Circle failed to successfully withdraw part of its cash reserves deposited in the bank. As a result, USDC was panic-sold by investors. The price of USDC once decoupled and fell to around $0.87.

In March 2023, Silicon Valley Bank collapsed after a run on its deposits, and Circle failed to successfully withdraw part of its cash reserves stored in the bank. As a result, USDC was panic-sold by investors. The price of USDC once decoupled and fell to around $0.87.

"Stablecoins may face various risks during their operation, including liquidity risk, market risk, technical risk, compliance risk, etc." A technology expert who has been deeply involved in the Hong Kong market told Caixin that in this regard, the Regulations have made detailed provisions on the issuance and management of stablecoins from a legislative level, including liquidity management, reserve asset management, technical risk management, as well as KYC, anti-money laundering, anti-terrorist financing and other compliance management.

"In the actual supervision process, relevant measures are expected to be more detailed and implemented to strictly control risks," said the aforementioned person.