TL;DR

Stablecoins have long been considered the "crown of the crypto industry", but early development was mainly focused on algorithmic stablecoins like Ampleforth's AMPL and Terra's UST (LUNA). These projects attempted to break free from USD asset dependence, building "dollar stablecoins" through algorithmic mechanisms, aiming to promote large-scale application of stablecoins in crypto and DeFi ecosystems, ultimately expanding to traditional off-chain users. Additionally, they differed significantly in their approach. Ampleforth was dedicated to creating a native settlement unit entirely within the crypto world, thus not maintaining a 1:1 peg with the US dollar; while TerraUSD (UST) tried to maintain a stable anchor to the US dollar to be more widely used as a payment and value storage tool.

This year, with the emergence of Ethena, DeFi stablecoins are no longer just price-anchored but have begun to anchor "yield sources". A new class of "strategic stablecoins" is emerging, essentially packaging hedging strategies or low-risk yield products into $1 face value circulating tokens. For example, Ethena's USDe is similar to a fund share, generating yield through a delta-neutral strategy of longing stETH and shorting perpetual contracts, distributed to holders in the form of sUSDe. Due to its similarity to hedge fund subscription shares, this stablecoin structure is viewed as a security by regulators like Germany's BaFin.

When systematically reviewing the yield mechanisms behind stablecoins, the article categorizes them into nine types, including on-chain lending, real-world assets (RWA), AMM market-making, CeFi deposits, protocol savings rates (like DSR), fixed-rate notes, derivative hedging, staking yields, and strategy aggregation Vaults. The annualized yield for each channel is currently roughly concentrated in the 3-8% range, with some special periods potentially briefly exceeding double digits.

Although current strategic stablecoin projects may seem highly homogeneous, their core differences are actually reflected in three key dimensions: sustainability of yield structure, transparency of yield disclosure, and compliance basis. Currently, stablecoins based on real-world assets (RWA), such as USDY and OUSG, have a relative advantage in compliance and have gained some regulatory acceptance, but their growth is limited by the US Treasury market structure. In comparison, derivative-linked stablecoins like USDe offer higher flexibility and yield potential but are more dependent on open interest in perpetual contract markets and more sensitive to market fluctuations.

In this trend, the most benefited infrastructure project is Pendle. By decomposing yield assets into fixed principal (PT) and floating yield (YT), the protocol builds an on-chain interest rate market, promoting standardization of "interest rate hedging" and "yield transfer". As more stablecoin projects use Pendle to manage their cash flows, its TVL, trading volume, and bribe mechanism are expected to grow further.

We believe that future strategic stablecoins will evolve towards modularity, regulatory-friendliness, and clear yield, and projects with unique yield sources, good exit mechanisms, and liquidity moats (ecosystem adoption) will become the cornerstone of the next "on-chain money market fund". However, these products may still be classified as securities by regulators, and potential compliance challenges cannot be ignored.

[The rest of the translation follows the same professional and accurate approach]Stablecoin's Own "Savings Rate"

DSR (Dai Savings Rate) was initially launched by MakerDAO and has now evolved into the SSR (Stablecoin Savings Rate) module in Sky.money. This module allows USDS holders to receive a share of protocol profits at an annualized interest rate, with interest calculated in real-time per block, no lock-up period, no fees, and users can deposit and withdraw at any time.

The earnings come from profits generated by MakerDAO/Sky.money. To promote broader use of USDS in DeFi, Sky.money has established an incentive mechanism that allocates part of the protocol income to the USDS savings rate. Currently, this rate is approximately 4.5% annually.

USDS Growth, source: defillama

Essentially, this is a protocol dividend-type stablecoin model. During market downturns, Sky.money may redirect earnings originally meant for empowering native tokens to USDS to promote its use, which could weaken the price support of native tokens. In a favorable market, moderately yielding token earnings in exchange for overall protocol growth can help improve token price, which is a reasonable strategy. Since this model is deeply tied to the protocol, Sky.money needs sufficient influence to truly promote USDS as a widely used unit of account, which is extremely challenging and demonstrates great ambition.

[The rest of the translation follows the same professional and precise approach, maintaining the technical terminology and context.]1. First, a new approach to assets. BTC, as a key asset connecting TradFi and Web3, has a market capitalization of trillions of dollars. If basic interest rates can be introduced into stablecoins through BTC-Fi, building a stablecoin system based on the BTC ecosystem might have lower promotion difficulties. However, the challenge lies in the lack of infrastructure in the BTC ecosystem itself. Considering an off-chain entry, such as starting with contract rate arbitrage around BTC, the overall logic still falls within the category of strategic hedge funds.

2. Secondly, new applications of strategies. In theory, all arbitrage strategies can become sources of "stablecoin" interest. For example, on-chain MEV, IV-RV deviation, cross-period volatility arbitrage, GameFi yields, and even security guarantee fees provided by EigenLayer AVS or partial income from DePIN devices could potentially be incorporated into the stablecoin interest mechanism, thereby deriving a new stablecoin interest rate model.

However, fundamentally, these are still strategy-based synthetic stablecoins, not stablecoins anchored to real assets in the traditional sense. Their market capacity is limited by the feasible space of the strategy itself, that is, the scale of the underlying market. Currently, most related markets are still small. In the long term, with the overall expansion of DeFi, this track has growth potential, especially since many strategies are highly Crypto Native, able to more sensitively reflect changes in the on-chain market.

Beneficiary of the Stablecoin War: Pendle

Fixed interest rate is an innovative yield mechanism aimed at providing users with predictable fixed returns, similar to zero-coupon bonds in traditional finance. In traditional finance, zero-coupon bonds are issued at a price below face value, redeemed at face value upon maturity, with no interest paid during the period. Investors' returns come from the difference between the purchase price and the redemption amount. In DeFi, Pendle has introduced a similar mechanism by tokenizing the future yields of yield-generating assets, allowing users to:

1. Lock in fixed returns: By purchasing tokens representing principal, holding until maturity provides a fixed return.

2. Speculate on yields: By purchasing tokens representing future yields, betting on changes in yield rates.

3. Improve capital efficiency: Selling future yields for immediate liquidity while retaining principal ownership.

Pendle Snapshot, source:pendle

Pendle is a DeFi protocol focused on yield tokenization, allowing users to split yield-generating assets into two types of tokens, PT and YT, and trade them on its platform. Essentially, Pendle builds a trading market for these interest rates, providing hedging methods for stablecoin yield strategies, thereby forming fixed interest rates.

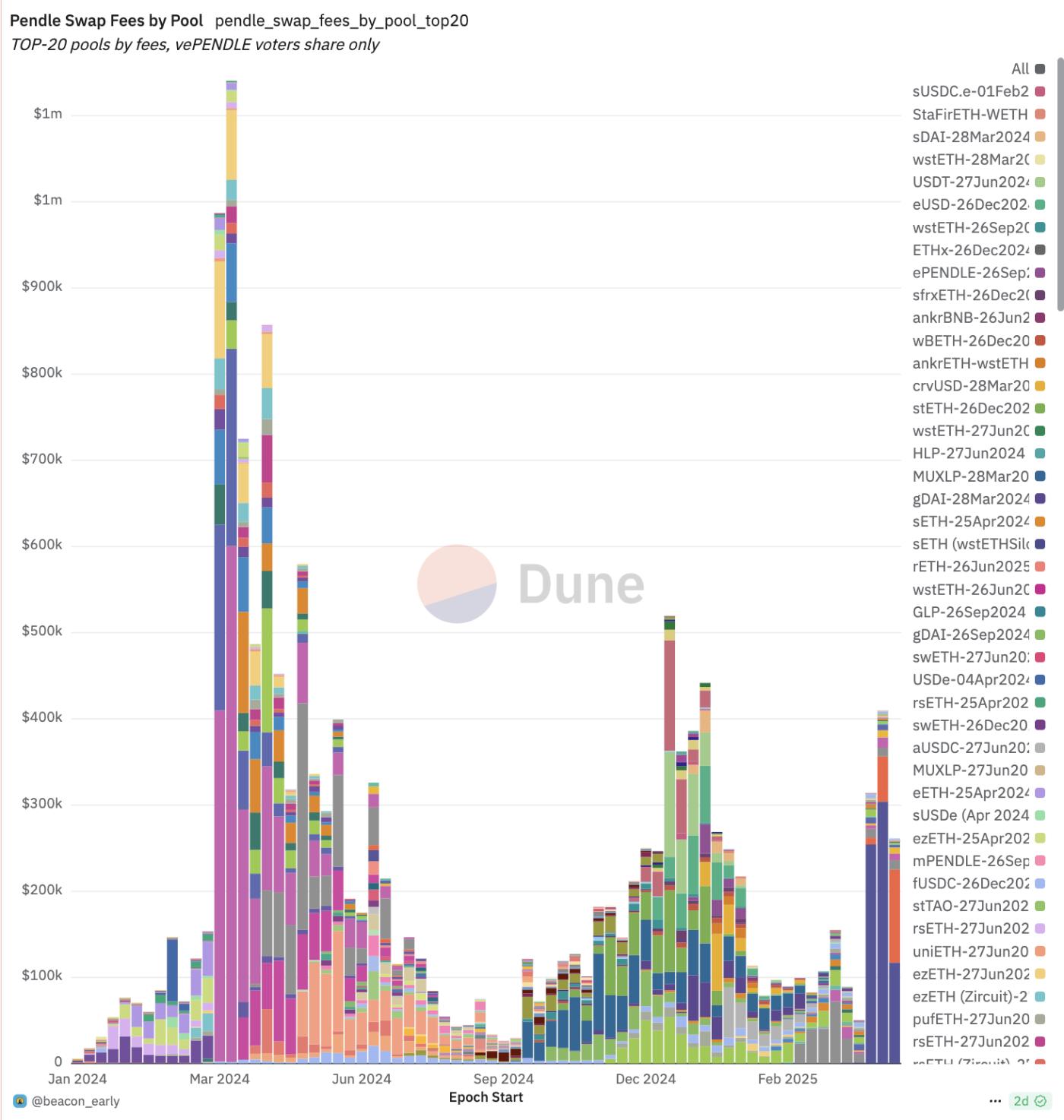

During the previous LRT wave, with EigenLayer's token issuance, Pendle's token price once dropped significantly. However, with the rise of "strategy-based stablecoins," Pendle's TVL has achieved explosive growth. It is gradually establishing its core position as the "interest rate swap layer" for such assets: Stablecoin issuers can sell future yields in one go through Pendle to hedge risks, while speculators and asset managers can buy or market-make these yield streams. With the introduction of more Δ-neutral and RWA hybrid yield coins, Pendle's TVL, trading volume, fee income, and vePENDLE ecosystem are rising in sync. Currently, it has formed a near-monopolistic leading advantage in this track.

Disclaimer:

This content does not constitute any offer, solicitation, or recommendation. You should always seek independent professional advice before making any investment decisions. Please note that Gate and/or Gate Ventures may restrict or prohibit all or part of its services from restricted regions. Please read its applicable user agreement for more information.

About Gate Ventures

Gate Ventures is the venture capital arm of Gate, focusing on investments in decentralized infrastructure, ecosystems, and applications that will reshape the world in the Web 3.0 era. Gate Ventures collaborates with global industry leaders to empower teams and startups with innovative thinking and capabilities, redefining the interaction modes of society and finance.

Official Website: https://ventures.gate.io/

Twitter: https://x.com/gate_ventures

Medium: https://medium.com/gate_ventures