Get the best data-driven crypto insights and analysis every week:

Tokenized Bitcoin: Extending Bitcoin’s Utility

By: Tanay Ved

Key Takeaways:

Tokenized bitcoin, such as wrapped bitcoin (WBTC) and cbBTC extend the utility of BTC beyond its base layer, enhancing accessibility and interoperability across chains.

Wrapped BTC tokens come with varying custody models and governance structures, ranging from fully centralized issuers (e.g., Coinbase’s cbBTC) to decentralized, smart contract-based systems (e.g., Threshold tBTC).

WBTC remains the largest by supply (~129K BTC), but cbBTC is quickly gaining share with native issuance across Base and Solana (~43K). Together, they represent over 172K BTC in tokenized form, used differently across chains.

Wrapped BTC is widely adopted in DeFi. WBTC dominates Ethereum DEX activity (led by Uniswap v3), while cbBTC is more active on Base DEXs like Aerodrome. Together, over $7B worth of WBTC and cbBTC is locked in lending protocols like Aave and Morpho, allowing users to borrow against their BTC.

Introduction

Bitcoin’s scarcity and predictable monetary policy make it a desirable “store of value”, with ownership increasingly shifting towards long-term holders, ETFs and the corporate treasuries of public companies. But as BTC is increasingly “HODLed”, what does it mean for the untapped utility of Bitcoin’s $2T native token?

In response, a growing range of products have emerged with the shared aim of putting BTC to work. From Bitcoin-based lending (i.e. Coinbase and Morpho’s integration, or Cantor Fitzgerald's Bitcoin credit facility via Maple Finance), to layers aiming to scale Bitcoin, wrapped bitcoin tokens for interoperability across chains and corporate treasury vehicles like Strategy, all reflect efforts to make Bitcoin more productive across the stack.

In this issue of Coin Metrics’ State of the Network, we explore the growing ecosystem of tokenized Bitcoin, focusing on Wrapped Bitcoin (WBTC) and Coinbase’s cbBTC as mediums for extending BTC’s utility across chains.

The Landscape of Tokenized Bitcoin Products

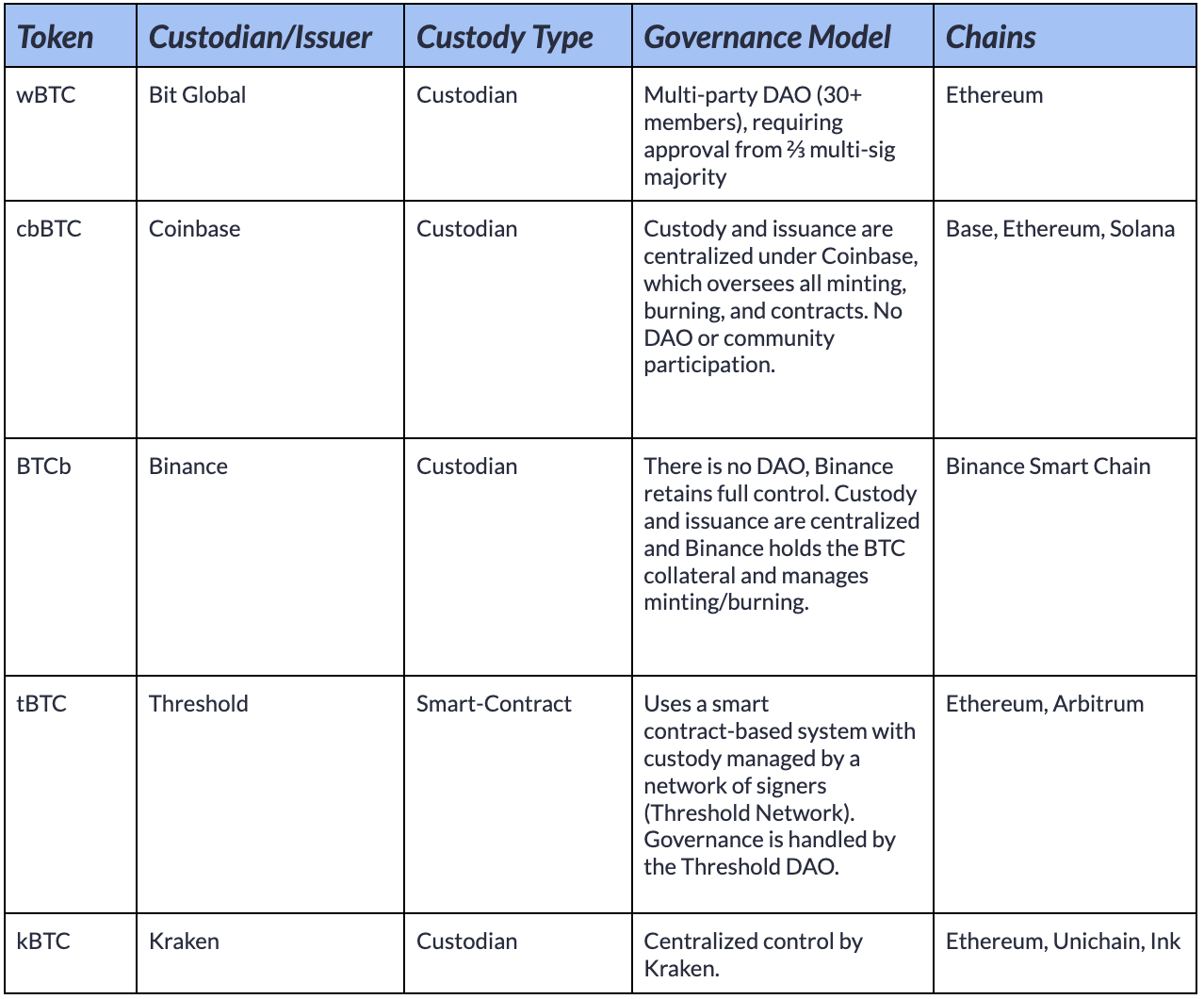

The demand for utilizing BTC across smart-contract platforms has culminated in an array of tokenized bitcoin, also referred to as “Bitcoin derivatives.” Among these, wrapped bitcoin is the largest category, representing tokenized versions of BTC issued on other blockchains, typically via a mint and burn mechanism and backed 1:1 by native bitcoin held in custody.

Wrapped bitcoin tokens aim to make BTC more accessible and interoperable, bringing programmability and lower-cost execution not available on Bitcoin’s base layer. The table below provides an overview of major wrapped Bitcoin tokens, comparing their custody models, issuing entities, governance structures, and supported blockchain networks:

While these tokens share the common goal of extending Bitcoin’s utility, they come with varying trust assumptions. Solutions today range from fully custodial models like Coinbase’s cbBTC, to DAO-based multi-signature systems like WBTC, and distributed, smart contract-based systems like Threshold’s tBTC. In all of these models, users give up custody of their bitcoin to a third party in exchange for a tokenized representation.

While the table above highlights the major bitcoin wrappers, there’s also an emerging category of liquid staked BTC derivatives. One example is Lombard’s LBTC, which represents BTC earning staking rewards by helping secure proof-of-stake (PoS) chains via Babylon Protocol.

BiT Global WBTC & Coinbase cbBTC

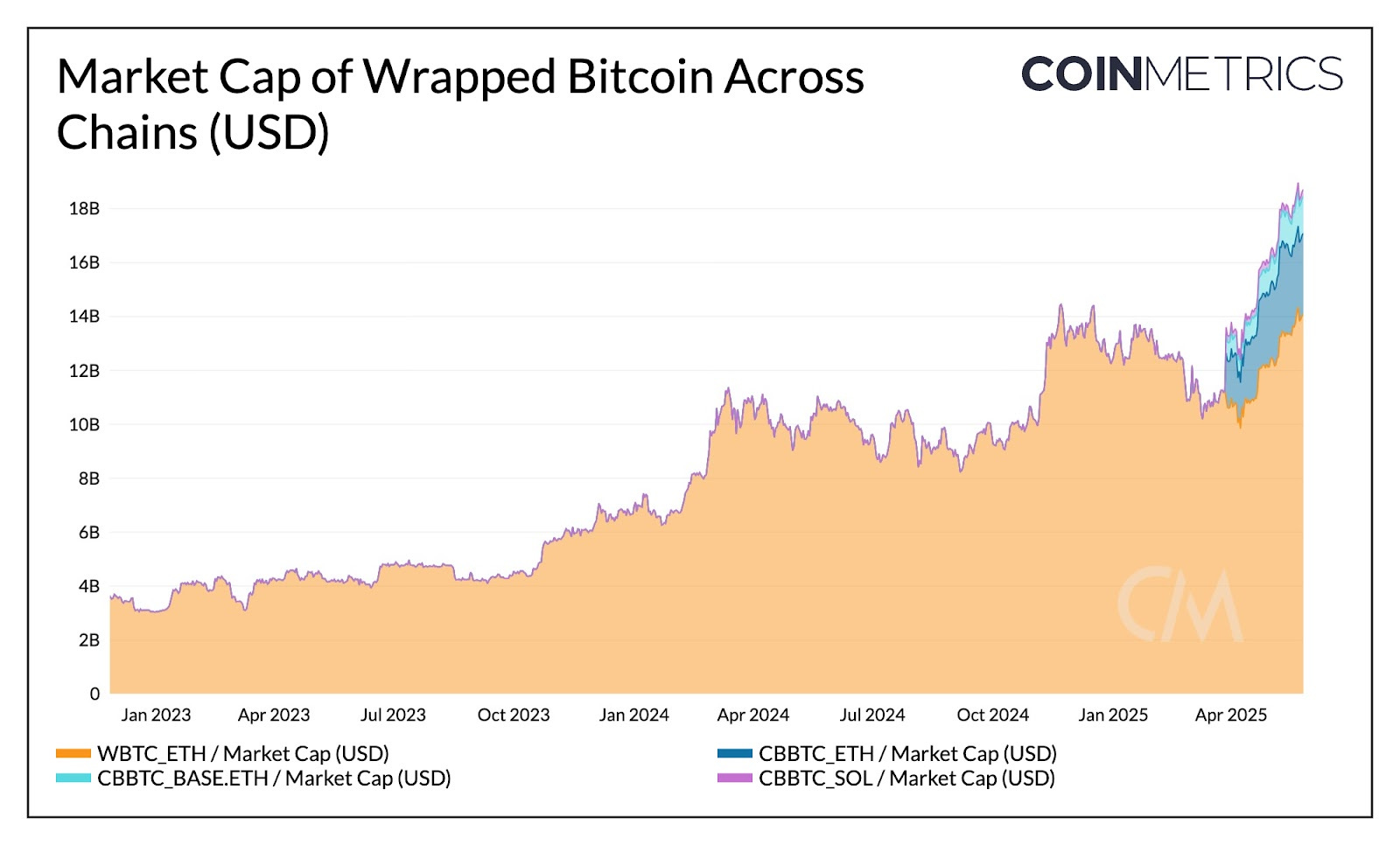

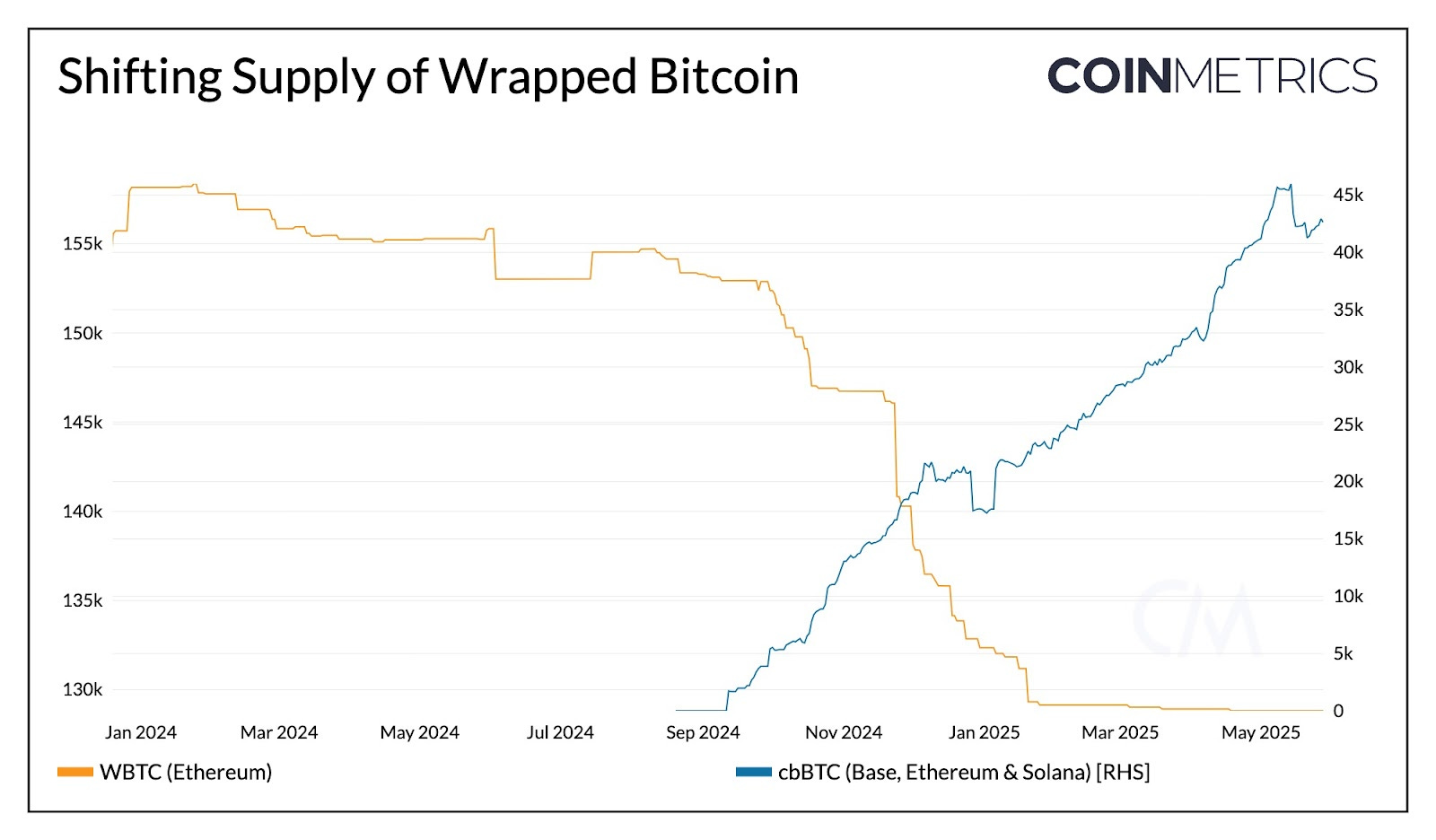

The market cap of wrapped bitcoin has quintupled since January 2023, boosted by a rising BTC price and the issuance of new products across chains. The two largest tokens include WBTC and cbBTC, issued by BiT Global and Coinbase respectively, with a total combined supply of 172,130 BTC.

Source: Coin Metrics Network Data Pro

As the first wrapped bitcoin token introduced to the market in 2019, WBTC has historically dominated the sector. However, amid the ownership of WBTC changing from to a consortium with BiT Global in September 2024, demand for WBTC appears to have softened. Meanwhile, the timely introduction and growth of Coinbase’s cbBTC as an ERC-20 token on Base and Ethereum, and as an SPL token on Solana has offset the decline in WBTC.

Source: Coin Metrics Network Data Pro

As of June 1st 2025, WBTC commands 81% of the wrapped bitcoin market with a current supply of 128.8K BTC. In contrast, cbBTC accounts for the remaining 19%, with issuance split across Ethereum, Base, and Solana at 27.6K, 13.2K, and 2.3K cbBTC, respectively.

Bitcoin (BTC) Usage Across Chains

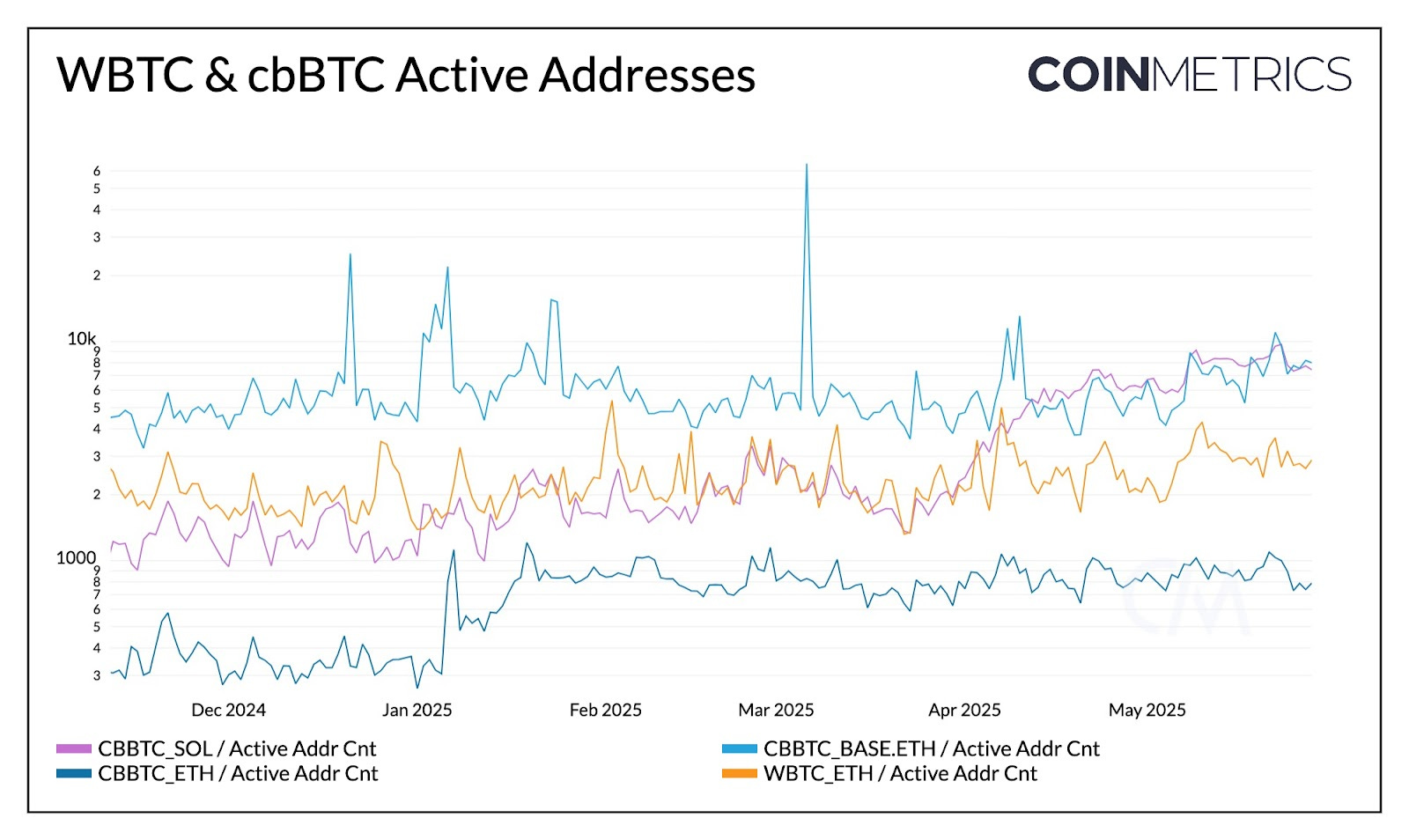

With BTC now proliferating across chains like Ethereum, Base and Solana, on-chain activity can offer deeper insight into their functional role within these ecosystems. While not perfect, active addresses offers a lens into the breadth of user interaction with tokenized bitcoin across chains.

Source: Coin Metrics Network Data Pro

Boosted by Coinbase’s broad distribution and low transaction costs, cbBTC on Base leads in this regard, averaging ~7000 daily active addresses. Solana follows closely, with active addresses having gained momentum since April, also benefiting from inexpensive, high-throughput infrastructure. Ethereum’s participation appears limited to larger but less frequent transactions, suggesting that while a significant share of cbBTC and WBTC resides on Ethereum, it’s used less actively compared to Base and Solana.

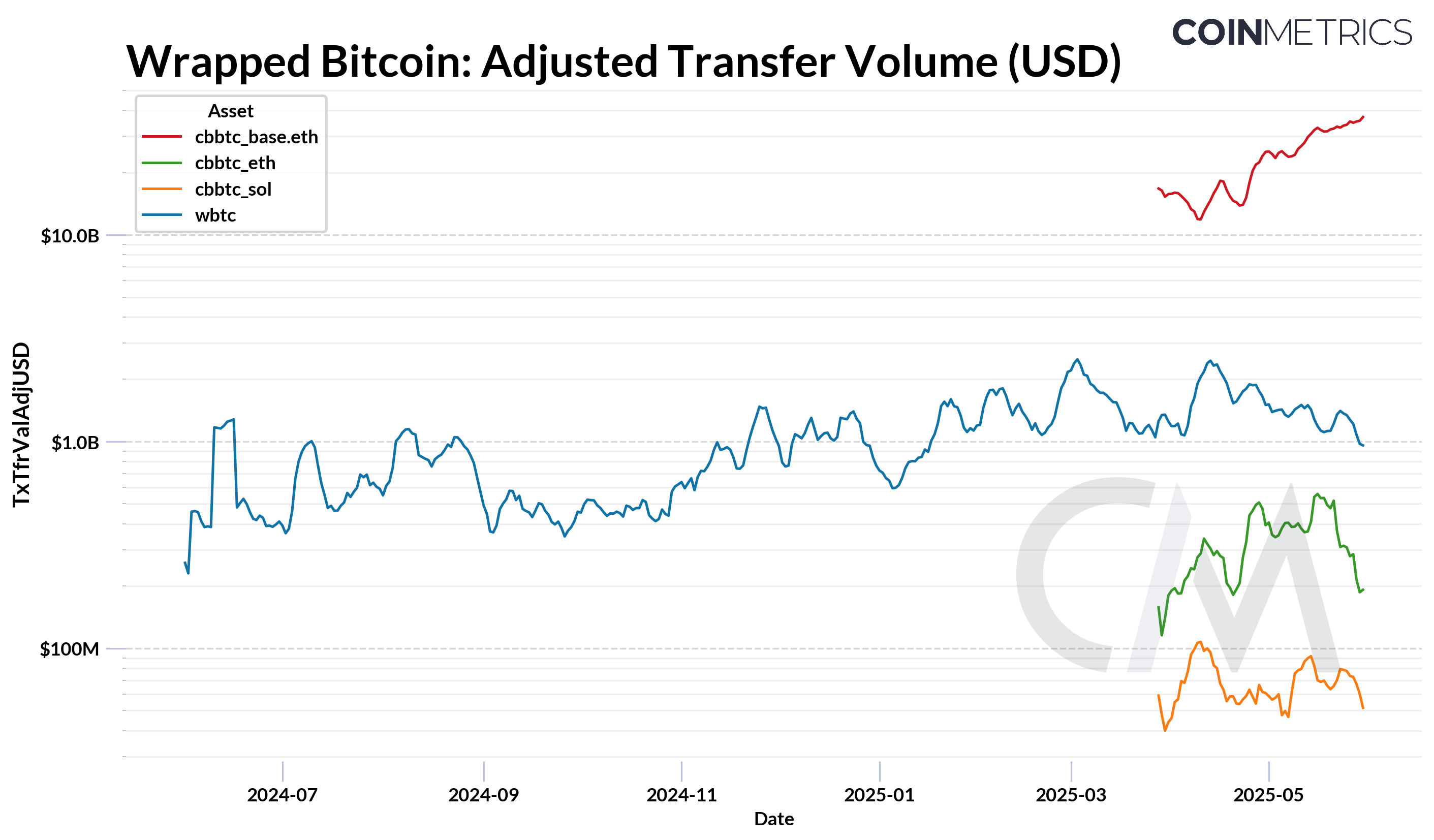

Transaction activity, measured through the count of transactions and volume of native tokens transferred, also paints a similar picture. Below, we see the adjusted transfer volume of WBTC and cbBTC across respective chains. cbBTC on Base immediately stands out, with weekly average transfer volumes reaching ~$40B. This is significantly higher than WBTC on Ethereum, which is seeing ~$1B in transfer volumes.

Source : Coin Metrics Network Data Pro

(*Note: cbBTC adjusted transfer volumes spiked on April 22 and April 26 to $506B and $787B, respectively. These outliers were excluded due to inorganic activity stemming from repeated transactions by the “Impermax Exploiter” address interacting with Morpho on Base.)

These trends are further supported by velocity, which measures how frequently tokenized BTC changes hands relative to its supply. cbBTC on Base exhibits the highest turnover, followed by cbBTC on Solana and Ethereum. All wrapped BTC variants show higher velocity than native BTC, underscoring their role in making bitcoin more actively used across on-chain applications.

Tokenized BTC in DeFi

A major driver of demand for wrapped bitcoin is to unlock utility in on-chain financial services not natively possible on Bitcoin’s base layer. As essential building blocks in DeFi, WBTC and cbBTC enable users to trade, lend, and provide liquidity without having to sell their BTC holdings.

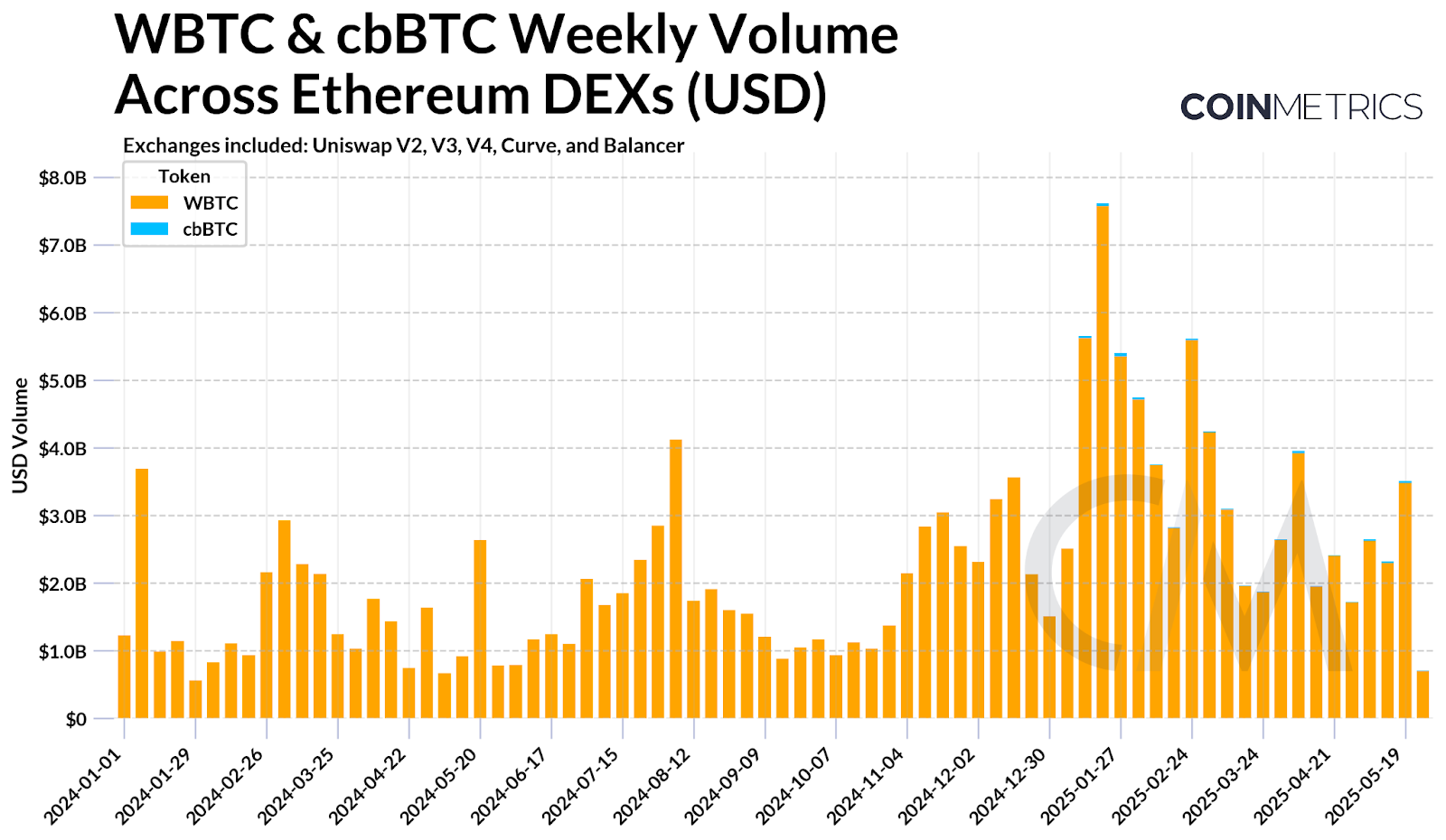

On Ethereum, WBTC remains the dominant wrapped BTC token in DEX markets, with Uniswap v3 accounting for the majority of its trading volume. While cbBTC also trades on Ethereum DEXs, its footprint remains comparatively small. To access applications on Ethereum scaling solutions, WBTC is typically bridged to Layer-2s, whereas cbBTC is natively issued across Base and Solana, giving it a broader reach across chains.

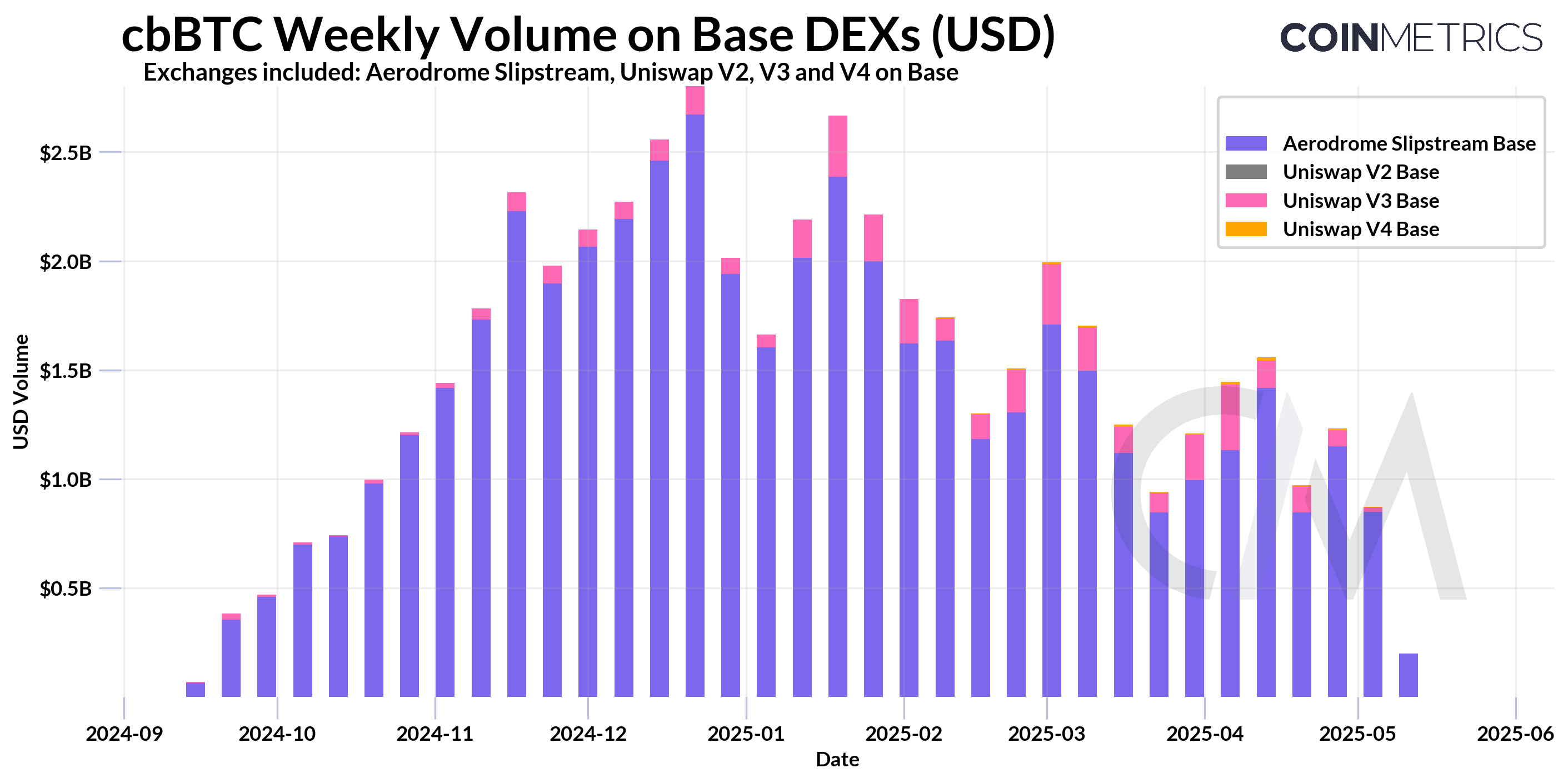

In contrast, cbBTC plays a much larger role in the Layer-2 ecosystem, especially on Base, where it is the leading tokenized Bitcoin in DEX activity. Most of the trading volume occurs on Aerodrome Slipstream, seeing over $2.5B at its peak in early 2025, followed by additional activity on Uniswap v3 on Base.

Source: Coin Metrics DEX Data & CM Labs

(*Note: Volume on Uniswap v3 Base for 4/26 and 4/30 were adjusted to exclude a set of repeated cbBTC trades initiated by a single address. These trades involved patterned USDC to cbBTC swaps and were removed to filter out inorganic activity.)

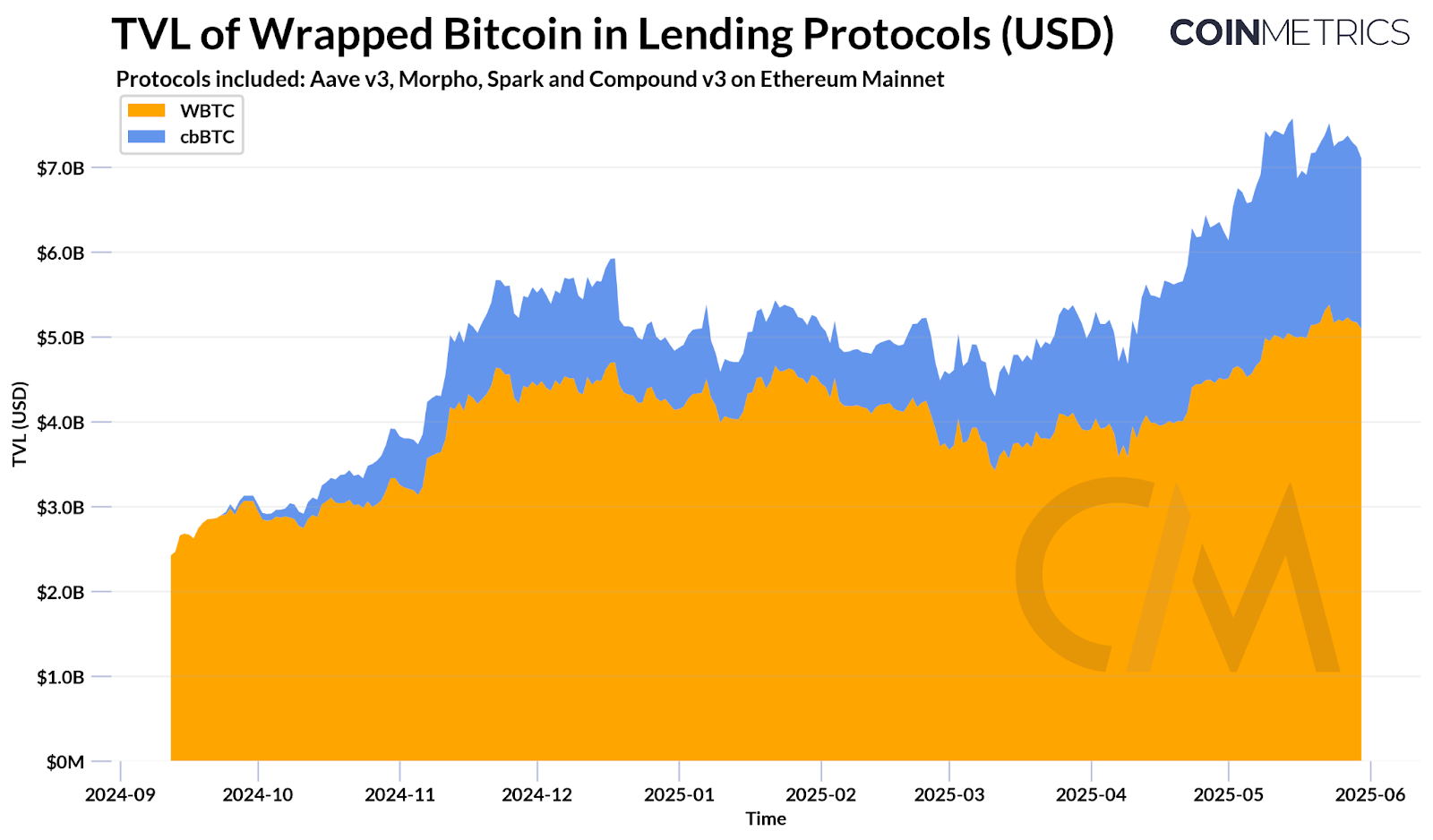

Beyond trading, wrapped BTC is a critical component in Ethereum-based lending markets. Both WBTC and cbBTC are widely adopted as collateral assets, with Aave v3, Morpho, and Spark being the largest holders of the cbBTC. As of June 2025, over $7B worth of WBTC ($5B) and cbBTC ($2B) is locked in these protocols, reflecting growing integrations and demand for bitcoin-backed lending.

However, introducing different versions of wrapped BTC as collateral comes with tradeoffs. Custodial models like cbBTC (issued by Coinbase) and WBTC (overseen by BitGlobal and a multi-sig DAO) can centralize risk, exposing users to custodial intervention. Protocol DAOs, market curators, and borrowers must weigh these risks against the liquidity and utility these tokens enable.

Conclusion

While Bitcoin’s role as a store of value remains foundational, wrapped tokens like WBTC and cbBTC are simultaneously expanding the utility of BTC. With these products, BTC can now seamlessly move across chains, participate in on-chain finance and integrate with new execution environments. While these models introduce varying trust assumptions, their adoption suggests market appetite for making BTC more versatile. As parallel efforts such as rollups and sidechains evolve, tokenized BTC will likely remain a key bridge between Bitcoin’s monetary reserve status and the programmable economies built on other networks.

Coin Metrics Updates

Follow Coin Metrics’ State of the Market newsletter which contextualizes the week’s crypto market movements with concise commentary, rich visuals, and timely data.

As always, if you have any feedback or requests please let us know here.

Subscribe and Past Issues

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.