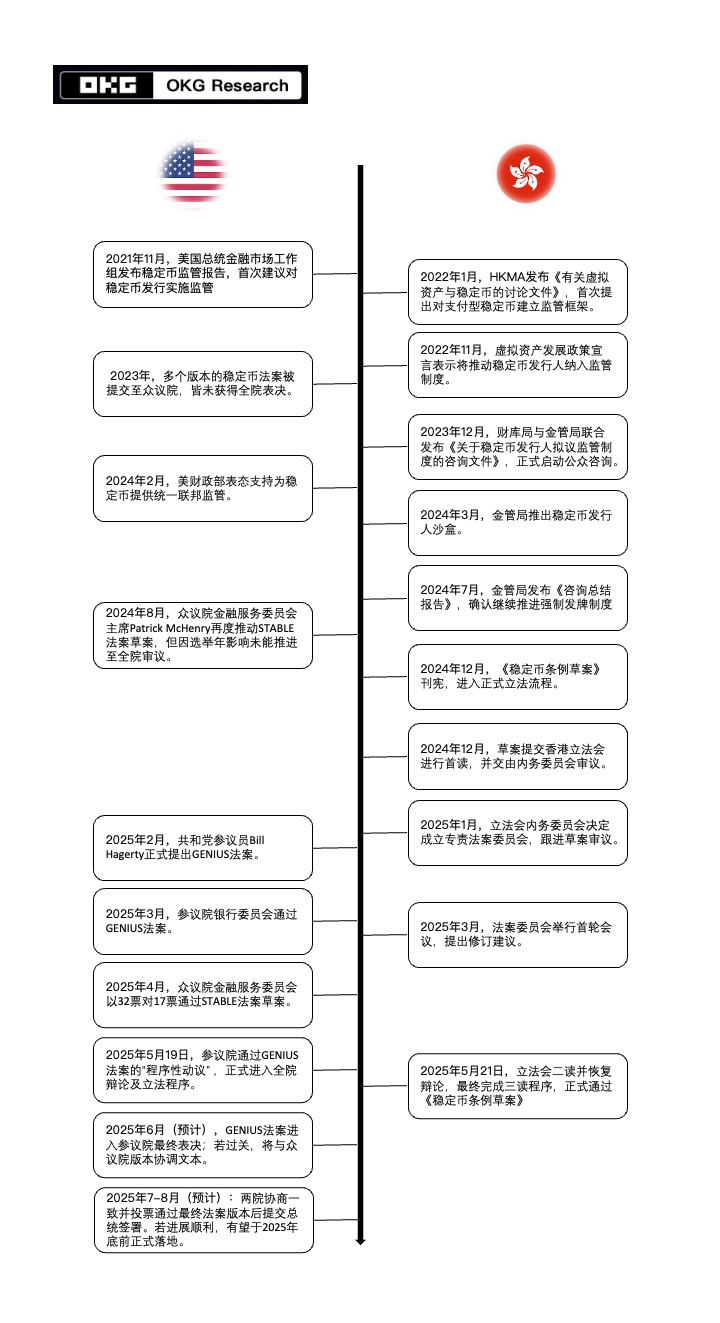

The U.S. Senate and Hong Kong Legislative Council have almost simultaneously taken key steps in stablecoin regulation this week: the former overwhelmingly passed a procedural motion for the GENIUS bill, clearing obstacles for the first federal stablecoin law in the United States; the latter passed the Stablecoin Ordinance through its third reading, making Hong Kong the first jurisdiction in the Asia-Pacific region to establish a stablecoin licensing system. The highly coincidental legislative pace between East and West is not just a chance encounter, but a competition for future financial discourse.

Stablecoin Annual Transaction Volume May Exceed $100 Trillion by 2030

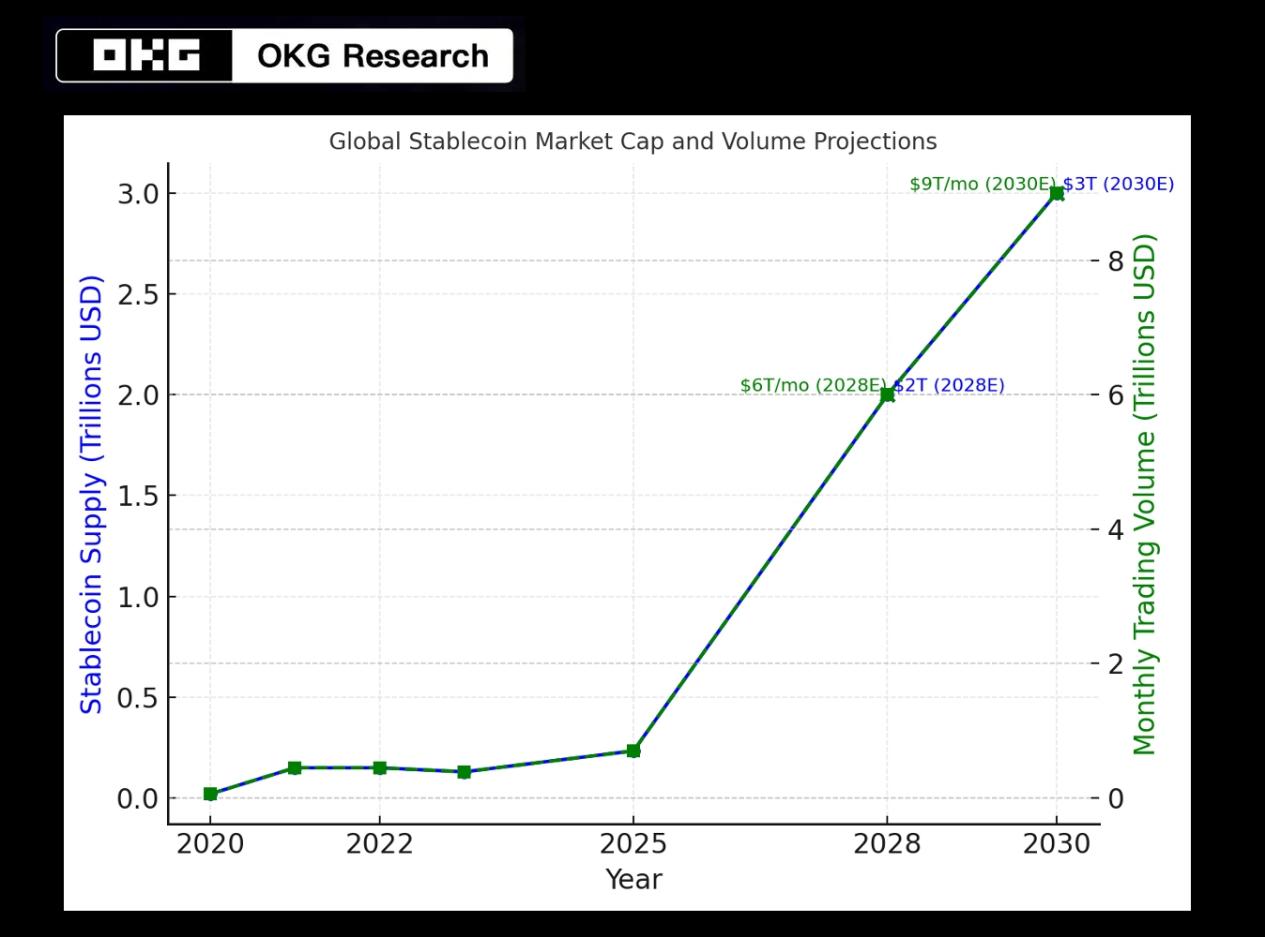

According to OKG Research's incomplete statistics, the current global stablecoin market value is approaching $250 billion, growing over 22 times in the past 5 years; from the beginning of 2025 to now, on-chain transaction volume has exceeded $3.7 trillion, with an estimated full-year volume approaching $10 trillion. USDT and USDC, representing U.S. dollar stablecoins, are widely used for trading and remittances in emerging markets, with volumes in some regions even surpassing traditional payment systems. Stablecoins have evolved from marginal assets to key nodes in global payment networks and sovereign competition, and the near-simultaneous legislation in the U.S. and Hong Kong signals that the global stablecoin market has entered an accelerated compliance period.

Based on this, OKG Research referenced Standard Chartered Bank's previous calculation model and current regulatory signals and institutional fund attitudes, maintaining the current stablecoin turnover rate, calculated:

Under an optimistic scenario of gradually expanding global compliance frameworks and widespread adoption by institutions and individuals, the global stablecoin market supply is expected to reach $30 trillion by 2030, with monthly on-chain transaction volumes of $90 trillion, and annual transaction volumes potentially exceeding $100 trillion. This means stablecoins will not only be on par with traditional electronic payment systems but will also occupy a structural basic position in global clearing networks. In terms of market value, stablecoins will become the "fourth category of basic monetary assets" after government bonds, cash, and bank deposits, becoming an important medium for digital payments and asset circulation.

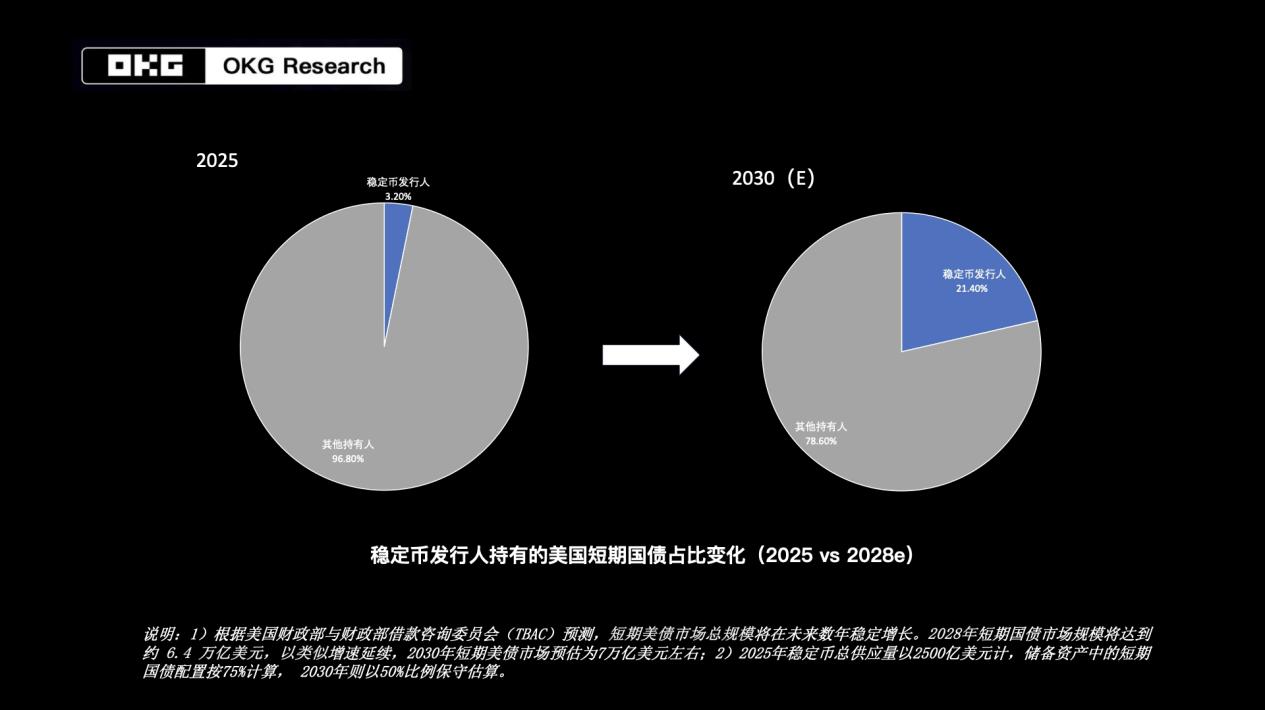

More notably, under this growth trend, the reserve structure of stablecoins will also generate feedback effects on the macroeconomic environment. OKG Research previously proposed that the existing scale of stablecoins has absorbed about 3% of maturing short-term U.S. Treasury bonds, ranking 19th among overseas U.S. Treasury bond holders.

Considering the GENIUS bill's explicit requirement of 100% high-liquidity U.S. dollar assets as reserves, short-term Treasury bonds are viewed as the primary choice (currently over 80% of USDT/USDC reserve assets are related to U.S. Treasury bonds). Estimating at a 50% allocation ratio, a $30 trillion market value would correspond to at least $1.5 trillion in short-term U.S. Treasury bond demand. This scale is close to the current overseas U.S. Treasury bond holdings of China or Japan, and stablecoins are poised to become the U.S. Treasury's "largest hidden creditor".

U.S. and Hong Kong Stablecoin Regulatory Frameworks: Consensus Amidst Differences

Despite differences in legislative paths and some details, the U.S. and Hong Kong have formed a high degree of consensus on basic principles such as "fiat currency anchoring, full reserves, and licensed issuance".

[The rest of the translation continues in the same professional and accurate manner, maintaining the original structure and meaning of the text.]