Written by: zhouzhou

Bill Ackman, founder of Pershing Square, warned world leaders: "Don't wait until war breaks out to negotiate, call the president now."

Ackman's warning was more than just exaggeration - it was like a plea.

A few days ago, President Trump's tariff plan was like a heavy bomb, devastating global markets, with US stocks losing $6 trillion in market value in a week, and the Dow Jones experiencing its largest single-day volatility of 2,595 points. Oil prices dropped, interest rates were cut, and inflation concerns lingered. Trump confidently claimed on Truth Social that "tariffs are a wonderful thing", but Wall Street giants could no longer sit still, speaking out and forming a tariff symphony.

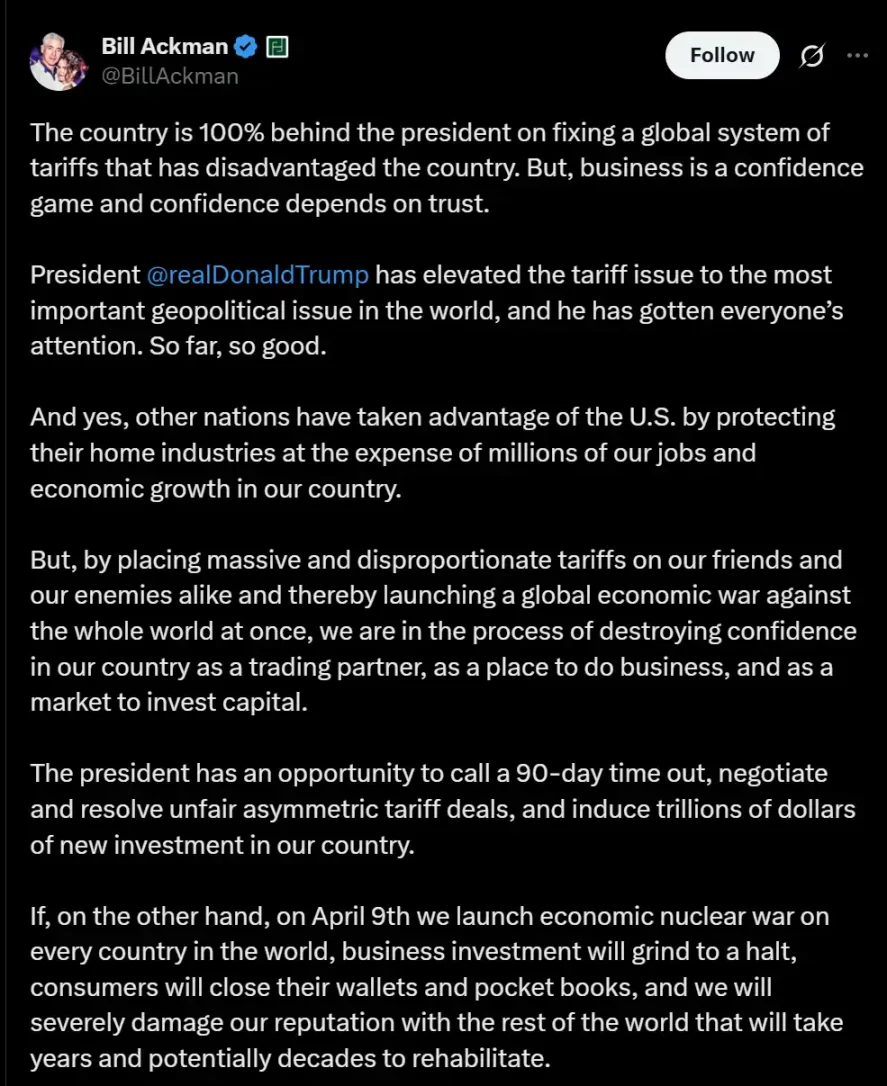

On April 6, 2025, Ackman posted on Twitter: "By imposing massive and disproportionate tariffs on our friends and enemies, we are launching a global economic war on the entire world. We are heading towards a self-induced economic nuclear winter."

Facing the Trump administration's continuously escalating tariff policy, Ackman was not the only one sounding the alarm. Many Wall Street bigwigs publicly opposed the expansionary tariff policy, even those who had previously supported him or hoped for relaxed regulation and economic growth under his government.

Former Goldman Sachs CEO Lloyd Blankfein also questioned: "Why not give them a chance?" suggesting Trump should allow countries to negotiate "reciprocal" tariff rates.

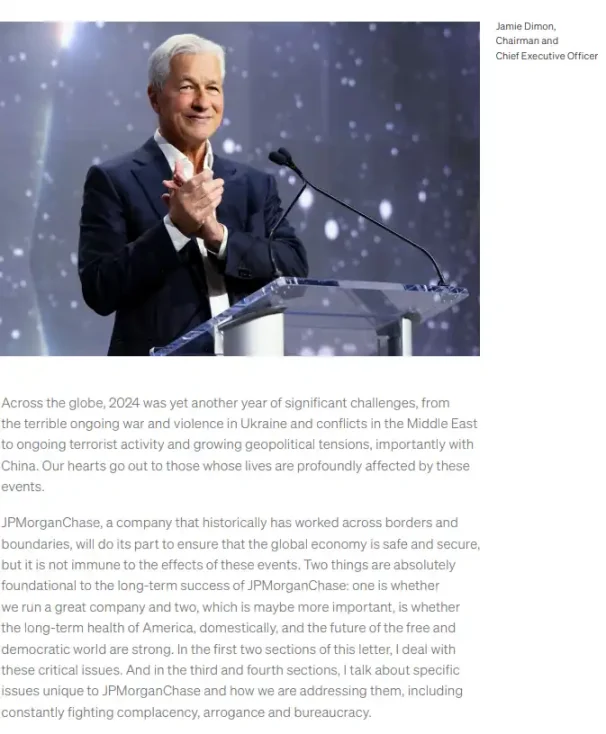

Including Boaz Weinstein, Ross Gerber, CEO and President of Gerber Kawasaki, and Jamie Dimon, CEO of JPMorgan Chase, also spoke out.

Boaz Weinstein predicted that "the avalanche has really just begun". Dimon directly stated: "The sooner this issue is resolved, the better, because some negative impacts will accumulate over time and become difficult to reverse", warning of a potentially catastrophic split in America's long-term economic alliances. Gerber called President Donald Trump's tariff policies "destructive", saying they could lead to an economic recession.

It was evident that even financial giants accustomed to market volatility, and those who had previously supported Trump, were now worried about the potential uncontrollable chain reaction of this tariff war.

The increasing criticism came as Trump showed no signs of withdrawing the punitive trade reforms set to begin on April 9. Markets can tolerate uncertainty, but not "policy speculation" based on strong-arm tactics. Wall Street's collective voice precisely demonstrated that capital is unwilling to pay for political gambling.

Howard Marks, co-chairman of Oaktree Capital, pointed out in a Bloomberg interview that tariff policies have changed the existing patterns of global trade and economics, making the market environment more complex. Investors need to consider a series of unknown variables, such as inflation potentially caused by tariffs, supply chain disruptions, retaliatory measures by trading partners, and the potential impacts of these factors on economic growth and asset prices.

Marks' warning actually revealed the anxiety of the entire professional investment circle. When policy dominates market rules, traditional analytical frameworks are failing, and even the most experienced fund managers must relearn how to bet in a global economic game.

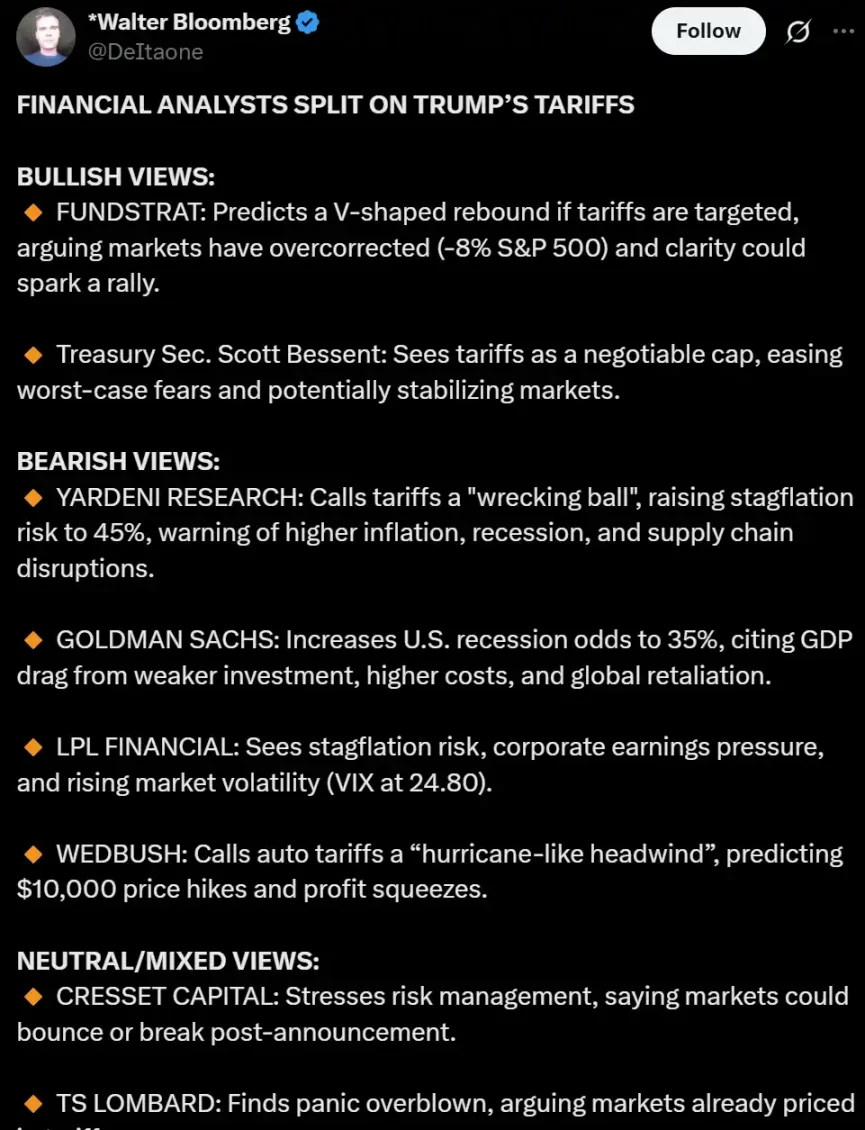

On April 3, 2025, Wall Street's stance on Trump's tariff policy was still divided. Long positions like Fundstrat and Treasury Secretary Scott Bessent believed that the market's previous adjustment was oversold, and a policy clarity might trigger a "V-shaped rebound". Shorts warned of increased risks, with Yardeni Research comparing tariffs to a "wrecking ball", Goldman Sachs raising the US recession probability to 35%, while LPL and Wedbush worried about stagflation shadows, corporate profit pressures, and potential devastation of the automotive industry.

Meanwhile, neutrals emphasized risk management, pointing out that some negative factors had already been priced in by the market, with subsequent trends critically depending on tariff enforcement and the actual resilience of manufacturing. However, as market volatility intensified and panic emotions rose, voices that were previously waiting and watching began to turn, with doubts about Trump's tariff policy becoming more pronounced.

Although Ken Fisher ruthlessly criticized Trump's tariff plan in early April as "stupid, wrong, and extremely arrogant", he maintained his usual optimistic attitude. He believed that "fear is often scarier than reality", and this storm might be just a market correction similar to 1998, potentially bringing annual returns as high as 26%.

Steve Eisman, the original prototype of "The Big Short" known for shorting the subprime crisis, warned that the market had not yet truly reflected the worst-case scenario of Trump's tariff policy, and it was not advisable to be a "hero". He frankly stated that Wall Street was too dependent on the old paradigm that "free trade is beneficial" and was at a loss facing a president who breaks traditional norms.

He admitted to suffering significant losses from being long, pointing out that the market was full of "losers' resentment". Eisman also emphasized that the current policy attempts to address groups overlooked under free trade, and Wall Street should not be surprised, because Trump "had long said he would do this, but no one took him seriously".

Amidst the clamor, US Treasury Secretary Scott Bessent emphasized that tariffs are essentially a "leverage maximization" negotiation chip, not a long-term economic barrier. He countered: "If tariffs are so bad, why are our trading partners also using them? If they only harm US consumers, why are they so nervous?" In his view, this is a counterattack against China's "low-cost, slave labor, and subsidy" system.

However, in reality, Bessent seemed to play no critical role in decision-making, appearing more like a "spokesperson" within the government to pacify the market. The violent fluctuations caused by tariffs have actually raised alerts within the White House.

This tariff storm exposed the impact of policy uncertainty on market confidence, with Wall Street's rare "collective criticism". Regardless of their stance, most voices were questioning or even angry about the policy's radicalism and hastiness. Behind the disagreements lies a widespread dissatisfaction with policy logic and execution pace. Perhaps what truly needs to be discussed is how confidence can be rebuilt in chaos?